ON DECK FOR WEDNESDAY, NOVEMBER 23

KEY POINTS:

- Front-ends cheapen on hawkish regional central banks and ahead of FOMC minutes

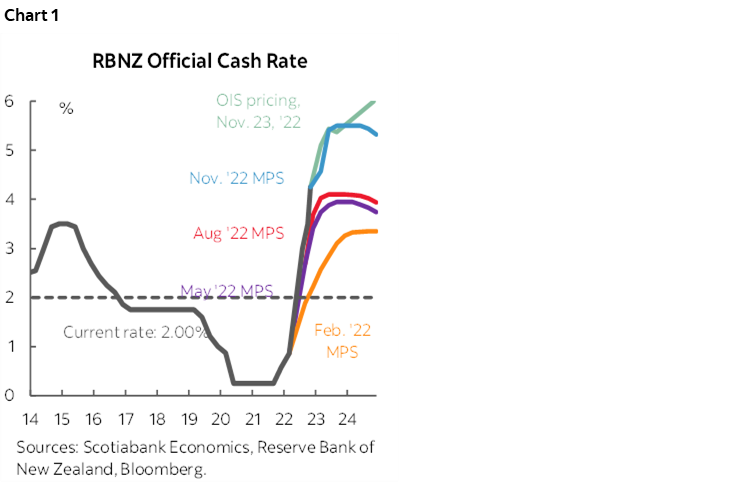

- RBNZ was even more hawkish than expected…

- …and this spilled over into other markets

- Sweden’s Riksbank will probably be the next more hawkish central bank

- China’s tangled mess of conflicting Covid Zero guidance…

- ...offsets talk of RRR cuts that may face the catch-a-falling-knife critique

- FOMC minutes to reinforce hawkish meeting takeaways…

- …but I’ll get more out of watching Canada take to the field at the same time

- Scotia Economics’ street-beating Fed Funds and BoC forecasts

- BoC’s Macklem & Rogers to testify after the close

- Global PMIs continue to signal contraction

Global markets are behaving about as one might expect given apprehension ahead of the FOMC minutes before US liquidity shuts down into Thanksgiving and in the wake of a hawkish surprise from the RBNZ that is mildly spilling over into other central bank expectations. That China headlines remain unfavourable isn’t helping either and they are offsetting RRR cut sentiment.

Equities are sticking close to home with little change in N.A. futures and most European cash markets outside of a small rise in the FTSE100. Asian equities generally posted mild gains overnight that were probably in lagging recognition of the western rally yesterday, except for Shenzhen again. The USD is little changed with gainers including the Scandies (see below), NZ$ and sterling versus weaker crosses like CAD, the yen and A$. Global sovereign yield curves are cheapening in bear flattener terms. Oil is down 3% which helps to explain CAD softness.

There was a riot at the “iPhone city” Foxconn plant in Zhengzhou as workers fought security and protested severe Covid Zero constraints. Workers complain that being isolated at the complex is spreading covid among them amid poor working conditions, and also complain about inadequate meals and unpaid wages. More mobility constraints were placed upon residents in Beijing. China is a tangled mess of conflicting Covid Zero guidance between state and local officials and it’s the local officials who are having to grapple with the pushback they are getting within an autocratic system. That continues to caution against overweighting any China narrative driven by CCP guidance.

Against these China headlines was thinly veiled guidance from the State Council that it is open to cutting the required reserve ratio again. This isn’t terribly new information as it has been the subject of speculation for some time. Personally I’m skeptical that it matters to growth. Would it really free up property lending and willingness to borrow in the context of all that ails the Chinese economy? Such hopes sound like they face the caution about catching a falling knife. China’s main export markets are going down, its Covid policies are a mess, so is its property financing market and the central bank can’t use its rate tool without cratering the currency and sparking a whole host of stability issues given the spread implications derived from a hawkish Fed. Meh, borrow anyway!??

New Zealand’s rates curve was the massive underperformer overnight and there may have been mild spillover effects into other front ends. Not only did the RBNZ pick up the pace of its rate hikes by going with a 75bps increase that was partially priced, but it also delivered pretty hawkish forward guidance. The result was that the 2-year yield is up 19bps in a significant bear flattener. The RBNZ now says that its terminal rate is likely to peak at 5½% by 2023Q3 versus the prior guidance that was set at 4.1% albeit way back in August which was the last time explicit guidance was offered and markets had long shot past that guidance given developments since then. This terminal rate guidance was higher than markets expected but markets went ever further with OIS now pricing the peak at 5½% by May (instead of Q3) which is about 30bps higher than prior to the statement. One reason for that may have been Governor Orr’s remark that he is “very eager” to get to this peak. The discussion also considered a larger move of 100bps today and the central bank is forecasting recession.

2-year yields are mildly higher elsewhere this morning on some combination of RBNZ effects and anticipation ahead of the FOMC Minutes. The Australian 2-year yield moved about 8bps higher overnight and moved the minute the RBNZ decisions hit. European 2-year yields are up by 2–7bps.

