ON DECK FOR THURSDAY, MAY 19

KEY POINTS:

- Risk-off sentiment continues

- Dollar softens as fed funds pricing eases

- Mixed signals from China’s move to rebuild oil reserves

- Alberta’s Premier the latest casualty of divided conservatives

- Limited US data

- Australian jobs turn up flat, markets ignore

- Philippines central bank commences hiking cycle

Don’t look.

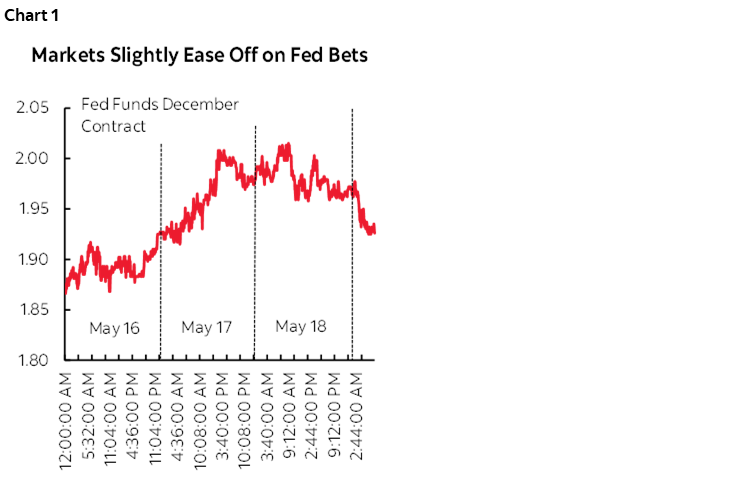

Ack, you silly beans, you looked! I told you not to! Well, ok then, here it is. Stocks are getting hit again and if this holds then US equities will be officially in the –20% zone from the early year peak which meets many definitions of a material correction. US and Canadian equity futures are down by about 1% which is less of a decline than earlier this morning. European cash markets are down by 1% to 2%. Asian indices ranged from up to ½% gains in mainland China to declines in the 1% to 2 ½% ballpark elsewhere. Sovereign bond yields are lower by 7–9bps across Treasuries, 5–9bps across Canada’s curve and 2–11bps across gilts and EGBs. WTI oil is down another 2¾% which is also less than before China headlines. The USD is broadly softer against major crosses despite risk-off sentiment and in part as fed funds futures ease off hiking bets somewhat (chart 1) on the theory that more rapid tightening of financial conditions may do more of the Fed’s work if it sticks.

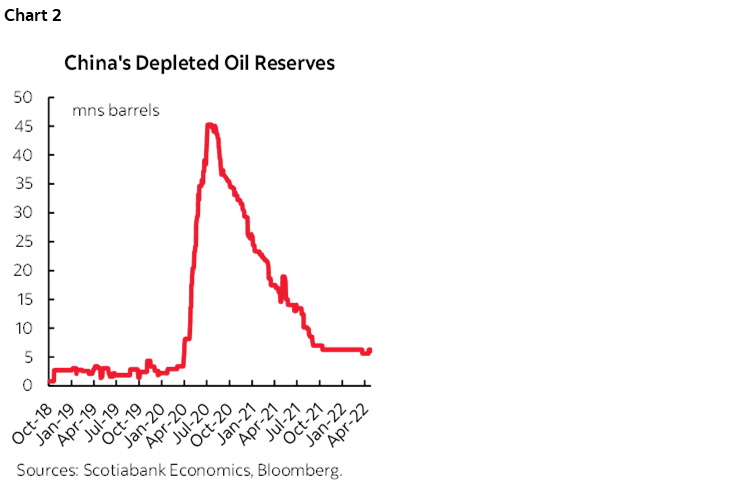

There is more evidence that China is going rogue on much of the rest of the world’s move to ban imports of Russian oil. Principles and values be darned, as cold hard economic opportunism is China’s guiding light. Anonymous folks are telling press outlets that China is seeking to buy more Russian oil no doubt at a discount in order to rebuild its depleted reserves. China’s oil stockpile is at its lowest since mid-April 2020 after which it soared as the pandemic swept the world (chart 2). There are several possibly important implications here and what may shake out of the mixture is uncertain.

