ON DECK FOR WEDNESDAY, NOVEMBER 9

KEY POINTS:

- Mild risk-off sentiment likely driven by China’s covid developments

- Chinese covid 19 cases on the rise

- Six takeaways from the tentative US midterm results so far

- Chinese inflation weakens more than expected

- US tech sector’s November layoffs are already matching all of October’s tally

- Mexican CPI unlikely to impact Banxico’s decision tomorrow

- Fed speakers likely to stay out of the political fray

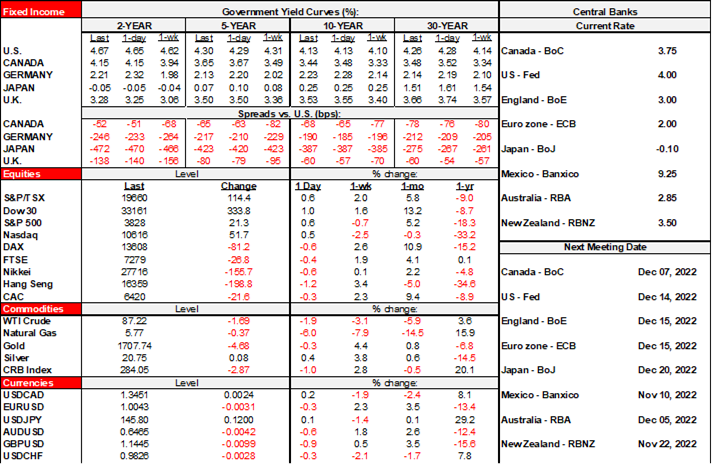

Very mild risk-off sentiment is marked by flat to slightly lower US and Canadian equity futures, mild declines across European exchanges except Italy and Spain, and declines in China and Japan. The USD is a little firmer on a DXY basis and mostly versus European and Antipodean crosses. Sovereign yields are a smidge higher in the US front-end with longer-dated EGBs and Canadas outperforming Treasuries and gilts. Oil is down over wa buck.

The mild moves are probably being driven by worsening Covid developments in China and perceived inflationary effects through supply chains even as the country’s own CPI inflation reading softened. I’ll come back to that after midterm comments.

US midterm results have not been decided and it could take a long time to get there, but so far, it’s looking like we can draw several tentative conclusions:

