ON DECK FOR FRIDAY, NOVEMBER 4

KEY POINTS:

- Risk-on optimism driven by ongoing speculation China to ease Covid Zero stance…

- ...but will it hold up when nonfarm hits?

- US payrolls preview

- Canadian jobs preview

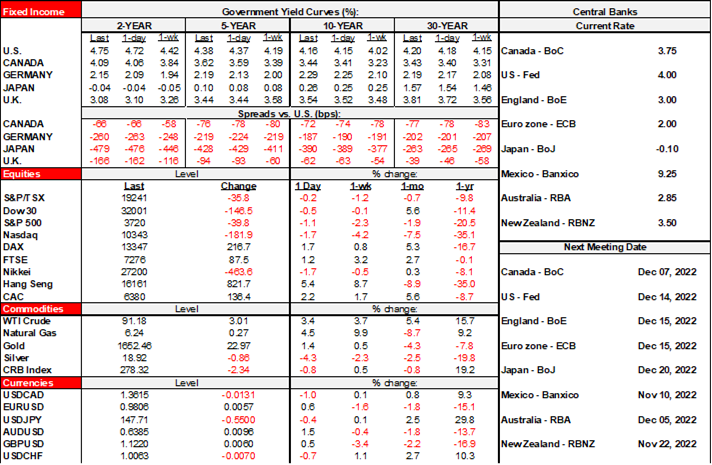

Welcome to Jobs Friday, with a solid market assist from ongoing speculative optimism in China that is driving risk-on sentiment across global markets pending US payrolls. Stocks are broadly higher with US futures up by ¾%, TSX futures up by over 1%, European cash markets gaining by 1–2% for most exchanges, while China optimism drove the Hang Seng up by 5.4% with mainland China’s exchanges up by about half that. Oil is up by about 3% and driven by the same China optimism. The US Treasury curve is bear flattening a little in 2s10s, Canada’s curve is slightly cheaper by 1–2bps across maturities, while the gilts curve is steepening and EGBs are slightly cheaper across maturities on balance. The USD is broadly weaker as higher beta and more commodity- and China-oriented crosses like the A$, NZ$, rand, CAD and Scandies lead the gainers. Canada’s free-spending budget is being ignored by markets as expected, while spending goes up yet again, lip service is given to the country’s miserable productivity performance and all the while making possibly optimistic forecast assumptions and assaulting business with further punitive taxes.

US NONFARM PAYROLLS PREVIEW (8:30AMET)

- Scotia: 150k

- Consensus: 195k

- Range: 80k – 300k (most within 150k – 250k)

- Whisper: 233k

- Mean: 197k

- Median: 195k (so no material skewness)

- Std dev: 37k

- 90% confidence interval: +/- 120k

- UR: Scotia 3.5%, consensus 3.6%

- Wages: 0.3% m/m Scotia and consensus

Drivers:

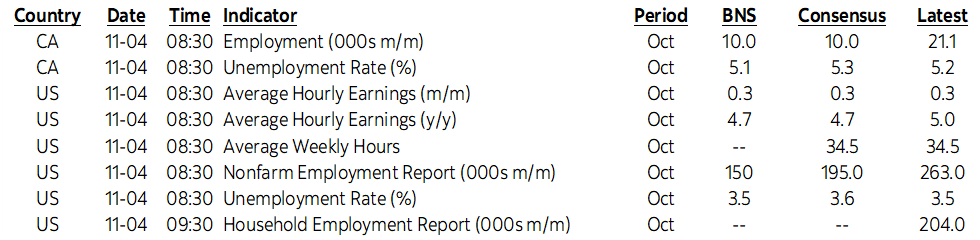

- Okun’s “law” would signal cooling trend growth in jobs as GDP growth ebbs, except for the Q3 GDP rebound. Chart 1.

- Consumer confidence signalled that jobs became less plentiful again with the reading down to its lowest since April 2021.

- nFIB hiring plans fell in October while its hard-to-file jobs readings moved sideways at its lowest since April 2021.

