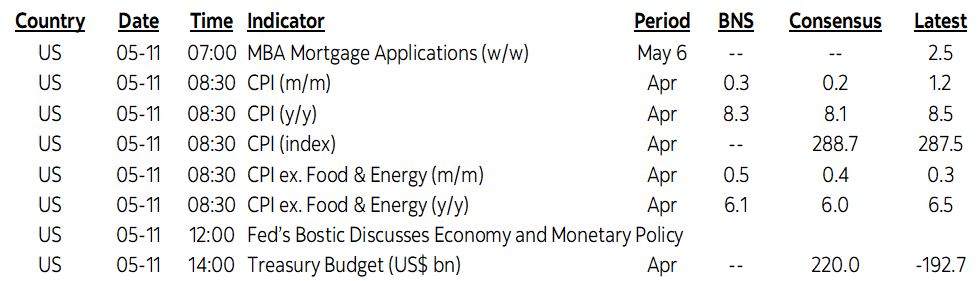

ON DECK FOR WEDNESDAY, MAY 11

KEY POINTS:

- Markets hoping for a soft US inflation print

- US CPI expectations

- The Fed’s summertime narrative is set regardless of today’s inflation reading

- Lagarde repeats guidance a hike could quickly follow the end of APP buying in July

- Chinese core inflation decelerates

- Oil up as Shanghai lockdowns cut new cases

- Bank Negara Malaysia surprises with a hike and hawkish guidance

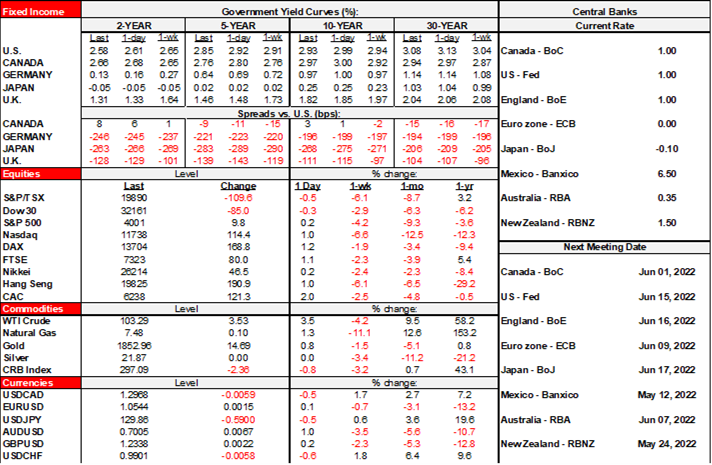

Another day, another inflation wiggle to feed the obsession of our times. Markets may be positioning themselves for a soft print with sovereign curves richer across the board and the USD weaker against all crosses. Stocks are trying to add to a comeback with US futures up by about 1%, TSX futures up by ¾% and European cash markets up by either side of 1%. Oil is about $3 higher and is getting an assist from Shanghai’s reporting that new COVID-19 cases dropped by half which I suppose happens when you strip everyone of their last shreds of dignity and rights.

US CPI inflation for April (8:30amET) will be the main draw and a distant second to that will be more ECB- and Fed-speak. Lagarde repeated that the first rate hike could come as soon as a few weeks after ending APP purchases and hence intimated that could happen by the July 21st meeting.

On US inflation, I’m a little higher than consensus on headline and core CPI but not by much this time. The main rationale is offered in the section on US inflation in the week ahead write-up.

- As for estimates, consensus expects 0.2% m/m for headline CPI but estimates are skewed higher including my guesstimate of 0.3% m/m SA. The year-over-year rate is expected to pull back to 8.1% (8.5% prior) and I’m at 8.3%. Core inflation is expected to rise by 0.4% m/m with the distribution skewed toward a higher reading including my estimate of 0.5% m/m. The year-over-year core rate is expected to ease to 6% y/y from 6.5% and I’m at 6.1%.

- Year-ago base effect shifts will lower the inflation rate. For that not to happen the price gain would have to be eight-tenths m/m NSA or greater which seems unlikely. As on the way up, pay more attention to m/m SAAR for evidence of inflationary pressures at the margin. This measure has been steadily accelerating over the past three months and hit 16% in the prior CPI report for March.

