ON DECK FOR WEDNESDAY, MAY 4

KEY POINTS:

- Oil rallies as EU finds solution to banning Russian oil

- EU photobombs Powell & Co…

- …as perhaps the day’s main event….

- …versus expectations for the FOMC to stick to its script…

- ...with a 50bps hike, faster guidance and implementation of roll-off plans

- India sacrifices principles in favour of deeper oil discounts

- RBI delivers an unscheduled hike

- NZ wages give the kiwi dollar a boost

- Australian consumers lift the A$

- Trade figures from Germany, Canada and the US

- ADP probably won’t affect expectations for nonfarm payrolls

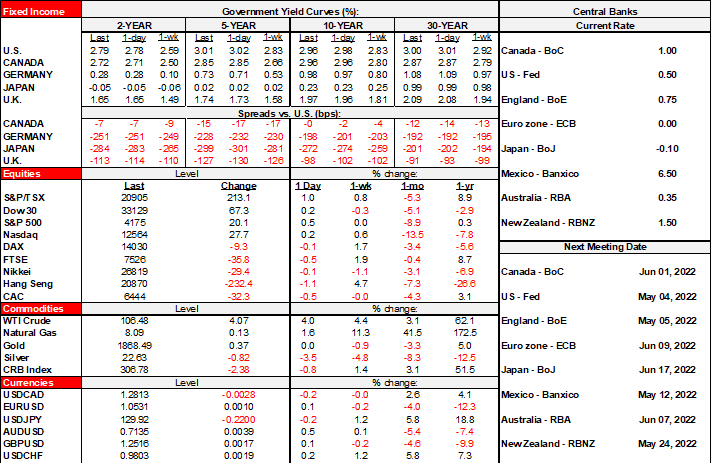

There are a few sideshows, but the overwhelming focus across global markets will clearly be on the Fed today while the EU attempts to photobomb Powell & Co and ahead of tomorrow’s OPEC+ meeting. Risk appetite is mixed. US equity futures are up by about ½% with the TSX flat, while European cash markets are off by up to -½%. US Ts are slightly bear flattening with 2s up 1–2bps and 10s down ~1bps. European curves are up by about 2bps across maturities and most countries except for more of a bear flattening move in countries like Italy and Spain. The USD is very slightly weaker on balance with the A$/NZ$, CAD and MXN leading the gainers along with the rupee (RBI, see below).

Oil prices are up by about US$4 because the EU formally announced plans to ban imports of Russian oil within six months and refined products by year end. It also added more sanctions to related services. Two minor loopholes will be that Hungary and Slovakia will be given until the end of 2023 to join the sanctions which might avoid vetoes when it goes to an all EU-27 vote. If it works, then the carve out for these two countries will be a neat solution that also conveniently lands the day before the OPEC+ decision and today’s technical committee weigh-in.

There are myriad risks. One is whether Russia just finds other outlets and to that effect India, which has never taken a stance against Russia’s invasion, is signalling it will keep buying but wants deeper discounts to around $70/barrel. India has for some time now been ramping up oil imports from Russia; isn’t that sweet to see opportunism over sacrificed principles, though we’ll see if it invites sanctions upon itself and perhaps deservedly so. Russia is getting its support in one form or another from countries ranging from China to India and the Middle East, each of which has its own frictions with neighbours and in many instances weak records on human rights. Second, will Russia retaliate and in what form.

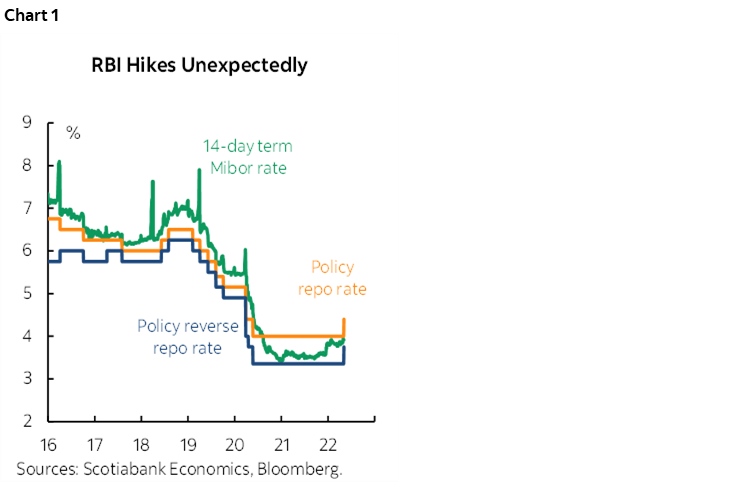

Speaking of India, the RBI surprised markets with an unscheduled emergency rate hike this morning. Wait, I thought cheaper oil was about to flood in, no? Meh. The repurchase rate was hiked by 40bps to 4.4% and the cash reserve ratio by 50bps to 4.5% (chart 1). That’s the first rate hike since mid-2018. The move was partly because the RBI wasn’t scheduled to meet until June 8th and Governor Shaktikanta Das emphasized that “Inflation must be tamed” while pointing to the next CPI report for April due out on May 12th as a likely hot one (~7% y/y prior).

