ON DECK FOR WEDNESDAY, NOVEMBER 2

KEY POINTS:

- Markets little changed into Fed-day

- For Powell to point to truisms isn’t a pivot…

- …and he’s likely to emphasize high-for-long guidance

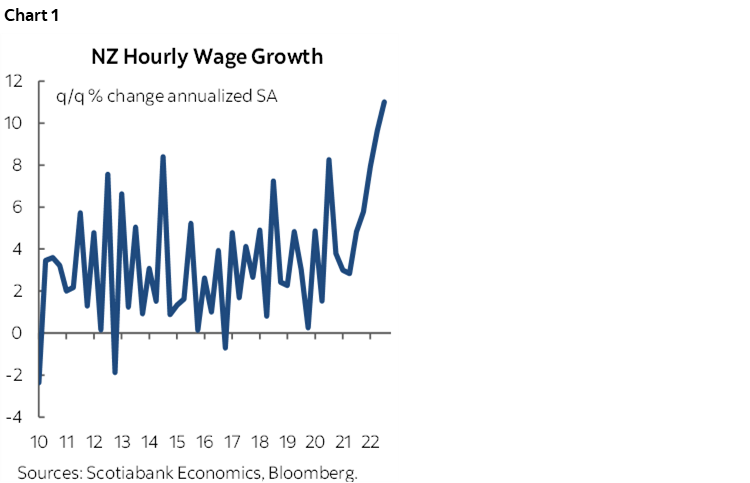

- NZ wage growth soars to an 18-year high

- Buy the rumour mentality continues to drive Chinese equities

- German trade revisions offset

- Canada’s world-beating immigration stimulus

The way Fed day ends may bear little resemblance to the way it started depending upon one’s expectations into it all. Additional catalysts include more buy-the-rumour mentality out of China, and ripping NZ wages with spillover effects across Antipodean markets. For now, the dollar is broadly softer, sovereign bonds are mixed with the US Treasury curve bull steepening as 2s richen a bit and hence reverse yesterday’s move, gilts are doing likewise but EGBs are mildly cheaper across the board and Canada’s curve is unchanged. US equity futures are little changed, TSX futures are slightly higher and European cash markets are also little changed with a slightly negative bias. Oil is down a couple of dimes.

Federal Reserve expectations are offered below but I’ll get other overnight developments out of the way first.

NZ wages drove the NZ$ to the top of the heap and motivated a 12bps spike in the 2-year yield. Hourly wage growth landed at 2.6% q/q SA non-annualized, or about 11% at an annualized pace which is the fastest rate since 2004Q2 (chart 1). This fans wage-price spiral concerns. The overall job market remains hot with employment up by 1.3% q/q SA non-annualized in Q3 (0.5% consensus) while the unemployment rate held near a record-low at 3.3% because of a significant increase in the labour force participation rate to a record-high 71.7% from 70.9%. Markets are pricing almost a full 75bps RBNZ hike on November 23rd. There may have been spillover effects into Australia’s curve and the A$ ahead of its own wages data in mid-November.

Buy the rumour sentiment continues to drive equity gains in China with local equities up by between 1% and 2½%. The drive is the same as yesterday in that markets are speculating that Covid Zero policies may be relaxed, despite all signs that restrictions are actually tightening.

German trade disappointed in September but mostly due to upward revisions to the prior month. Exports were down 0.5% m/m (consensus +0.5) but August was taken up to a gain of 2.9% from 1.6%. Ditto for imports as the 2.3% drop in September (-0.6% consensus) was mostly due to a 1.5 ppt upward revision to August’s growth that is now 4.9%.

FEDERAL RESERVE—TRUISMS DON’T MAKE FOR A PIVOT

The Fed is obviously going to be the main game in town with a few sideshows along the way like ADP head fakes at 8:15amET. The statement lands at 2pmET, we’re in between updates to the Summary of Economic Projections and dot plot with the next ones due out next month, and Chair Powell’s press conference starts at 2:30pmET.

