ON DECK FOR THURSDAY, NOVEMBER 24

KEY POINTS:

- Stocks and bonds richen, USD weakens

- Four factors affecting markets other than the FOMC minutes

- FOMC minutes offered no new or unexpected information

- Key US data on the path to the next FOMC decision

- Riksbank hikes 75bps, forward guidance points to only a little further tightening

- BoK hikes 25bps, Board consensus points to getting close to being done

- SARB hiked 75bps but the decision was split

- BoC’s Macklem offered nothing new, Canada’s payrolls are too stale to matter

- Turkey cuts on Thanksgiving

Risk-on sentiment is carrying stocks and sovereign bond prices higher amid lighter market activity given the US holiday. There may be several catalysts beyond all the headlines on FOMC minutes. In fact, as argued below in a separate section, I’m skeptical toward the minutes-are-dovish angle and so with that here are some other considerations.

- The first caution is to acknowledge the US Thanksgiving holiday that a) drives lower volumes of global trading activity, b) can prompt wild reactions to things in whippy markets, and c) may drive defensive position covering in rates until more normal volumes can react to developments next week.

- Second, much of the action was baked in before yesterday’s FOMC minutes after US releases that included slightly higher jobless claims and especially the reaction to a drop in the US S&P composite PMI while markets nevertheless ignored decent durable goods orders and a strong and unexpected 7% m/m gain in new home sales. The S&P gauges aren’t even the ones that the Fed watches versus the ISM measures that weed out international operations to focus upon the domestic economy. In any event, these market reactions may be continuing to drive sentiment that (some) weakening data is dovish this morning. I thought those reactions were overdone and selectively picked through the data.

- Third is speculation toward China cutting its required reserve ratio in the wake of guidance from the State Council. Efforts to stimulate China’s economy would be of benefit to global equity risk appetite. We’ll see if they deliver and if it matters, or if lenders and borrowers alike are reticent to engage because of mounting downside risks to the economy.

- Fourth, bond markets might be taking Chinese developments differently and as evidence of mounting downside risks to the Chinese economy as a reason to buy bonds. I don’t know how this will play out, but the lockdowns and generally stricter controls pose renewed risks to supply chains that will have to be closely monitored for implications by way of renewed inflationary shocks. That depends upon how far the measures wind up going through winter.

And so US and Canadian equity futures are up by about ¼% and European cash markets are up by ¼% to ¾% in Germany’s case. Tokyo and Seoul gained about 1% with the Hang Seng up by a little less as mainland China’s exchanges were little changed to slightly negative. Sovereign bond yields are under downward pressure in Europe and led by +/- 10bps declines in 10-year EGB yields. Canada’s curve is slightly richer in sympathy toward global moves. The USD is slightly weaker with gainers led by the won, yen, sterling and A$/NZ$.

Bank of Canada

Last evening’s testimony by Governor Macklem contained no new information. His opening statement is here. On hikes he repeated that “We are getting closer, but we are not there yet” in reference to an end. He also repeated that “We are still far from that goal” in reference to the inflation target.

China

There was more bad news out of China overnight with further lockdowns including Zhengzhou where the Foxconn “iPhone City” plant is located that is now locked down for mass testing starting tomorrow and over five days and then we’ll see when the results come in. There were more cases in Beijing and more preparations for a surge.

Riksbank

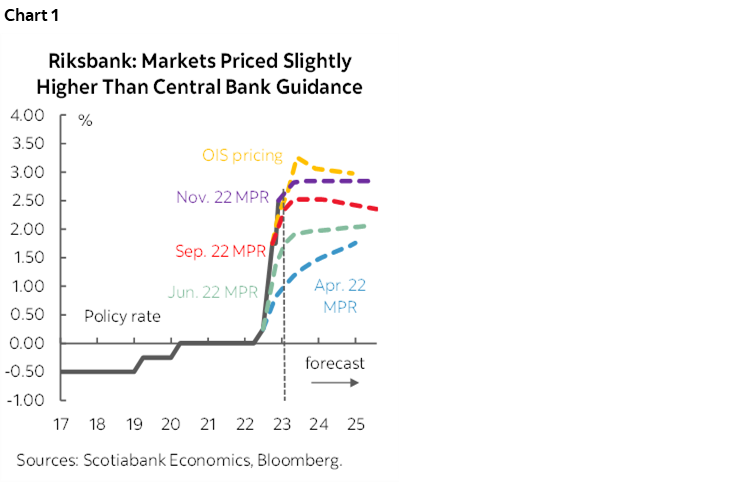

Sweden’s Riksbank hiked by 75bps to a policy rate of 2.5% which was priced, while forward guidance had little effect on the krona and Swedish short-term yields that if anything were both a little softer pre- and post-decision. Forward guidance slightly added to the prior projection with less than another 50bps of hikes expected next year to a peak projection of just under 3% (chart 1). Market pricing for the next meeting in February was unaffected with just over ¼% hike priced.

