ON DECK FOR FRIDAY, MAY 13

KEY POINTS:

- Friday the 13th brings good luck to markets

- It wasn’t new, but markets like to constantly hear Powell rule out bigger rate moves

- China’s financing cools more than expected…

- …and a higher yuan fix was set…

- …ahead of the PBOC’s decision and more data

- Peru’s central bank hiked as expected

- Light US data on tap

Friday the 13th brings good luck to any superstitious investors out there after all! Who knew!?

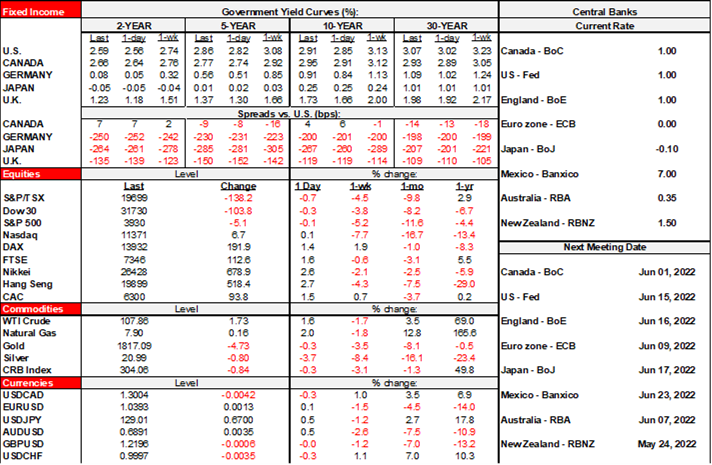

Stocks are broadly higher with US snp futures up by about 1%, TSX futures up by just under 1% and European cash markets up by 1 – 1½%. This follows an Asian overnight session that saw broad-based gains led by the Nikkei 225 and Hang Seng that were both up by about 2¾%. Sovereign bond yields are under upward pressure with US Ts about 2bps cheaper in 2s and about 6–7bps at the long end. 10 year gilts and EGBs are also about 5–6bps higher and a little more in Italy. The USD is roughly unchanged on balance as dips by the yen and sterling offset gains across most other major crosses. Oil is up by about 1½%.

I don't see major fresh catalysts to these moves. We're asked to believe that Powell's reaffirmation of 50bps moves while ruling out 75bps hikes offers relief, but if so, investors weren't listening when he previously said it. Even Bullard is not actively thinking of 75bps moves.