- There was no material change in initial jobless claims between reference periods

- ISM-services employment fell back into contraction last month

- ISM-manufacturing employment ticked back up to 50, no neither expanding or contracting

- ADP landed at 239k for October, but still offers poor tracking of private nonfarm payrolls

- JOLTS job openings increased by 437k in October and were revised up by 227k to smaller decline of 890k in September.

- on wages, the US has held relatively steady if albeit not spectacularly on a trend basis throughout this year.

CANADIAN JOBS PREVIEW (8:30AMET)

- Scotia: 10k

- Consensus: 10k

- Range: -13k to +42k (most within 0–20k)

- Mean: 8.5k

- Median 10k (so no material skewness)

- Std dev: 12k

- 95% confidence interval: +/-57k

- UR: Scotia 5.1% (lowest), median 5.3% with range of 5.1–5.5

Drivers:

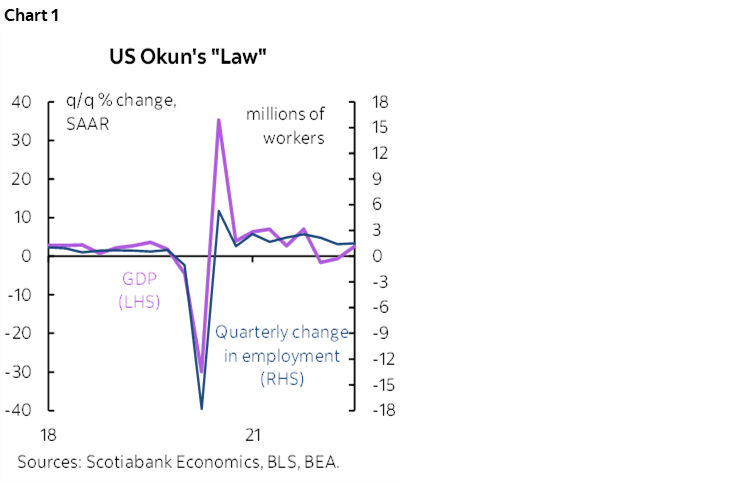

- Okun’s “law” suggests that as Canadian GDP growth ebbed in Q3 after a torrid pace of expansion over the prior four quarters that employment growth should be cooling. Chart 2.

- the education sector distortions may have stabilized after the big drop in this sector during August and the rebound in September. Expect more volatility going forward.

- weaker CFIB hiring plans

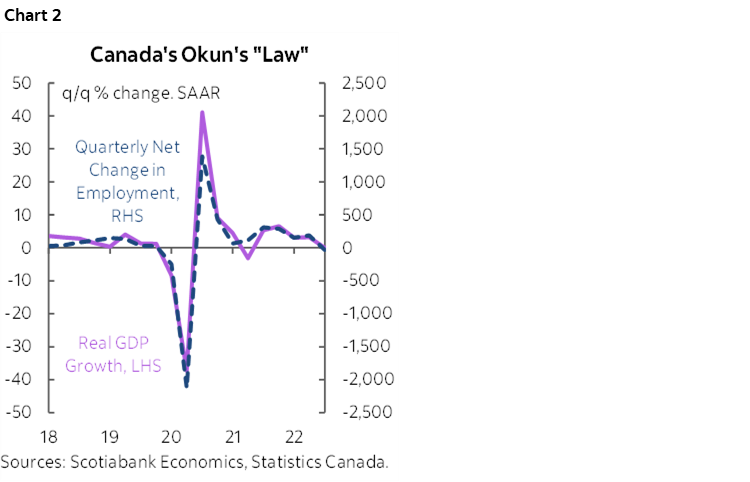

- falling labour force participation rates are making it difficult to find workers. This is focused upon young women <25 and older workers with Statcan pointing to childcare and retirement as among the drivers. This is why I went with a lower than consensus UR. Then again, the sector breakdown shows that a falling labour force participation rate since May is focused upon higher contact sectors more affected by the pandemic like retail and wholesale trade, plus information/culture/recreation and education (chart 3).

- the job market’s extreme tightness is also making it difficult to get more workers

- watch wage growth for permanent employees, m/m % change SAAR that ebbed sharply in September following very strong gains over prior months.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.