ON DECK FOR TUESDAY, OCTOBER 18

KEY POINTS:

- Risk-on sentiment continues with a little help from earnings

- Uncertainty around BoE selling drives gilts volatility

- NZ inflation soared, driving higher RBNZ rate hike expectations

- RBA minutes reinforced decision rationale…

- …but it’s not a template for other central banks

- German investor expectations remain at GFC levels

- Another strong US bank earnings beat

- Canada’s bifurcated housing market

- US industrial production expected to be soft

Risk-on sentiment continues as US equity futures are up by 1–2%, TSX futures are up by 1% and European cash markets are up by between ¾% and as much as 1 ½% in Italy. The USD is little changed but that’s masking some outliers like another drop in sterling and a strong gain by the NZ$. Sovereign curves range from slightly dearer US Treasuries and Canadas to generally cheaper gilts and EGBs but with the NZ front-end among the biggest underperformers.

What’s a day without more volatility in gilts? An FT piece argued that the BoE was going to delay selling of gilts again beyond the already delayed start on Halloween which perhaps wasn’t the best choice. The BoE issued a comment that the report was “inaccurate” but didn’t slam the door on the suggestion. 10-year gilts are cheaper by about 7bps this morning.

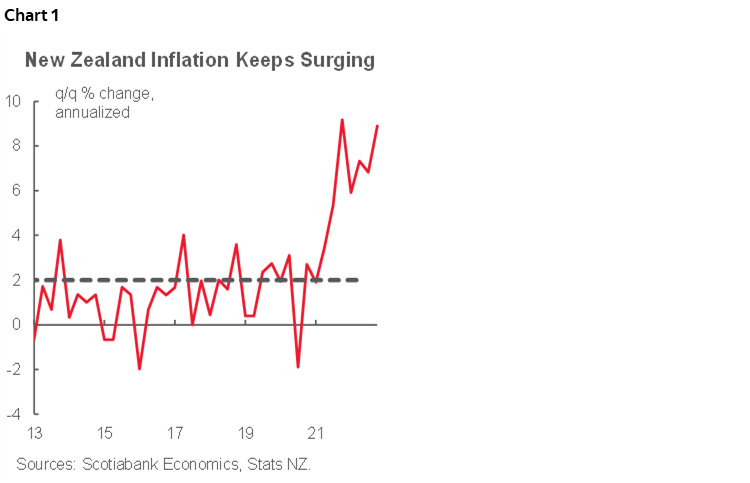

Hotter than expected Q3 inflation out of New Zealand drove the NZ$ to appreciate and the sovereign curve to bear flatten. CPI landed at 2.2% q/q SA non-annualized for a large overshoot of consensus at 1.5%. The annualized rate climbed to 8.9% q/q SAAR (chart 1). That drove the year-over-year rate to 7.2% (7.3% prior, 6.5% consensus). There was high breadth to the overshoot. Pricing for the next RBNZ move on November 23rd moved up from 58bps to 70bps as local banks increased their calls to 75bps. From 3.5% now, OIS markets have a peak rate priced at between 5½% and 5¾% next year.

Minutes to the RBA meeting on October 4th when they hiked by just 25bps said that arguments for 25 or 50 were ‘finely balanced’ and that 250bps of hikes since April justified downshifting the pace given lagging effects. Guidance continues to point toward further rate increases in data dependent fashion. Next up is Q3 inflation on October 25th as there hasn’t been a report since July.

As previously written, the RBA is not really a test case for other central banks in my view. For one, the Fed has gone the other way as a more impactful effect upon other central banks. For another, the RBA has had multiple pivots this year. Third, market pricing for the terminal RBA case rate was getting too aggressive at 4 ¼% prior to the October meeting when Governor Lowe had said he hoped it would come to rest within a 2.5–3.5% rate and so part of the aim was to rein in pricing. Markets reacted by downshifting a bit but are still pricing a terminal rate toward 4% by mid-2023 from 2.6% now. Australia also has materially softer wage growth than elsewhere such as the US and Canada and so wage-price spiral concerns are less acute.

German ZEW investor sentiment traded off a deterioration in the current situation assessment with a very slight improvement in the expectations component that nevertheless remains at its weakest level since the GFC.

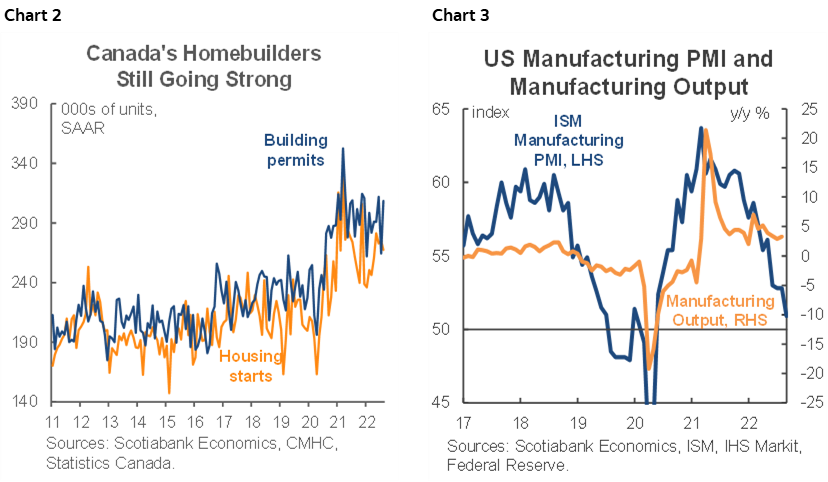

Canadian housing starts for September (8:15amET) will land in the context of continued strength in building permit volumes as the new build segment of the housing market continues to struggle with supply shortages and given the need to expand the housing stock in the face of the sharp increase in immigration targets (chart 2). US industrial production in September is expected to be soft (9:15amET) as ISM’s slippage has served as an advance signal for the manufacturing component (chart 3).

As for earnings, Goldman Sachs once again delivered the goods. Q3 EPS of US$8.25 handily beat consensus expectations by fifty cents. FICC trading revenues drove much of that beat. Netflix reports in the after-market.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.