ON DECK FOR WEDNESDAY, OCTOBER 5

KEY POINTS:

- Pivot talk gets rightly booted

- RBNZ hikes 50 as expected and with hawkish flair

- OPEC+ meeting may only further inform oil’s near-term direction

- US ADP payrolls, ISM-services, US trade on tap

- Canadian trade to further inform Q3 growth tracking

- Light overnight releases didn’t matter much

Pivot talk has rightly gone out the window here as the absurdity of taking anything the RBA does as indicative of what’s coming for the Federal Reserve’s stance was knocked back even further by their steadfast kiwi neighbours. The latest catalyst is that the RBNZ held firm and hiked its policy rate by 50bps as widely expected but with hawkish flair applied to the bias.

As a result, sovereign yield curves are back to cheapening with US yields up by 3–5bps in a mild steepener play. Canada’s curve is slightly outperforming the US. The gilts curve is also steeper on a bigger sell off in 10s (+8bps) than the front-end. EGB yields are higher across the board with wider Italian spreads over bunds being the stand out. The dollar is great again versus most pairs. Equities are lower with US and Canadian futures down by about ¾% along with similar to a little worse performances across European exchanges. Oil awaits OPEC with prices currently a few dimes higher.

In addition to hiking 50bps, the RBNZ did the following upon review of the October statement and meeting summary (here) compared to the prior one in August (here):

- guided that they discussed whether to hike by even more at this meeting. 75 was also considered but the committee reached consensus on 50.

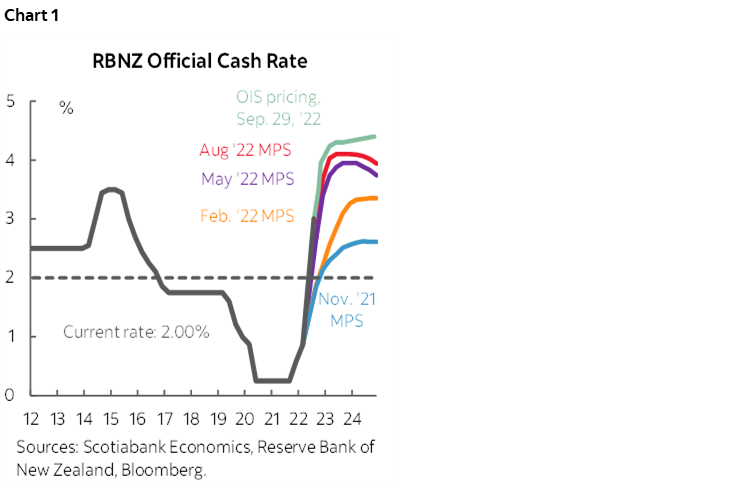

- the statement’s concluding paragraph remained unchanged with guidance continuing to say “that monetary conditions needed to be continue to tighten until they are confidence there is sufficient restraint on spending to bring inflation back within its 1 to 3% per annum target range.” Market pricing for the policy rate remains slightly higher than the RBNZ’s guidance in August (chart 1).

- reference to hiking “at pace” was retained which suggests further 50bps hikes.

- key will be the refreshed forward guidance at the next meeting on November 22nd. The last time they forecast the direction of the OCR was in August and they said it would peak at 4% or a little higher. Hiking 50 to 3.5% now and guiding further adjustments ‘at pace’ may suggest they will raise their terminal rate given changes since that prior forecast. Those changes include NZ$ weakening with a further 10% depreciation since August as the weakest major cross to the USD, stronger than expected GDP growth of 1.7% q/q SA non-annualized in Q2 (1% consensus), labour shortages and ongoing inflationary pressures.

The OPEC+ meeting is on tap as the rest of the day’s main event with potential further effects on oil, inflation trading, the rates complex, some currency pairs and energy subindices in high yield and equities. Speculation has ratcheted toward higher potential cuts of as much as 2+ million bpd. Being a cartel that is replete with cheaters, the issue to be settled over time will be whether they collectively continue to over-produce relative to their targets as they have been doing (chart 2). Either way, at least short-term markets are listening with WTI up by over US$6 so far this week on speculation surrounding the meeting. Implications for gasoline prices could impact US October CPI after we get through next week’s September print.

Data risk is light and focused upon better than expected European releases. See-sawing German export volumes were up 1.6% m/m in August which was in line with expectations, but the prior month’s drop was revised to be a ½ less at -1.6% m/m. Import volumes were up 3.4% which was much stronger than consensus and the prior month was revised up by a large 1.6 ppts to now show a small positive at +0.1% m/m. French industrial output was up by 2.4% m/m in August (0% consensus) and led by manufacturing in a rebound from an unchanged 1.6% prior drop.

The won is the pack leader this morning with a gain of over 1% to the dollar while most other crosses are weaker. Slightly firmer than expected CPI for September was the culprit. Core CPI was up 4.5% y/y (4.4% consensus and prior).

On tap will be minor data releases. US ADP payrolls (8:15amET) have been back with methodological revisions for one reading so far and the second one is due out. ADP had signalled a gain in private payrolls of 132k in August when nonfarm private payrolls were up by 308k. Enough said. US ISM-services is expected to weaken but still signal moderate growth in September’s reading (10amET). The US adds the services balance to trade figures (8:30amET) that will probably show a slightly smaller overall deficit. Canada updates trade figures for August (8:30amET) and it’s always a random guess, but this will further inform Q3 GDP tracking via exports and import leakage effects.

BanRep watchers are taking down higher than expected inflation numbers on the path to the next policy rate decision on October 28th. CPI was up by 0.9% m/m (0.75% consensus) and 11.4% y/y (10.8% prior, 11.3% consensus). That reinforces the part of consensus that thinks the policy rate will be hiked by 50bps versus the part of consensus at 25.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.