ON DECK FOR TUESDAY, MARCH 29

KEY POINTS:

- Risk-on sentiment hoping for peace behind the headlines…

- …but naively so?

- Caveats to Dudley’s warning about US recession risk

- US consumer confidence probably fell

- PBOC keeps injecting liquidity

- Chile’s central bank expected to hike

Risk-on sentiment is being partly driven by what superficially appear to be constructive headlines coming out of negotiations between Russia and Ukraine (see below). US equity futures are up by around 1% across benchmarks, TSX futures are slightly negative and weighed down by the headline effects on aided by oil prices that are off by about $6, and European cash markets are up by 1–3% after overnight Asian markets saw gains in Tokyo and Seoul while mainland China slipped. Sovereign bond yields were under upward pressure before the Ukraine headlines, but now they are more mixed. US yields are down by 1–5bps as the 2s10s curve bull flattens. Canada’s curve is richer by 3–4bps. Gilts and EGBs are underperforming with the gilts curve bear steepening and the bunds curve slightly bear flattening The USD is slightly weaker as the euro and related crosses lead the gainers.

Markets are reacting to constructive headlines coming out of Russia, but caution is required. Russia is reportedly curtailing activity near Kyiv and Chernihv, citing talks are in the "practical phase" and its negotiator is noting that there could be a Putin-Zelenskiy meeting. This follows previous indications that the Russians are focusing efforts upon eastern Ukraine, no doubt in part because of Russia’s disastrous experience trying to take Kyiv. These are the bureaucrats talking, mind you, and we know from past instances that it's only what Putin thinks that matters when he remarks on the news from his negotiators. Putin has had a past tendency to douse constructive talk by saying Ukraine is not meeting his demands. Talking is constructive, I suppose, but it's not the talk from the Russian negotiator that we need to hear. One possibility is that curtailing activity around Kyiv is a set up to reinforcing the demands around Donetsk and Luhansk and other demands that Ukraine has consistently rejected.

One would think it’s doubtful that there will be major, durable progress in the talks given that Putin has regularly repeated his aims. They include Ukraine being the first to stop all military action, Ukraine enshrining neutrality in its constitution, Ukraine officially acknowledging that Crimea belongs to Russia and for Ukraine to recognize the Donetsk and Luhansk regions as independent states. Ukraine has routinely rejected this package of demands and it seems unlikely it would say yes to all of them. In any event, most of us are certainly not Kremlinologists and it's a mugs game trying to outguess habitual liars and miscreants like Putin, so it’s likely wise to caution against the market reaction and resort to watching for tangible measures led by Putin while wondering what’s up his sleeve next.

US consumer confidence (10amET) will inform initial perspectives on how the war’s effects on inflation and the Fed’s hawkish pivot are impacting consumer attitudes net of a buoyant job market. Soaring gas prices will likely drop both the present and expected future conditions indices while putting further upward pressure upon one-year ahead inflation expectations that according to this measure are already running at 7% which is the highest since July 2008.

Chile’s central bank is expected to raise its overnight rate by 175bps late this afternoon (5pmET). Consensus runs from 150–200bps. Scotia’s Chilean economist is at the bottom of this range, while the most votes are assigned to the upper end of that range.

The PBOC continues to inject liquidity into the financial system through ongoing reverse repo transactions. 150 billion yuan of 7-day reverse repo flows netted 130 billion given modest maturities. 340 billion matures by one week from tomorrow and so gross transactions will need to remain high. The overnight repo rate has fallen to 1.69% from 2% last Thursday. While the 7-day repo rate slipped a touch overnight, it’s up by about 14bps over this same period.

Australian retail sales doubled consensus expectations (1.8% m/m, consensus 0.9%) with a small dent from a slight downward revision. This is for February, so big deal given it pre-dates the war’s effects. Spenders returned to restaurants (+9.7% m/m) as a covid-19 wave subsided which crowded out spending on groceries (-2.6% m/m). Strong gains were posted for clothing and household goods.

US RECESSION RISK?

When a very good and well regarded economist and past Fed official like Bill Dudley emphasizes recession risk as “virtually inevitable” it’s worth listening to (here). I think his article is definitely worth reading but differ from his views in a few key respects.

Let’s start with where I agree as I think he’s right to hold the Powell Fed accountable for its total misreading of inflation and Dudley is right to argue that the revised framework played a role in the Fed’s misreading of inflation risk and its delayed reaction. Waiting too long to adjust the policy stance now requires harsher adjustments as the Fed finally decides to act and that’s not really an entirely new criticism of Fed policy. The Fed messed up and misjudged inflation risk by being far too dismissive toward entertaining any prospect of sustained material upside risk.

Still, I feel he goes too far in drawing parallels to recessions that followed past tightening cycles and in arguing that recession is “inevitable.”

