ON DECK FOR THURSDAY, MARCH 3

KEY POINTS:

- Funding markets continue to hold firm

- BoC’s Macklem may provide reinvestment guidance…

- …after his expected hawkish message yesterday

- Fed’s Powell to repeat the same core messages on day two

- US ISM-services expected to improve as omicron fades

- Nonfarm payrolls preview

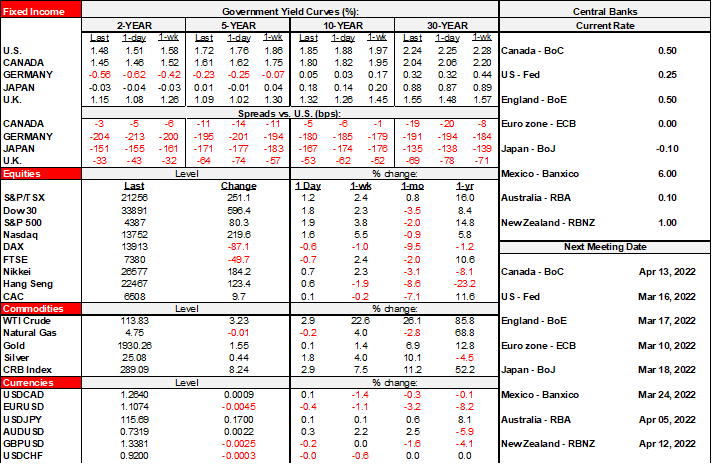

We’re back to mild risk-off sentiment this morning. Stocks are little changed (NA futures) to down as much as 2% in Europe except Paris. US Ts are slightly bid with yields ~3bps lower with Canada slightly underperforming and versus for sale signs springing up all over European fixed income land. Gilts are performing the worst with yields up 5–7bps. The USD is slightly firmer on balance, but with CAD, the A$ and one or two others holding their own. And yes, oil is up again by about 3–4% or so for a US$38/barrel rise in WTI so far this year and 75% higher than at the start of December. Regular unleaded gasoline is up about 11% so far this year and the highest since July 2014.

The main calendar-based focal points will include round two of Chair Powell’s testimony this time before the Senate Banking Committee (10amET), and appearances by BoC Governor Macklem.

I would expect Powell to reaffirm his guidance that included:

- they’ll hike 25bps in two weeks;

- they are open to 50 moves if inflation surprises higher for longer;

- that they plan a series of rate hikes;

- that the war in Ukraine represents significant risk to the ultimate path;

- that they will further discuss but not finalize balance sheet plans at the March meeting and therefore won’t have a decision at the ready on reinvestment plans.