The kiwi dollar got some support overnight from the Q1 release of strong wage growth. It climbed to 1.9% q/q SA non-annualized (1.2% consensus).

The consumer gave the A$ a lift when retail ales roughly tripled consensus expectations (1.6% m/m, 0.5% consensus).

Germany gave back a little more of the prior month’s surge in exports than expected and volumes were weaker than the headline numbers. They fell by 3.3% m/m in March (-2.1% consensus) with the prior month’s 6.4% gain revised down a touch to 6.2%. Imports were strong with a gain of 3.4% m/m (prior revised up to 4.7%). Controlling for price effects, exports were down by 6.8% m/m (5.1% prior) and imports were 2% lower (3.6% prior).

The FOMC statement will be at 2pmET and Chair Powell’s presser will start 30 minutes later. The script has been set. Powell said on April 21st that +50bps would be considered which is basically central bank language for saying mark it down as done. The minutes to the March meeting had “many” participants advocating a 50bps move at this meeting. We haven’t heard enough members deviating from that guidance since then. The Fed’s not in surprise mode into the meeting so while a dissenter or two is possible, I wouldn’t expect 75bps+. I would expect them to repeat that the committee wishes to get to neutral “expeditiously” and that “one or more” 50bps moves are likely (probably raised to “more” at this meeting). If he repeats that guidance then 75bps would be dashed for the next meeting as well.

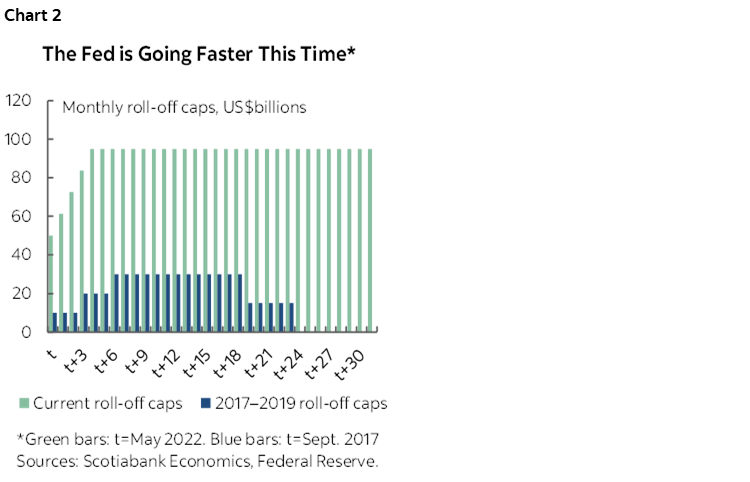

We’ll probably also get the implementation of plans to shrink the SOMA portfolio as outlined in the April 6th minutes to the March 16th meeting. Recall the outlines of that plan included getting up to peak roll-off caps on maturing Treasuries ($60B/mth) and MBS ($35B/mth) totalling US$95B/month within three months which is much faster than the last time around (chart 2 with an interpolated path over the first three months until we know better). The starting pace is uncertain, but the compressed time internal is what matters. They said they would consider outright MBS sales once unwinding is “well underway” and plough the proceeds back into Treasuries toward the goal of having a cleaner balance sheet. There are no end targets being offered for the size of the SOMA portfolio or optimal reserves because, well, neither the Fed or anyone else really knows where those points may be! Expect similar open-endedness tomorrow.

There will be no fresh forecasts with this meeting. They will arrive with the updated SEP in June including a fresh Rorschach plot. That said, I’d expect the presser to emphasize the solid details under the hood in terms of Q1 US GDP and to repeat earlier optimism on the outlook for the economy. Rhetoric around inflation risk may be further amplified given the arrival of further serial supply shocks since the March 16th meeting.

Powell is likely to discuss leaning toward a faster up-front pace of hikes than the last projections that saw fed funds at 2% by year-end, but markets have already blown well past that anyway and so the incremental impact on markets may be minor/nothing. It would be more of a surprise to market pricing if Powell sounded more cautious, but I think the Fed’s singular focus is upon bringing down inflation through expedited exits.

Canada’s merchandise trade surplus in March (8:30amET) is likely to sharply widen as the reflection of the sharply wider US merchandise deficit and given high commodity prices. Canada’s import leakage effect will update out understanding of the implications for Q1 GDP growth. The US will take the prior release for the merchandise component and tack on a usually fairly stable services surplus to give the whole trade picture (8:30amET). ADP payrolls for April (8:15amET) will probably just be mild ecotainment unless it’s a real shocker to the +383k consensus, and even then, we’ve had several in the pandemic alone that have been total head fakes ahead of nonfarm.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.