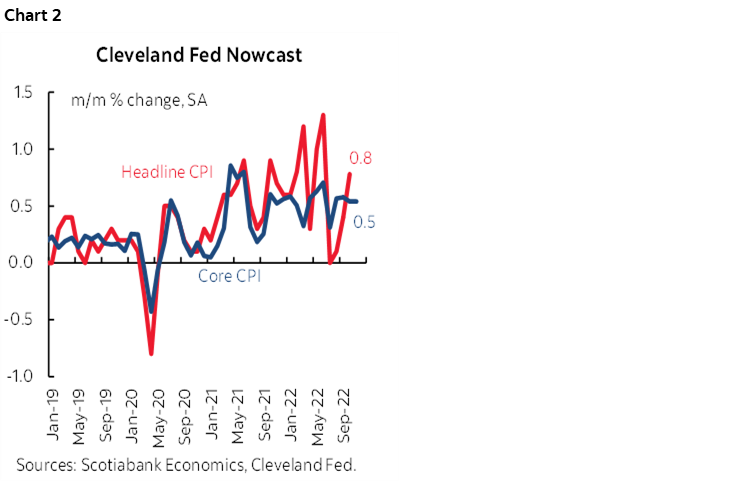

Bottom line: Powell doesn’t want financial conditions to ease and short circuit what they’ve done to date, so expect somewhat of a repeat of the last appearance with what I think will be a generally hawkish bias that says they’re not there yet and to lean against premature easing. The economy rebounded with 2.6% growth in Q3 and ‘nowcast’ tracking that is above consensus for Q4, core inflation is not cooling and the next reading for October is likely to be hot again which he would have folks telling him about, and the US labour market is not opening up any slack to date. Witness the Cleveland Fed’s core CPI ‘nowcast’ that points to another hot reading next week (chart 2).

All of consensus expects +75bps which is fully priced. The absence of forecast updates on the heels of the ones provided on September 21st likely means that the statement will be kept short and sweet, on-script and continue to guide that further rate hikes lie ahead. I expect few if any notable statement changes.

The presser is where things may be more likely to get interesting, if anywhere. It’s a truism—not a pivot—that we’re getting nearer to the end if they land at 4% today and in relation to the fact that the September dots were evenly split between terminal rates of 4.5%, 4.75% and 5%. I don’t find there would be much value to him stating the obvious in that regard and that we’ve understood for quite some time now. He’s likely to once again diss the dots anyway by saying there is high forecast uncertainty.

That could mean one more and done, which I doubt, or with hikes reaching into Q1 and in data dependent fashion which is our forecast for a 5% terminal rate. I also wouldn’t find it to be of much value if he says that, by definition, as they draw nearer to the end, the pace may be downshifted from 75bps per meeting but if I were him I’d keep options open. Yes the economy is going to be damaged, but the bigger fight is to anchor inflation expectations, amid ongoing upside risks to inflation, and to thwart wage-price spiral risks.

A hawkish surprise would be if he said they’re unsure of the terminal rate and that it could be higher than they’ve guided. It would also rattle market pricing if he said he’s still open to the possibility of another 75bps move on December 14th with fff only slightly leaning in that direction and closer to 50.

What again may be more instructive to the market tone would be that I fully expect him to lean against any talk of easing and to repeat language that he used at the last meeting. That included:

- noting that at 3.25% “We’ve moved into the very lowest level of what may be restrictive.” He’ll say they are now only just getting to be meaningfully restrictive at 4%.

- saying that in order to downshift the pace of hikes and stop, they want a sustained period of below-potential growth that so far they’re not even close to getting;

- adding to that by saying they also want evidence of cooling labour markets, ditto;

- and saying they also seek hard evidence that inflation is moving back down to 2%, double ditto;

- and positive real rates across the curve which may exist across longer maturities but not yet at the very front-end depending upon inflation expectations.

- less denial and more acceptance toward a harder landing as he has been gradually introducing meeting-by-meeting.