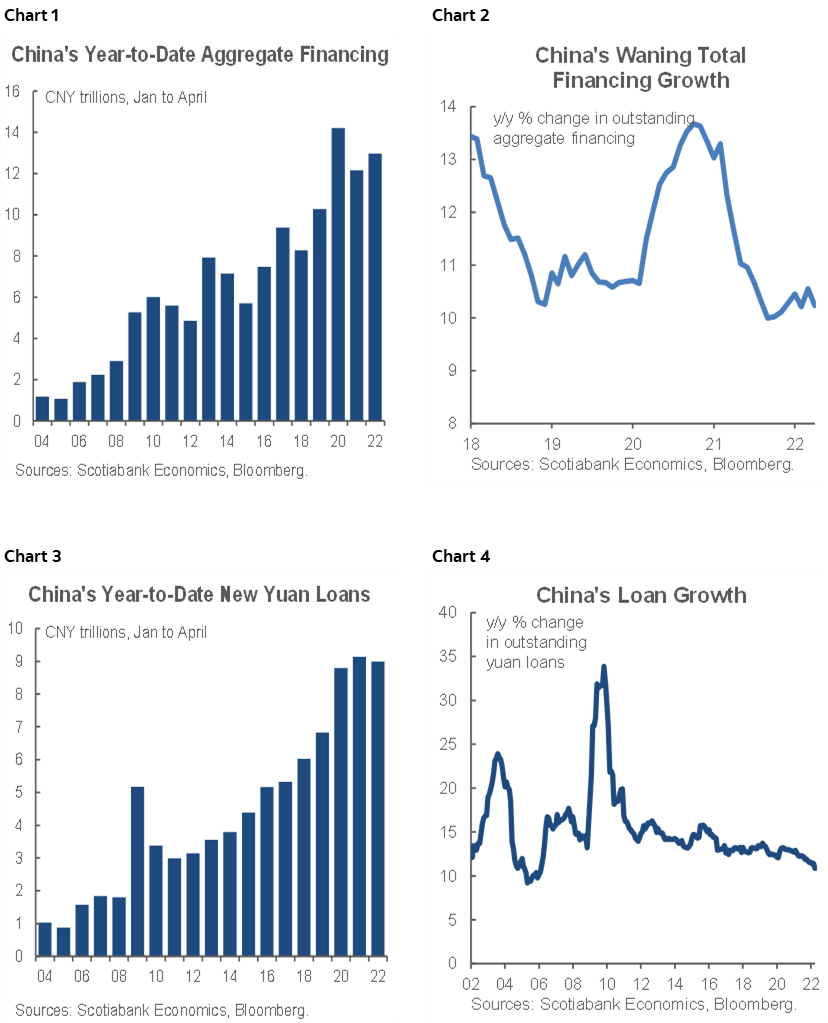

Maybe China is also playing into this with markets speculating upon the end of lockdowns while policy and data exert influences. China’s financing figures sharply disappointed expectations and might contribute to easing bets as China’s 2-year yield was slightly lower overnight while a higher yuan fix drove the currency a bit higher. April’s readings indicate total financing was up by only 910 billion yuan (2.2 trillion consensus) and core domestic currency loans were up by 645 billion (1.53 trillion consensus). Year-to-date flows are shown in chart 1 and the year-over-year growth rate in total outstanding balances across all financing products is shown in chart 2. Charts 3 and 4 do likewise just for yuan-denominated loans. The y/y growth rate of the total stock of all financing products is riding at multi-year lows. While the amount by which the financing activity slowed was surprising, the direction is not given Covid Zero lockdowns. Whether this tips the balance in favour of a PBOC rate cut will have to wait until Sunday night when the central bank sets the 1-year Medium-Term Lending Facility Rate just before a batch of readings on the economy land.

Icymi, Peru’s central bank did indeed hike by 50bps to a 5% reference rate last evening. Other overnight developments were minor including Norway’s GDP that landed on the screws for Q1 (-0.6% q/q SA) but set up a nice built-in effect into Q2 with March GDP up 1% m/m (0.8% consensus) and with a positive revision.

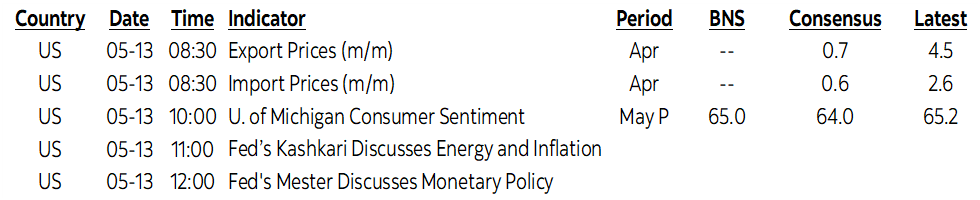

There isn’t really anything on tap into the N.A. session that is likely to materially impact broad risk appetite. Twitter is getting hammered (but Tesla shareholders are rejoicing) as Musk’s takeover is put on at least temporary hold. US import and export prices for April will be updated at 8:30amET and then the University of Michigan’s consumer sentiment for May is due at 10amET and is expected to slip. There will also be limited Fed- and ECB-speak including the Fed’s Kashkari and ECB’s Nagel at 11amET and then the Fed’s Mester and ECB’s Schnabel at 12pmET.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.