ON DECK FOR FRIDAY, NOVEMBER 25

KEY POINTS:

- Dollar strengthens, yields spike amid light volumes

- Yuan weakens on China’s RRR cut…

- ...that otherwise had little effect as it was well anticipated

- Why the PBoC cut the required reserve ratios…

- ...and why it will probably have little to no net effect

- Apple’s anecdote speaks volumes on this being early days for supply chain upheavals

- US markets face early close

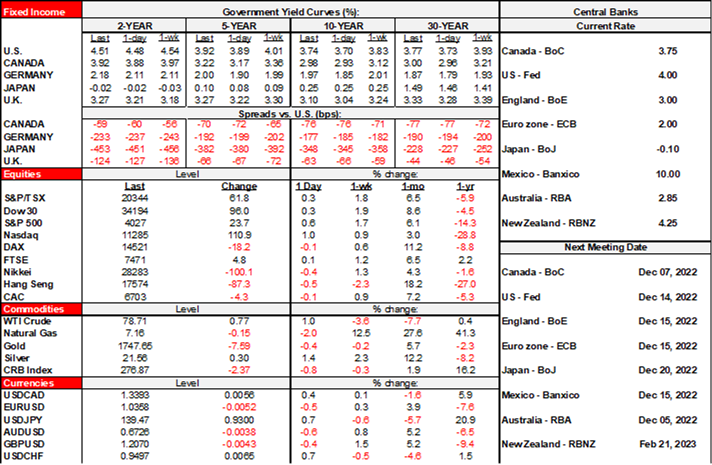

A quiet session has been spiced up a bit by China’s well telegraphed decision to cut its required reserve ratios this morning. That’s carrying little to no incremental effect on markets in part because it’s not a surprise and partly because there were more negative headlines out of China overnight concerning case counts and stealth restrictions. The half day—if that—in US markets will impair global volumes as bonds shut at 2pmET and stocks close at 1pmET.

Sovereign bonds have a cheapening bias this morning with EGBs underperforming a sell-off in US Treasuries across the curve. The USD is firmer and especially versus the yen and yuan. Stocks are little changed with a slightly negative bias across N.A. futures and European cash. Asian equities slipped a touch in Tokyo, Seoul, HK and Shenzhen with the Shanghai Composite bucking the trend somewhat. Oil is up by over a buck across the benchmarks.

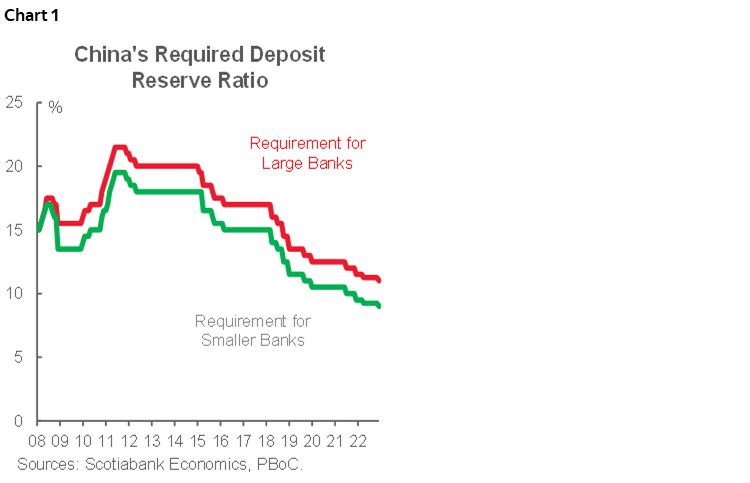

The PBoC cut required reserve ratios by 25bps effective two Mondays from now. A cut has long been anticipated even well before the State Council intimated the other day that it would pursue such a measure. See chart 1.

The PBoC estimates that the measure will inject about US$70B of liquidity into the system which is modest to say the least.

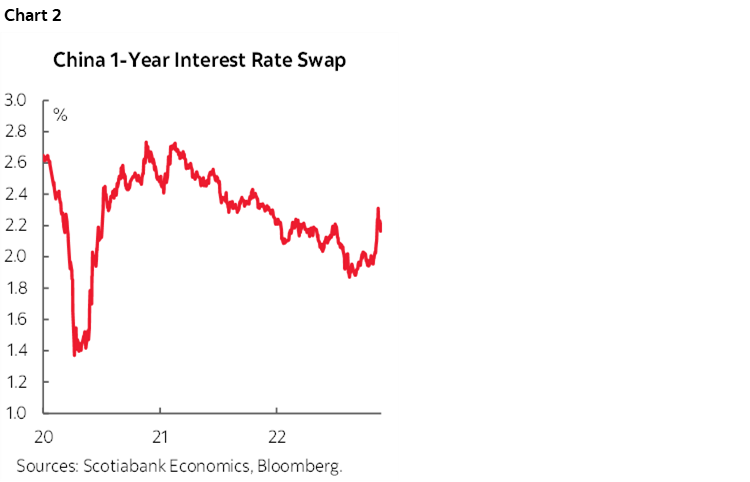

So why do it? The main motive is to address liquidity strains. Measures of liquidity had been deteriorating over time while downside risks to the economy have been intensifying. China’s one-year interest rate swap has risen by about one-third of a percentage point since mid-August (chart 2). The one-year volumes in the Medium-Term Lending Facilities have recently soared amid concern toward how a large maturity in mid-November would be handled.