CANADA’S IMMIGRATION STIMULUS TO BUOY HOUSING

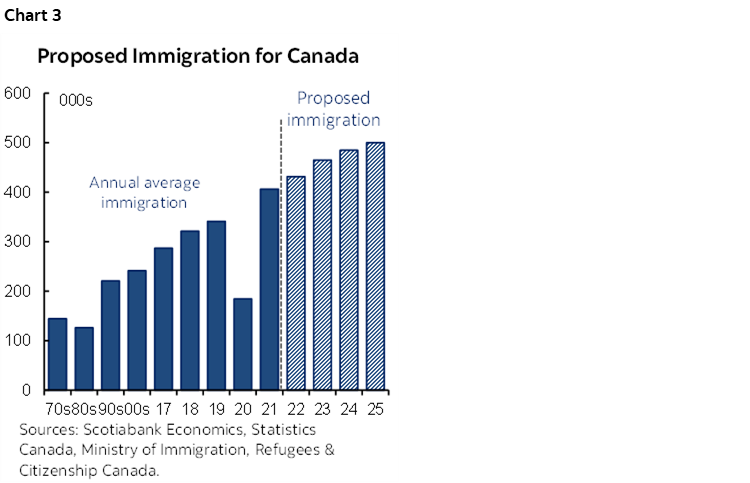

In case you missed it, Canada added more immigration stimulus to housing markets yesterday. It did so by once again raising its annual immigration target to 500,000 folks per year by 2025 while further emphasizing admittance of folks destined for the workforce. That basically means adding a new city of Ottawa or city of Edmonton roughly every couple of years. Chart 3 shows the massive surge that is definitely a stand-out compared to other major nations as Canada is the only G7 country to be recording accelerating population growth. Within less than a decade the annual number of immigrants targeted for arrival into Canada will have roughly doubled. Canada is among the few advanced nations doing something about longer run workforce challenges and there is generally high support for the initiative.

Implications include the following:

- Canada will have to build more homes. Fast. It already had deep supply issues and now they'll become more acute.

- The stimulus boost leans against a housing correction on the new build side and mitigates it on the resale side. A move like this reinforces my narrative that as housing corrects, more in resales than new, it is likely to be a replay of the repeated cycle of temporary improvements in housing affordability and then back up we go. Add in the prospects for Bank of Canada cuts of uncertain magnitude and timing maybe from late next year into 2024 and here we go again with demand outstripping supply. Sidelined domestic buyers will be accumulating cash into a softer price environment and ready to buy just as immigration fans supply shortages. That could also mean that inflation relief derived from housing and spillover effects may be transitory.

- Labour markets will welcome the higher targets over time by comparison to soft domestic demographic drivers and skills shortages, but we’ll have to get through a recession’s likely impact upon the labour market first.

- Longer run neutral rate estimates may be higher due to the workforce impact upon potential GDP growth.

- Canada had better improve integration of new arrivals and distributing them across the country. Fast. This ages old challenge is nothing new. Neither is the need to improve.

- The move supports remaining DB pensions and a need for infrastructure spending especially in the handful of cities that attract the most immigration.

Implications include the following:

- Canada will have to build more homes. Fast. It already had deep supply issues and now they'll become more acute.

- The stimulus boost leans against a housing correction on the new build side and mitigates it on the resale side. A move like this reinforces my narrative that as housing corrects, more in resales than new, it is likely to be a replay of the repeated cycle of temporary improvements in housing affordability and then back up we go. Add in the prospects for Bank of Canada cuts of uncertain magnitude and timing maybe from late next year into 2024 and here we go again with demand outstripping supply. Sidelined domestic buyers will be accumulating cash into a softer price environment and ready to buy just as immigration fans supply shortages. That could also mean that inflation relief derived from housing and spillover effects may be transitory.

- Labour markets will welcome the higher targets over time by comparison to soft domestic demographic drivers and skills shortages, but we’ll have to get through a recession’s likely impact upon the labour market first.

- Longer run neutral rate estimates may be higher due to the workforce impact upon potential GDP growth.

- Canada had better improve integration of new arrivals and distributing them across the country. Fast. This ages old challenge is nothing new. Neither is the need to improve.

- The move supports remaining DB pensions and a need for infrastructure spending especially in the handful of cities that attract the most immigration.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.