- Seasonality should be a light influence on m/m NSA and add only a touch to the y/y rate.

- Gasoline prices were off a bit in NSA terms and should subtract a few tenths in weighted m/m SA terms.

- Spot natural gas prices were up by about one-third m/m NSA and SA and could offset the gasoline drag.

- Used vehicle measures were divided this time but the one I think matters most should add a bit to m/m SA.

- New vehicle prices were up and should add a tenth or two. The BLS will change its measure of this (see below).

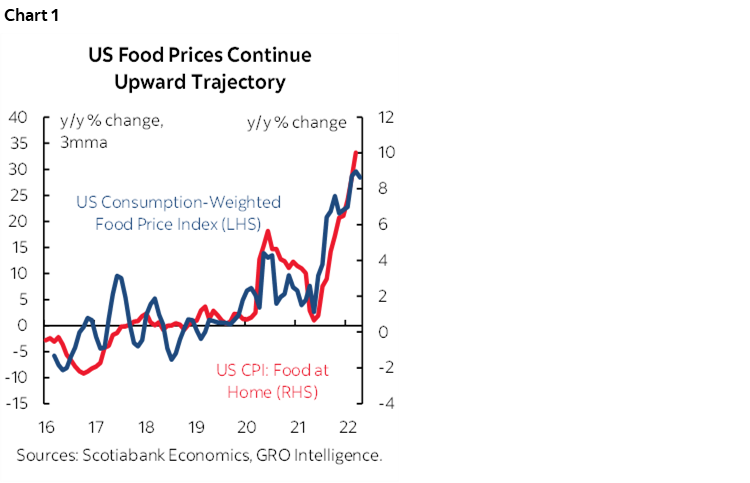

- Food prices are a wildcard at the consumer level but I’ve factored in a small further rise to the strong upward trend (chart 1).

- I’ve assumed a further reopening/normalization effect on services prices.

One wildcard uncertainty concerns methodological changes this time that merit caution into this one. With April CPI the BLS will formally switch to the measure of new vehicle prices tracked by JD Power. That index was up by 3.4% m/m NSA at a 4.1% weight so it would provide a small NSA contribution that is mostly retained after considering April SA factors. Motorcycle prices will drop out of the measure this is replacing and the new vehicle price category will break out cars and trucks but if I understand correctly then they won’t combine the two into one category.

For my two cents, nothing in this report will affect nearer term decisions by the Fed that has teed up a 50bps hike at each of the next two meetings.

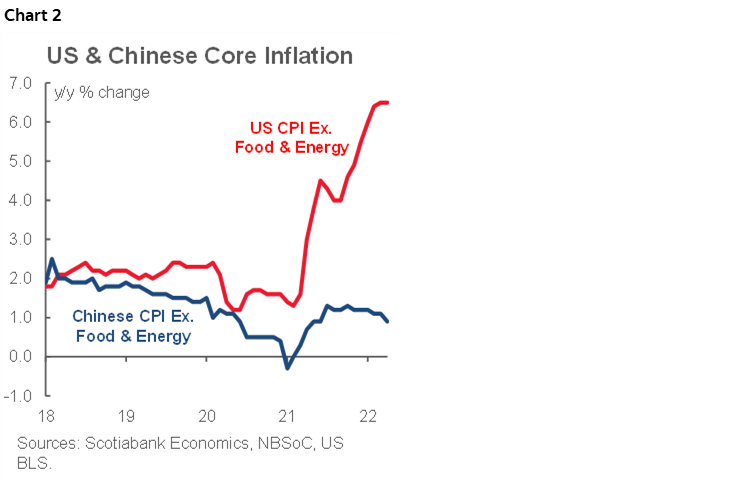

China’s inflation rate picked up to 2.1% y/y (1.5% prior, 1.8% consensus) but solely due to commodity pressures and namely oil. Core inflation weakened to 0.9% y/y (1.1% prior) and has been trending lower this year. The diverging pattern of US versus Chinese core inflation explains the relative monetary policy divergence and yuan weakness (chart 2). The question will be how quickly Chinese core inflation may rebound as the shackles get loosened.

Bank Negara Malaysia hiked 25bps to a 2% overnight policy rate that only about one-quarter of consensus expected and accompanied this with hawkish forward guidance pointing to further hikes.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.