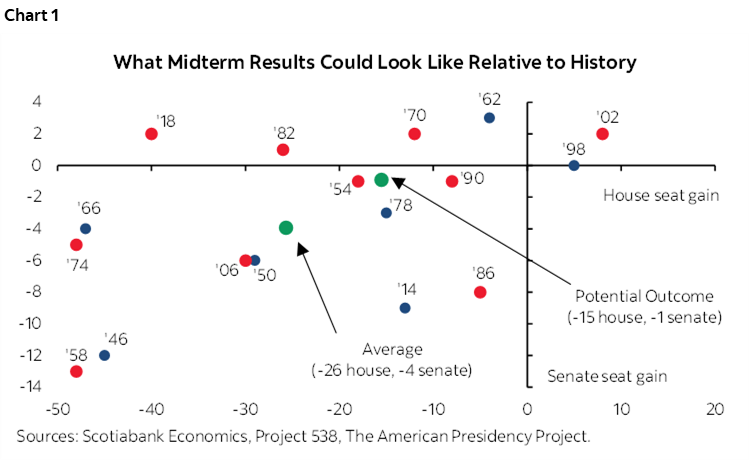

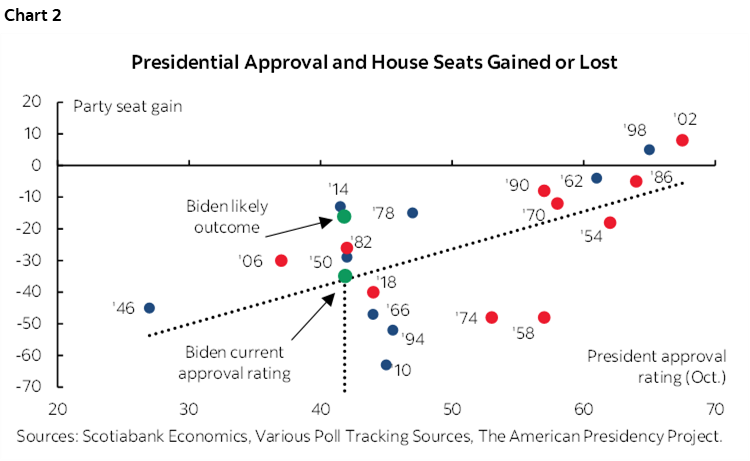

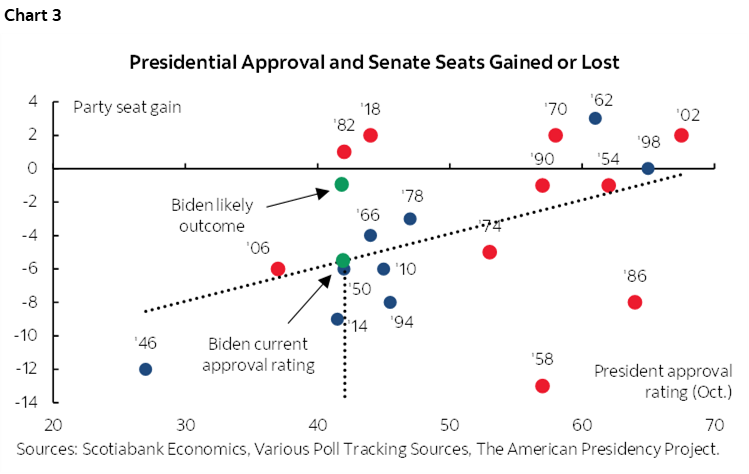

a. The Democrats didn’t suffer any worse than normal outcome in the midterms compared to prior incumbent governments and might even do better than average as shown in charts 1, 2 and 3 on the next page with tentative tracking results for this election that are likely to change when final results become known.

b. the GOP wave is hardly overpowering. They may take the House and are ahead so far, but the Senate remains a toss up and a close race in Georgia might be at risk of going to a run-off on December 6th given that so far neither candidate (Warnock and Walker) have the requisite 50% of the vote. That could add weeks to determining who won the Senate.

c. Such checks and balances are probably to be welcomed given market sensitivity toward giving either side much power at this point of a unique and highly inflationary cycle.

d. The case for Ron DeSantis to go up against Trump in pursuit of the GOP nomination for the 2024 Presidential race got a major boost by his performance in Florida and the shortcomings of Trump-backed candidates in the results so far.

e. The case for Gavin Newsom to seek the Democratic Party nomination for 2024 also strengthened with his performance.

f. DeSantis versus Newsom in 2024? In my personal view, that would be a welcome turning of the tide as America would put two divisive Presidents with a tonne of baggage into the rearview mirror.

Chinese stocks fell with mainland exchanges down by about ½% while the Hang Seng was 1.2% lower. A modest number of new cases in Beijing was nevertheless the highest tally since May. The largest outbreak in the country is in Guangdong province and its cases also climbed to the highest since last April. The Foxconn “iPhone City” plant remains under lockdown conditions. Stocks can do whatever in China, but as near as I can tell the downside risks to the economy are still acute and include ongoing property market challenges, souring growth prospects across key export markets, Covid Zero that seems to be broadly intact regardless of speculation at the margins, and the fact that the PBoC’s hands are significantly tied with the yuan’s tumble this year to 7.2 on the Fed-PBoC spread driver that they probably don’t want to worsen given the stability considerations. A tumbling currency isn’t quite the same shock absorber that it is in other economies given the massive glut of savings tied up in Chinese banks.

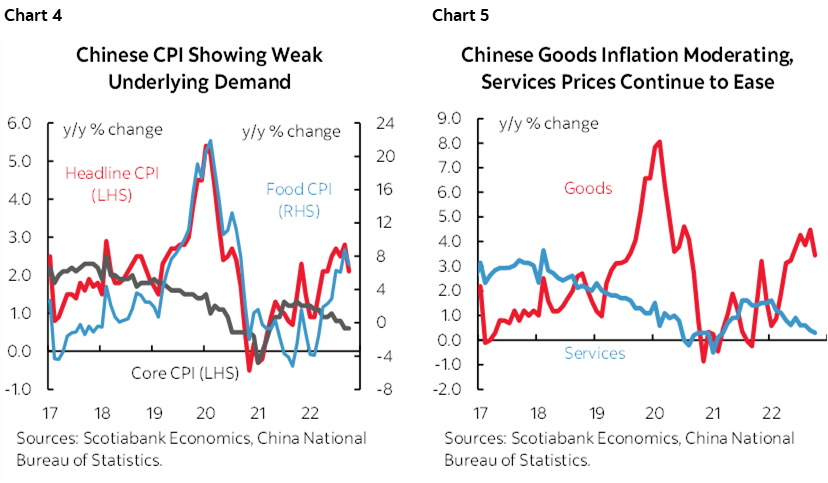

Chinese inflation weakened by more than expected (charts 4, 5). Headline CPI decelerated to 2.1% y/y (2.8% prior, 2.4% consensus). It was up by only 0.1% m/m is seasonally unadjusted terms which is about average for the month. Core CPI held at 0.6% y/y which is about half of the peak that was set late last year and early this year. The yuan weakened a bit and rates shook it off.