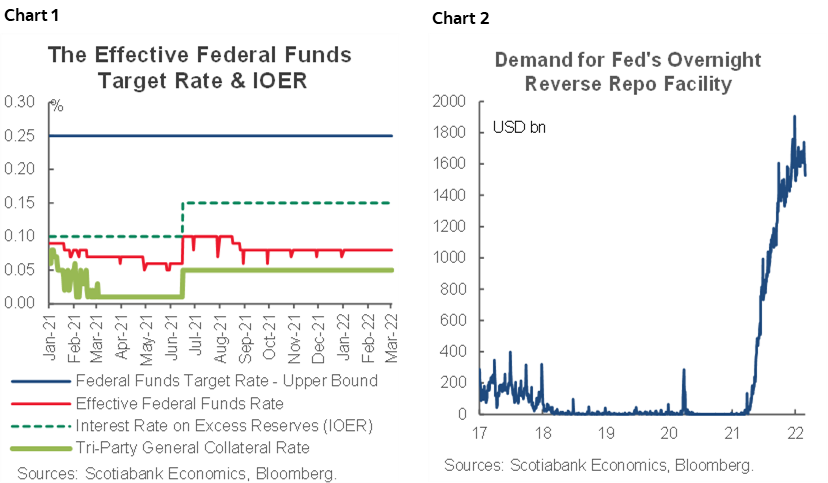

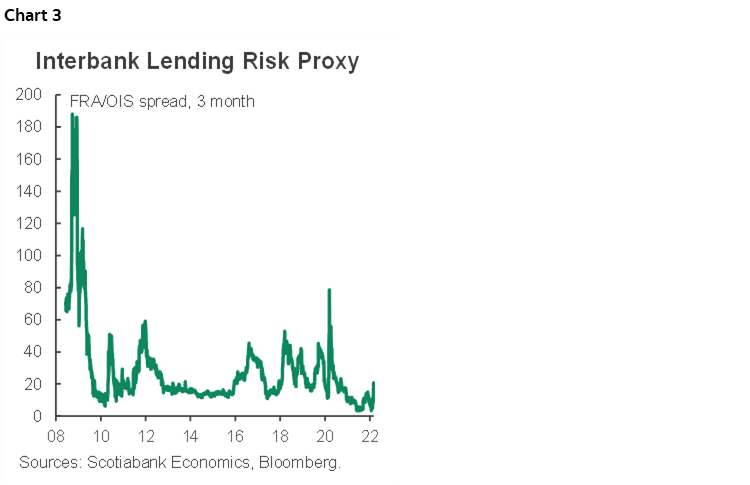

We’ll see how the Fed reacts if inflation goes double digits…. In any event, his remark on the war being something whose effects will be with us for years is likely spot on and is an argument for “being nimble” as he puts it while making necessary decisions along the way. The Fed tentatively believes it has the market infrastructure in place (e.g. standing repo facility) to avert a funding shock/crisis driven directly or indirectly by the war in Ukraine but obviously we’ll be testing scenarios and limits to this going forward. So far, so good. The Fed is retaining control over effective fed funds with its relative policy rates corridor (chart 1), it’s large repo book (chart 2) and with interbank funding markets remaining generally calm (chart 3).

Then it’s over to BoC Governor Macklem after the BoC met our expectations for a hawkish hike that emphasized stronger GDP growth than they expected, firmer oil prices with terms of trade implications and greater upward pressure upon inflation (recap here). His speech and presser today may lay out parameters around reinvestment plans going forward. If it doesn’t, then reducing reinvestment at the April meeting is probably not on. I’d expect him to repeat the main messaging in yesterday’s statement, but also watch for remarks on pace and goalposts. By the time the parliamentary testimony rolls around afterward (3:30pmET) he’ll be spent so don’t even bother with it. It’s usually a rather tedious affair in any event.

Limited data risk is also on tap in the US. Expected improvement in the service sector is the main highlight when ISM-services for February arrives (10amET). Weekly jobless claims (8:30amET) shouldn’t matter a whole lot given they are between nonfarm reference periods. Ditto for factory orders in January that should follow the 1.6% rise in durable goods orders at a somewhat softer pace held back by nondurables (10amET).

The week will close with US payrolls tomorrow (Canada is off-cycle this time with jobs out the following Friday). It will probably be the least consequential jobs report in quite some time. The change between reference periods will be stale in relation to fresh developments like the war and surging oil. The Fed’s script for March is largely set with a very high bar set against changing. For what it’s worth, here’s the run-down on expectations:

- Consensus expects +418k. My estimate is 450k and hence not materially different this time around.

- Most estimates are within about a 300–500k m/m range.

- The very thin tails are set at +80k and +730k.

- the mean and the median estimates are similar which indicates no real skewness.

- As for drivers, mobility improved between reference periods, fewer people indicated they were

- the standard deviation is 112k and the 90% confidence interval on payroll changes is +/- 110k.

- the ‘whisper’ number (to which anyone with a Bloomberg account can contribute…) is 331k.

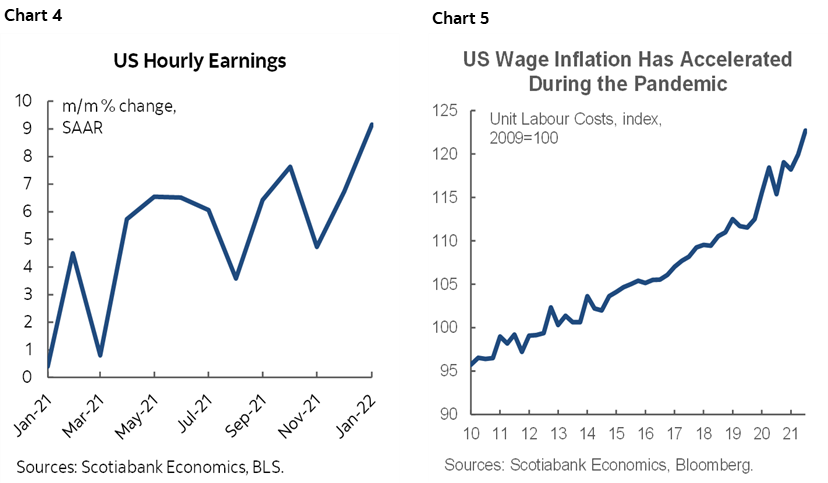

- Key will be wages with growth inching toward 6% y/y and at a similar annualized m/m pace dating straight back to last April alongside tepid productivity growth and hence accelerating unit labour costs.

As charts 4 and 5 demonstrate the US is experiencing accelerating gains in wages and overall employment costs adjusted for productivity. The accelerating trends in tightening labour markets indicate that momentum is shifting away from real wage declines toward at least holding even with inflationary pressures if not exceeding them and especially on a productivity-adjusted basis.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.