ON DECK FOR THURSDAY, MAY 12

KEY POINTS:

- Risk-off sentiment on off-calendar risk, ongoing effects of US CPI

- Euro drops as Finland seeks NATO membership

- UK economy posts softer than expected readings

- Banxico expected to hike today

- BoC will probably state the obvious about commodities and Canada

- More US inflation readings on the way

Off-calendar risk is combining with spillover effects of yesterday’s US inflation readings to continue to drive risk-off sentiment. Sovereign bond yields are broadly lower by 4–7bps in a US Ts flattener move while gilts and EGBs rally by a little more. The USD is broadly stronger along with the yen and Swiss franc. Equities are down. Again. US and Canadian equity futures are off by about ½% – 1% with European cash markets mostly down by 2%+. Oil is down by over 1%.

China’s Sunac China Holdings defaulted on a dollar denominated bond as a sign of ongoing struggles in its property finance market. Some view it as a fresh catalyst to a wave of other defaults in the property sector.

The euro dropped on headlines that Finland’s government threw support behind joining NATO and the predictable objections from Russia that ensued. Finland and Sweden are expected to take formal steps toward membership soon which will take time for all of NATO’s members to ratify.

The UK economy posted a batch of generally softer than expected readings this morning. Q1 GDP grew 0.8% (consensus 1%) as consumption was the lone bright spot and even that disappointed. An estimate of monthly GDP ended the quarter at -0.1% m/m to set up a soft Q2. Industrial output fell 0.2% m/m in March, a services index retreated by 0.2% and the lone bright spot was construction output at +1.7% m/m.

Swedish inflation was a bit firmer than expected with underlying CPI at 0.6% m/m (0.4% consensus) and 6.4% y/y (6.2% consensus).

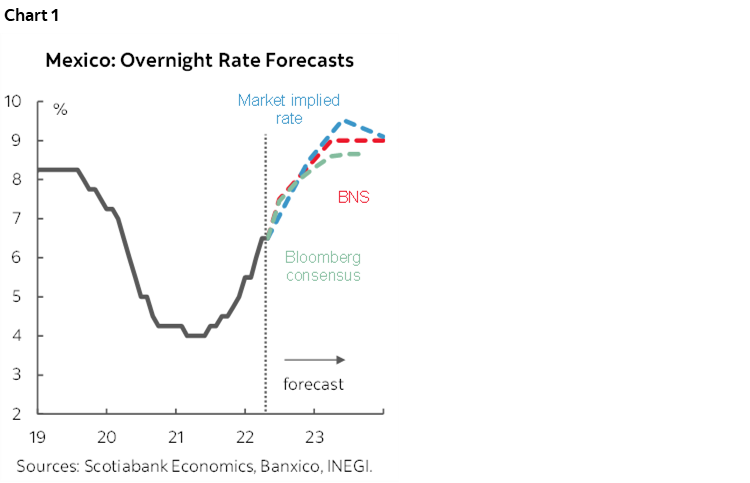

Banxico is expected to hike by 50bps this afternoon according to 22 of 23 forecasters (2pmET). Markets and economists view the central bank as still facing a steep hill to climb in significant part due to being pulled along by the Fed (chart 1).

US producer price inflation for April is expected to be cooler than March but remain elevated. Prices are estimated to have risen by about ½% m/m with prices ex-food and energy perhaps a touch firmer than that. US weekly initial jobless claims are due at the same time (8:30amET).

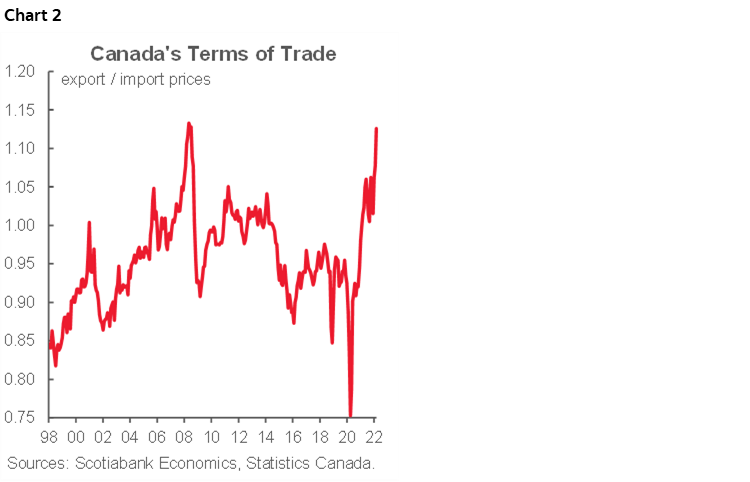

BoC DepGov Gravelle speaks on commodities and the impact on growth and inflation in Canada (11:35amET). There are no prizes for thinking that he’ll say hot commodities are a plus for Canada and through the terms of trade effects an imported lift to incomes that all else equal benefit growth and raise inflationary pressures (chart 2). The BoC has recently adopted the practice of skipping pressers (Rogers, Schembri, Gravelle today).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.