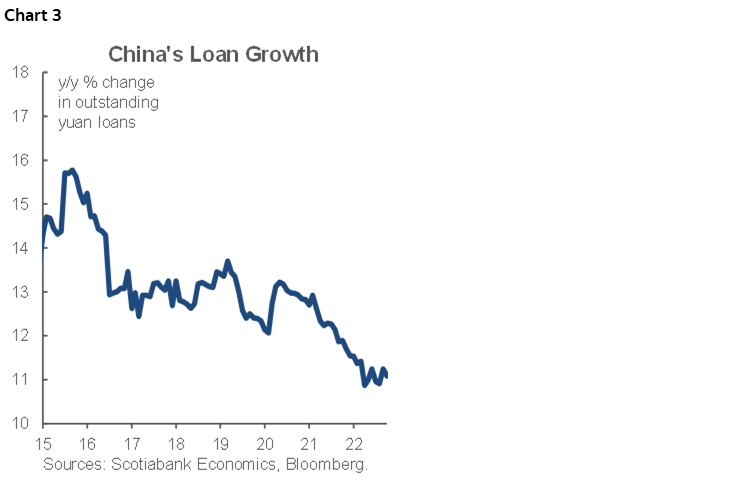

A related motive is to spur lending activity, or to at least prevent further weakening due to liquidity strains. Growth in the stock of outstanding yuan-denominated loans has been steadily decelerating since the earliest days of the pandemic (chart 3).

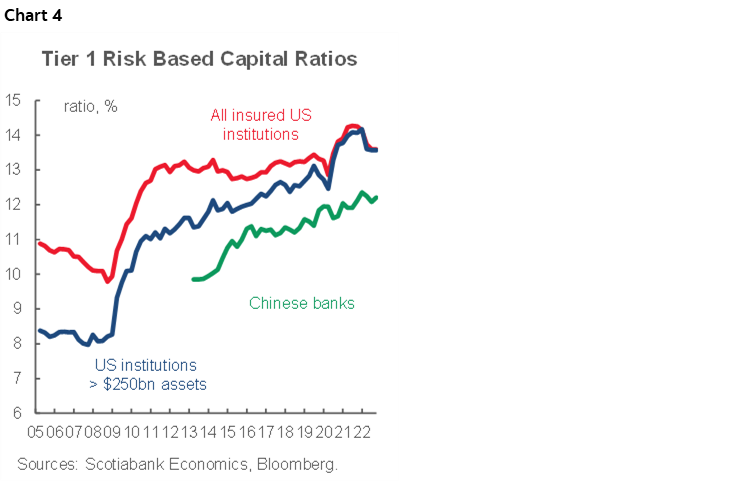

The cuts extend years of reductions dating back to 2011 as the required reserve ratios have been roughly halved over this time. At the same time, the Tier One risk-based capital ratio of Chinese banks has modestly risen by about a percentage point to 12.2% now. By contrast, the same ratio for US banks now sits at 13.6 and has increased by about 2½ ppts over the same period (chart 4).

So will it work? I’m doubtful. First, it’s not really incremental stimulus if all it is designed to do is to free up liquidity that has been under strain. The move just seeks to offset some of that and try to prevent further worsening. Second, amid mounting downside risks to China’s economy, using various monetary policy tools to try to encourage more lending requires willing lenders—which is perhaps less of the problem in a system where the state has the power to tell many of the banks what to do—and willing borrowers. It’s the latter that I doubt will respond as monpol faces the pushing-on-a-string critique. Third, the PBoC’s ability to follow through with other easing measures remains constrained by the implications for the yuan on the Fed-PBoC policy differentials.

On a mildly related note, apparently if you have an eye on putting an Apple iPhone 14 pro or pro max phone under the Christmas tree this year then you’re out of luck as the deliveries are now being pushed out to January 3rd and hence after Christmas. Analysts are pointing to the doubling of wait times over the past month due to the issues at “iPhone City” in China. I mention this because the macro implications fit my narrative that we remain at a highly nascent stage of revamping global supply chains.

On that note, everyone is focused upon short-term progress toward healing global supply chains that not only may face renewed setbacks but also face years of turmoil ahead. The macro thesis that remains intact is that while there are countless articles about near-term inflation and inventories and like matters, it remains very early days for c-suites that are grappling with how to adjust their supply chains to a permanently changed world.

The 2016 US election and Brexit vote started it all by injecting uncertainty into global trade arrangements (looking at you, Trump and Boris). The pandemic and Ukraine war escalated the disruptions to an altogether different level. Years of outsourcing to the lowest cost jurisdictions over the preceding decades was driven by the singular fixation upon reducing operating expenses and that counted upon stability driven by steady globalization. Companies across multiple sectors are now grappling with multiple vulnerabilities because of higher border frictions that impair the ability to get product on time if at all and at higher cost. Simply put, their supply chains are spread far too thinly and are more vulnerable than ever to abrupt disruptions. That, in turn, raises financial distress costs ranging from foregone sales to the extreme case of outright bankruptcy. To right the ship, a rebalancing across supply chains may tilt further toward tolerating higher expenses—and passing them on where possible—in order to lower financial distress costs.

There is a lot of uncertainty around various effects. No macro model rooted in past relationships can hope to anticipate the effects. No central bank would go out on a limb in the crafting of near-term policy by referencing longer-term risks. Markets are incapable of pricing such uncertainties that far out in time as liquidity and risk tolerance around such positioning drops off to being scant to nil.

The consequences, however, could be powerful drivers of the global macro environment for years to come. Companies may be wise to hold higher inventories given the dents to the JIT model. Companies may return to placing a premium upon more open, democratic and stable systems closer to where consumption occurs. That could motivate a shift in employment patterns toward those home markets and away from the regions of the world that benefited from one-way outsourcing. All of that, in turn, spells structurally higher inflation as part of the incidence effects attached to passing on the consequences to various stakeholders.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.