Bank of Korea

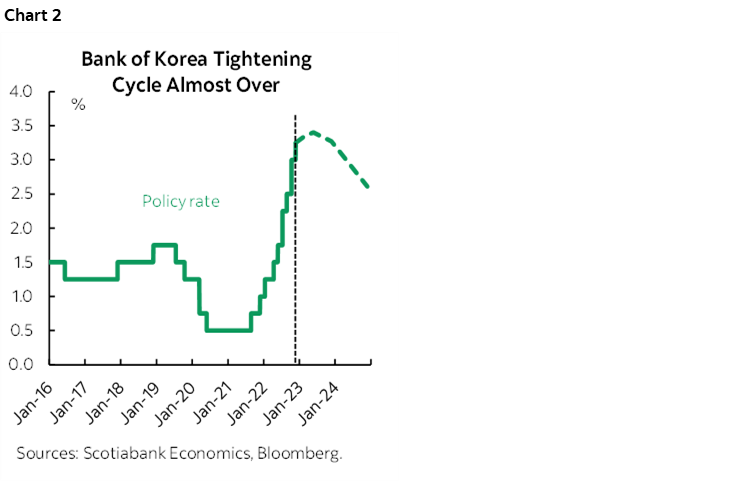

The Bank of Korea slowed the pace of rate hikes as expected by unanimously raising the 7-day repo rate by 25bps to 3.25% and guided that most of its members think only a little further tightening is likely. The front-end rallied and its higher beta currency rallied overnight, but probably more due to global forces than any surprises from the central bank. One of the earliest hiking central banks in the world began to raise rates in August of last year and has now raised by a cumulative 275bps. Governor Rhee Chang-yong guided that most Board members think the end is near, so to speak, with 1 thinking they’re done, 3 expecting only another +25bps hike, and two open to raising by more than 75bps. Pricing is shown in chart 2.

SARB

South Africa’s central bank hiked by 75bps to a 7% policy rate as expected. It was a 3–2 decision with a minority in favour of a smaller 50bps move.

Turkey

With the serious central banks out of the way we can turn our attention toward the others. Turkey’s central bank cut on US Thanksgiving; you can’t make this stuff up. Anyway, it cut its one-week repo rate by 150bps to 9% as expected. That has been Erdogan’s stated goal since September when he said that the rate should come down to single digit territory by year-end and so the complicit central bank declared that cuts are now at an end. What Erdogan wants, Erdogan gets, or he fires anyone who objects. Turks pay the price through a collapsed lira and 85% y/y inflation.

German business confidence climbed in November with the IFO expectations gauge rise by 4.1 points to 80. Big whoop, it’s still toward the lowest since the start of the pandemic after plunging ever since the peak in mid-2021.

Mexican bi-weekly inflation was in the ballpark of expectations with a 0.6% m/m rise and core up 0.3% m/m.

Beyond that the focus is likely to be mainly upon off-calendar risks into lighter global liquidity on the US Thanksgiving holiday. Canada updated payroll figures this morning that showed a gain of 85,300 positions, but that report is little watched because it seriously lags with September data on tap today (LFS is due out for November next Friday) and they only measure payroll employees in a country that has a large number of folks employed at small businesses.

FOMC MINUTES RECAP

We’re also asked to believe that an added market catalyst is that the FOMC minutes were dovish relative to already known and priced considerations. I didn’t see any new information in the minutes, but maybe folks were positioned amid lighter volumes for something other than what the FOMC officials have been saying and what markets were pricing.

Here is a recap of what the minutes contained.

1. Terminal rate: They reinforced what Powell said on November 2nd followed by other FOMC officials by way of openness toward raising it but without pre-judging how high just yet. Stay tuned for the December dot plot that I think will raise the median to 5%. This wasn’t new information relative to market pricing for a 5% peak. Here is the direct passage of relevance from the minutes:

"Even so, various participants noted that, with inflation showing little sign thus far of abating, and with supply and demand imbalances in the economy persisting, their assessment of the ultimate level of the federal funds rate that would be necessary to achieve the Committee’s goals was somewhat higher than they had previously expected."

So what does ‘somewhat higher’ mean? I’d be surprised if it’s higher than 5–5.25%, but we’ll see.

2. Pace: Powell said on November 2nd that they might downshift at either the December or January meeting. Since then, we've heard a number of officials lean toward December. The minutes reinforce this expectation with the reference to a "substantial majority" leaning toward downshifting and likely 50bps. Here is the direct quote with the key being the ‘soon’ set up given the way the Fed’s language evolves:

"In addition, a substantial majority of participants judged that a slowing in the pace of increase would likely soon be appropriate."

3. Pause: I thought they might reinforce FOMC officials' comments against pausing any time soon and against premature easing. That has characterized other communications but I don't see it in the minutes.

Data on the path to December may inform terminal rate forecasts but there is a high bar to affecting 50bps pricing. Key data will include:

1. PCE inflation for October next Thursday. I put in 0.4% m/m for PCE and 0.3% m/m for core PCE inflation which is similar to what we saw in CPI. I'm below consensus for spending though as I think some are overestimating the match between the retail sales control group and total consumption plus services consumption may not have repeated the same large prior gain as goods consumption picked up the pace.

2. Payrolls and wages for November next Friday. My guesstimates include +205k for payrolls with wages up 0.3% m/m SA. Most of the advance readings are unavailable so far.

3. CPI for November on December 13th and hence on day 1 of the next two-day FOMC meeting when they can theoretically adjust forecasts in the SEP and dots that evening that they would have first submitted the prior Friday. While it overestimated core CPI the last time around, the Cleveland Fed's 'nowcast' has a decent track record and it's pointing to 0.5% m/m for core CPI on the eve of the next decision. Headline CPI is tracking similarly to core given that gas prices were slightly lower on the month with a possible modest offset from food prices.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.