ON DECK FOR TUESDAY, NOVEMBER 22

KEY POINTS:

- Mild risk-on sentiment with oil settling down after rumour-driven volatility

- OECD updates to consensus, long inflation battle still lies ahead

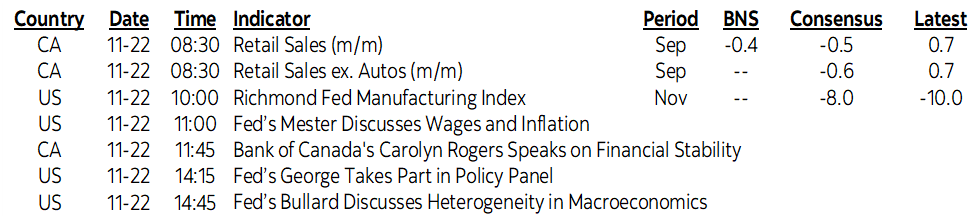

- CDN retail sales updates for September and October

- BoC SDG Rogers likely to offer low market risk

- Fed’s 3 hawks will probably just repeat prior remarks

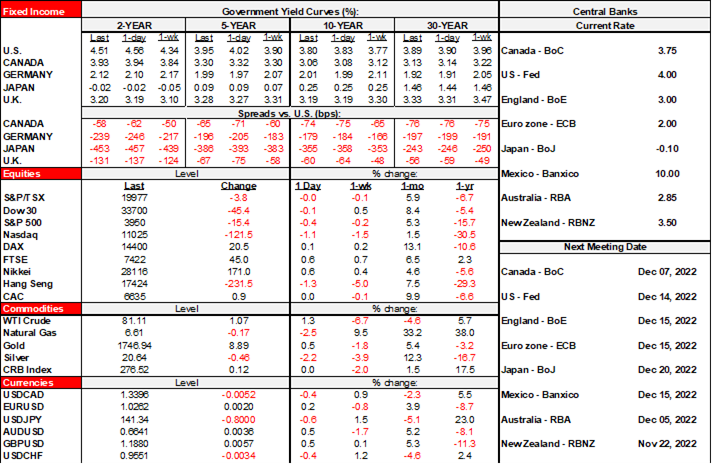

Mild risk-on sentiment is lifting equities across N.A. futures and European cash markets. Tokyo moved higher with the Nikkei 225 up over ½%, but HK fell 1.3% and Shenzhen lost 1.3% partly on policy risks as Xi Jinping’s ‘common prosperity’ drive resurfaced through executive pay cuts and tech fines. Oil is stabilizing after yesterday’s rumour-driven volatility that made no sense by positing that amid declining oil prices the Saudis would want to promote a faster increase in production; absent a rumour, start one I suppose. Sovereign yields are mixed as the US Treasuries and Canada curves push lower by 2–4bps across most maturities versus mild cheapening in Europe. The USD is broadly softer as part of the risk-on sentiment.

OECD forecasts were revised this morning (here) and the freshening brings the group in line with consensus since its last update on September 26th. They expect the world economy to grow by 3.1% this year and 2.2% next year which is basically stall speed and the weakest growth since the early 1980s excluding crisis years like 2009 and 2020. See chart 1 for growth. For inflation forecasts (chart 2), the notable thing is that they forecast the Fed and BoC being unable to hit their 2% inflation targets until 2024 while the ECB and BoE won’t do so even by then.

BoC SDG Rogers will take part in a fireside chat on risks to financial stability (11:45amET). I’m not expecting anything new out of this. Watch for repeated warnings on households mixed in with mitigating factors and how the financial system is strong. No press. Tomorrow’s parliamentary testimony by Macklem and Rogers may incrementally add to BoC insights. Or not.

Canada updates both September and October retail sales estimates (8:30amET). Be careful with gasoline price effects and cognizant of the fact that retail in Canada doesn’t capture any services spending. September’s initial nominal ‘flash’ estimate of -0.5% m/m may be revised. The fact that lower gas prices were likely among the drivers could mean something different in terms of sales volumes and breadth as details get filled in. October’s initial flash estimate will be offered for the first time. A caveat toward the prelim October reading is that it’ a nominal estimate that will be impacted by higher gasoline sales and when combined with the absence of detail we might have to wait until the fuller report in order to tell what happened anyway.

Light US developments are on tap. The Richmond Fed’s manufacturing gauge (10amET) will be a tie-breaker of sorts after the Empire gauge improved but the Philly Fed measure deteriorated while the KC Fed’s measure held little changed. More Fed-speak is on tap but I don’t expect anything new from the trio of hawks. Mester (11amET) will probably repeat her remarks that were offered yesterday afternoon before the close with no incremental effects. George (2:15pmET) is likely to repeat her remark from November 10th that the Fed “has more work to do” and more measured hikes are preferred. Bullard (2:45pmET) is likely to repeat his preference for a terminal rate peak of 5% or slightly higher after his presentation last week.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.