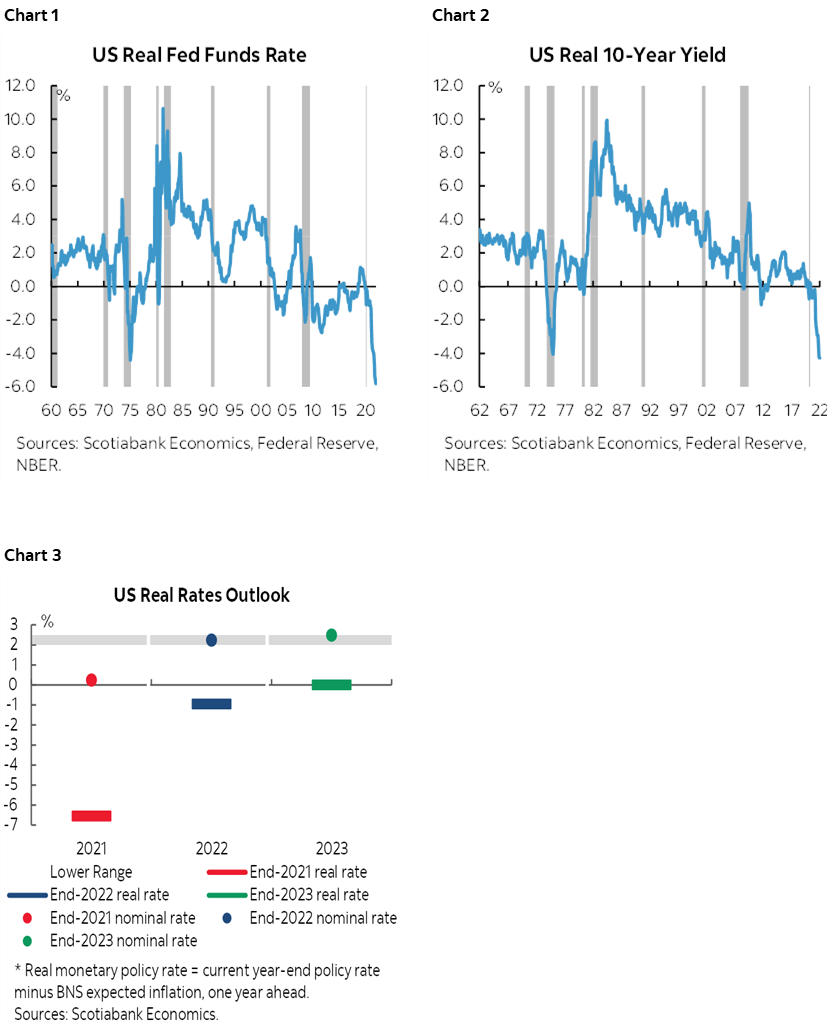

For one thing, there is the possible issue of money illusion. When reviewing past tightening cycles, it’s probably skewing the debate to look only at the nominal policy rate. We should be using real rates and ideally in a forward-looking sense by assessing expected inflation. It’s the real policy rate that is used in macroeconometric models as guides to expected future economic growth. The difference matters enormously today. We’ve never had a recession with a real policy rate (chart 1) or real US 10-year yield (chart 2) as deeply negative as at present and with the real policy rate expected to only claw back toward zero or slightly restrictive by next year (chart 3).

Second, while I agree that too many folks have dismissed inflation as entirely driven by supply-side effects and that this argument will continue to hold in future, we obviously can’t dismiss the role of supply side drivers. Some of this inflation will cool as industries grapple with addressing supply chain problems through efforts to restock, invest and hire. This is important because it’s a bit of an exaggeration to pin all of the responsibility for bringing inflation back toward target on the magnitude of Fed policy tightening when there are other factors at work in boosting inflation now and probably moderating it later. That means the Fed might not have to rely as much upon tightening and damaging the unemployment rate to bring inflation down if other factors contribute toward easing inflationary pressures. As supply chains adjust and if the war in Ukraine eventually does subside then the Fed might not have to tighten as much over time in order to ratchet inflation lower.

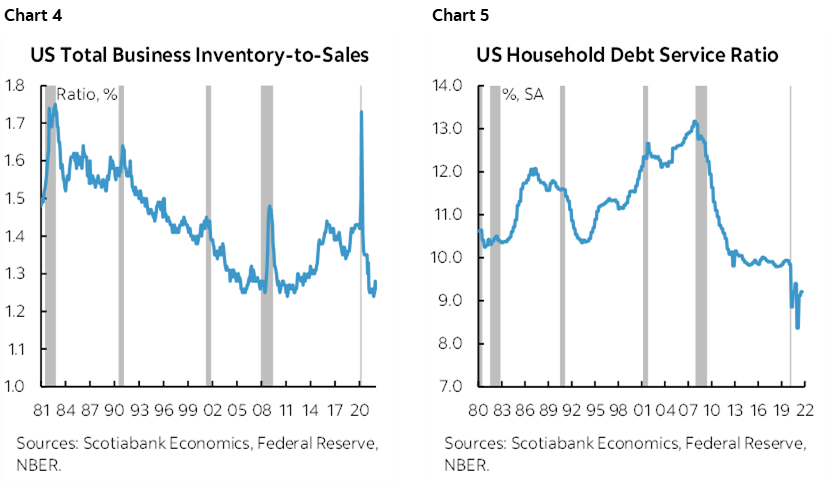

Third, most economists would draw upon a variety of recession warning signs. It would be unusual to have a recession with the inventory-to-sales ratio as low as it is now (chart 4). Ditto for the household debt service burden (chart 5).

Fourth, the so-called “Sahm Rule” he cites is a statistical observation rather than a rule. Positing that inflation will only be brought down when the unemployment rate moves up by half a point or more which tends to presage recessions invites flagging three cautions. One is the prior point about how Dudley is treating today’s inflation as virtually identical to past bouts of inflation when a good portion of it may be fundamentally different. Two is that the connection between unemployment rates and inflation (ie: the Phillips curve) has weakened over time than was the case during many of the past recessions he cites. Three is that, like any “rule”, it’s prone to being violated as circumstances change and today’s circumstances differ in multiple regards (war, pandemic, different demographics, etc).

So will a recession occur? Oh I’m sure it will. At some point. Dudley doesn’t tell us when. He can’t be reasonably expected to do so amid high uncertainty, but it’s not really telling us much that at some point coming out of a pandemic (we hope…) and experiencing a boom might at some future point give way to recession. Some day. Somewhere. That warning won’t win anyone a Nobel prize. Give a forecast or give a time, but never the two together is a classic trick in this profession and some have used it as a go-to throughout their careers. Claim victory when the forecast comes true whether it’s next year, the year after, 5 years from now or later...

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.