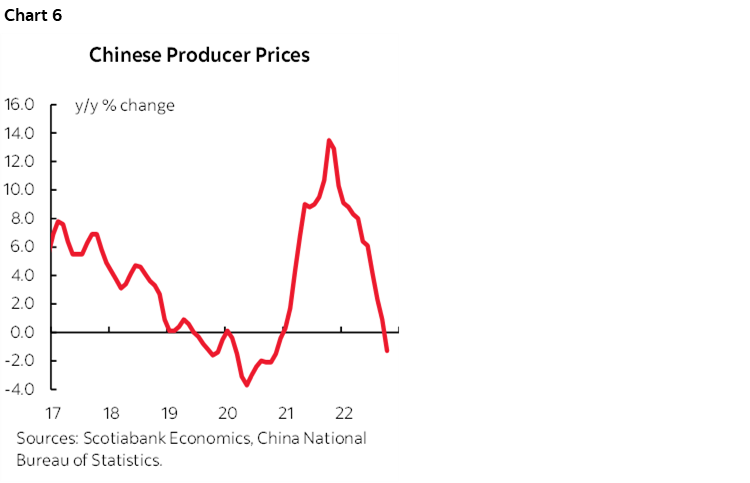

Chinese producer prices fell by 1.3% y/y which was in line with expectations for continued descent from a peak of 13.5% y/y last October (chart 6). Headlines shout deflation which this isn’t, at least not in the classic economist’s definition as a sustained economy-wide decline in many prices that changes behaviour by motivating consumers to postpone purchases into a cheaper future environment. That’s very difficult to turn around. Think Great Depression. This deceleration is principally driven by lost y/y momentum in oil prices.

Meta Platforms’ share price is up sharply this morning as it announced 11,000 job cuts that will take the US tech sector’s layoff tally up to about 20k in the nine days of this young month. That almost matches the acceleration to 22k tech layoffs in all of October.

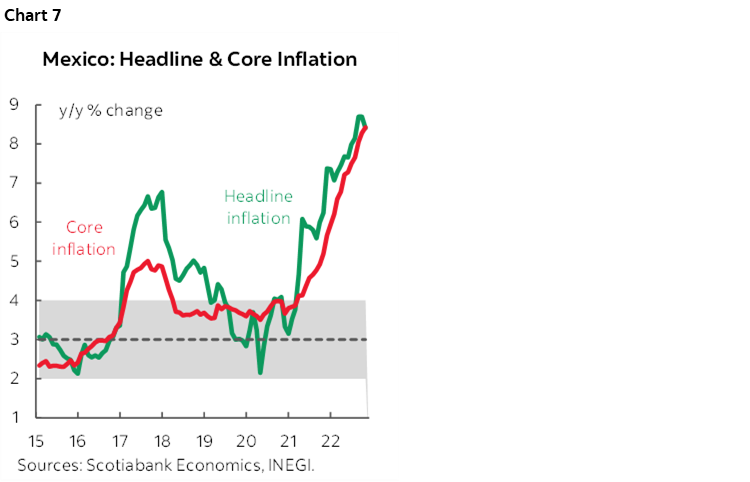

Mexico’s inflation update was met with the big shrug as the results landed on the screws (chart 7). Headline and core CPI were both up by 0.6% m/m, matching expectations. The results were unlikely to impact tomorrow’s Banxico decision anyway amid widespread expectations that it will follow the Fed’s recent 75bps hike. I’m not sure the results would even impact the bias, since Banxico may not be 100% wedded to following the Fed but is pretty closely aligned toward its path.

Continue to watch Fed-speak for guidance on the diversity of opinion around how to adjust terminal rate projections in next month’s updated SEP and dot plot given Chair Powell’s guidance last week. They wisely stayed out of the fray on election day and might keep playing it safe today. Richmond’s Barkin (11amET) and Minneapolis President Kashkari (8pmET) are both on tap.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.