Another example of spillover effects into other regional central bank decisions is the case of Sweden. The Riksbank is expected to hike by 75bps tomorrow with all but two out of sixteen economists in that camp and markets priced halfway between 50 and 75 while some tail views leave open the possibility of a 100bps move. This is driving the krona to be the strongest gainer versus the USD this morning and may also explain some of why NOK is also outperforming despite lower oil prices.

A wave of global purchasing managers’ indices continued to signal contraction in their respective economies while nevertheless putting in varying performances that weren’t big surprises. Here’s the summary:

- Australia: the composite PMI fell by 1.1 points to 47.7 with declines in the services (47.2 from 49.3) and manufacturing (51.5 from 52.7) readings.

- Eurozone: The composite measure slightly increased to 47.8 (47.3 prior) entirely due to the manufacturing component (47.3, 46.4 prior) as the services PMI was unchanged (48.6).

- UK: The composite PMI was unchanged at 48.3 (48.2 prior) which is a statistically insignificant difference for soft data. Both services (48.8) and manufacturing (46.2) were unchanged from the prior month.

The US S&P PMIs (formerly Markit) will be released later this morning (9:45amET) and Japan’s Jibun PMIs arrive tonight. Japan might be the only composite reading to stay above the 50 dividing line between expansion and contraction.

FOMC minutes then land this afternoon (2pmET) but there is likely to be more new information arising from Canada taking the field to play Belgium at the same time than is likely in the minutes. They are likely to have a hawkish tone and there might be some market sticker shock, but I struggle with what the minutes could say that would be terribly new information. Watch for language based upon the frequency of citation of the views that are expressed (one, a couple, a few, some, several, many, most, generally all, etc) to inform matters like the central thinking around the terminal rate into the expected dot plot revisions next month, the desire to downshift the pace at the December meeting which seems to have a fair amount of support, and against pause language. I expect a hawkish tone in keeping with the hawkish reaction to the communications back on November 2nd. The minutes may be somewhat stale given Fed-speak that has leaned against pause talk after October core CPI and the solid nonfarm and wages report.

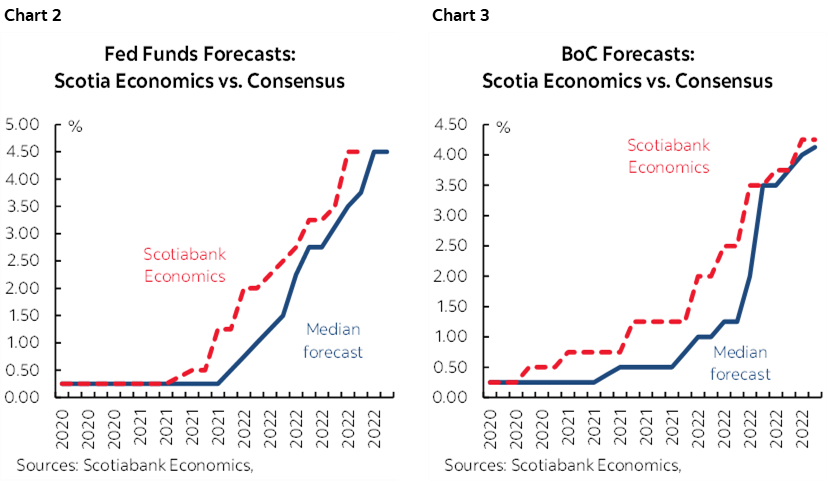

Further on the Fed and as a reminder, Scotia Economics continues to forecast the Fed’s terminal rate to rise to 5% by 2023Q1 at which point we think they’ll be done in a shift away from tracking the latest inflation prints and toward a more measured and circumspect stance toward evaluating the lagging effects of a massive 475bps rate hike and more aggressive balance sheet unwinding this time around than the last time. There is mild upside risk to this but I think the dots in December are likely to show a central tendency opinion around this terminal rate versus the 4½% to 5% equally weighted dots in the September plot. But meh, who cares what Scotia Economics thinks about the Fed, right? Chart 2 is the answer and chart 3 is the BoC equivalent. I think our BoC calls are well understood but I generally find that the Scotia Economics view on the Fed has not been well marketed and understood. In fact, some media outlets behave like outsourced marketing departments for some of the street’s highest profile shops that have had the worst Fed calls!

Then BoC Governor Macklem and SDG Rogers testify after the market close (4:30pmET). There will be another opening statement and then Q&A. One area where he may be grilled could be on his arguments around wage growth (see the week ahead). Canada has a weaker standing than multiple other industrialized economies marked by faster wage growth, tighter labour markets and poorer productivity growth—all of which means higher than average wage-price risks.

Last, US new home sales are also due for the month of October (10amET) and are expected to post a significant drop in keeping with less model home foot traffic.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.