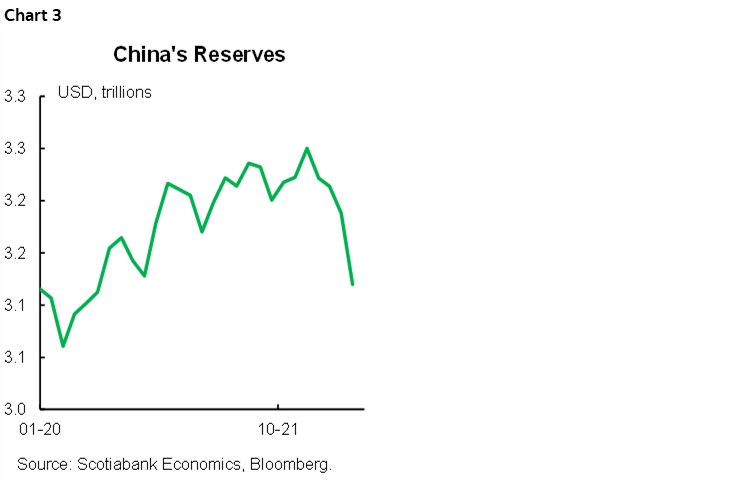

- In one sense that’s a negative in that it is likely to raise tensions with China’s key export markets and may invite some forms of retaliation because it goes against what they are doing in terms of banning Russian oil imports. This piece in this morning’s Wall Street Journal may support this narrative as it indicates China’s leadership passed a directive in March to ban overseas holdings of real estate or financial assets by senior officials. China may be pursuing steps to shield officials from what happened to Russian oligarchs. That may serve as a warning sign that greater global tensions may lie ahead. China’s total foreign reserves have also been falling of late (chart 3) with FX policy to stem the yuan’s slide in the mixture of influences. Telling deep pocketed officials that benefit from party ties to sell dollar assets and repatriate into yuan may carry the indirect benefit of stemming the yuan’s slide.

- In another sense, if China wants to rebuild depleted oil reserves, then it adds to signs that the economy is expected to rebound as restrictions are eased and further stimulus supports may be forthcoming.

- To add a third dimension, depending upon how much China wishes to buy, it could also mean renewed upward pressure upon oil prices but that’s not evident this morning! Unless they’d be falling faster if not for China’s actions.

Data isn’t really mattering in all of this and we won’t get any earnings bombs today. Australia’s front-end had been rallying before jobs hit and the release was largely shaken off. Jobs were flat (+4k) as a big gain in full-time jobs (+92k) was offset by a big drop in part-time jobs (-88k). That pushed the participation rate down a tick to 66.3%. Slightly positive revisions to jobs were enough to dip the unemployment rate to 3.9% which then held steady in April.

Bangko Sentral ng Pilipinas raised its overnight rate by 25bps to 2¼% for its first hike as expected but also raised its standing overnight deposit rate by 25bps against the consensus median expectation.

Light US data is likely to be largely ignored today. The Philly Fed’s gauge for May (8:30amET) fell 15 points to 2.6 as new orders climbed, shipments rose to their highest reading since October 2020, but employment decelerated while prices paid and received eased off somewhat especially on the paid side. Weekly initial jobless claims back up a bit to 218k last week (197k prior revised down from 203k) while continuing jobless claims continue to decline (1.317 million from 1.342 million before). April’s existing home sales arrive later this morning and are expected to slip (10amET).

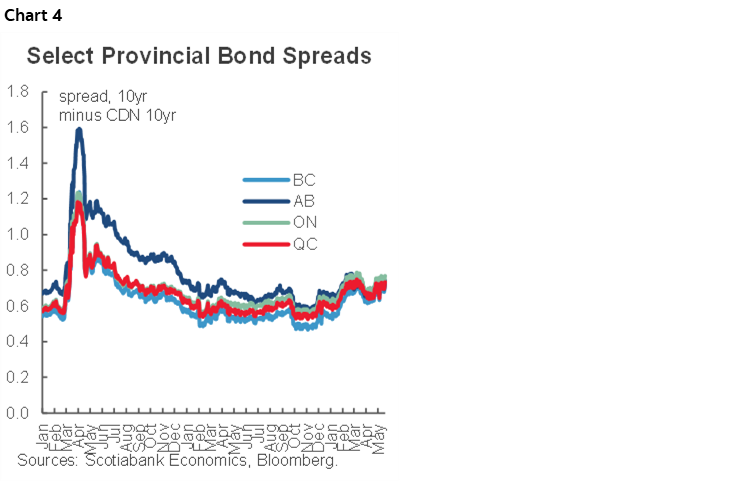

Deeply divided Canadian conservatives took down another one of their leaders last evening. Alberta Premier Kenney—one of the most recognizable faces in Canadian politics in a province that’s once again enjoying booming oil prices—lost a leadership review which will mean that the United Conservative Party (an oxymoron?) will launch a campaign for his replacement ahead of the election to be held next May 29th, 2023 unless the provincial Legislature is dissolved before then. The reason they took him down? Because even though there were ups and downs in Kenney’s approach to the pandemic, enough Conservatives were against the public health restrictions he implemented at times. A near tie between the UCP and left leaning NDP in the polls perhaps didn’t help much either. As a sidebar, this may be further evidence that should the pandemic take a nastier turn in future, say with vaccine evading and more harmful variants, then implementation of public health restrictions may be very unlikely regardless of the consequences. It also indicates that Conservatives are getting more and more deeply divided across the land by contrast to the Liberal-NDP pact that has a lock on the center-left vote. Alberta’s provincial bonds have many selling points and their spreads have performed similarly to other larger Canadian provinces of late (chart 4).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.