ON DECK FOR MONDAY, MARCH 28

KEY POINTS:

- BoC and Budget effects driving two-year GoC to underperform

- Oil drops on China lockdowns…

- …as risk centers on testing results, further possible measures

- BoJ wallops yen on freshened commitment to a 10-year yield ceiling

- PBOC injects liquidity for quarter-end, lockdown reasons

- BA.2 variant edging higher in N.A.

- BoE’s Bailey tamps down cheapening across gilts front-end

- US trade deficit holds steady, inventories constructively expanding and the Dallas Fed’s manufacturing gauge may add to ISM sentiment

- Global Week Ahead highlights

Regular publishing will resume after I was on March break vacation last week.

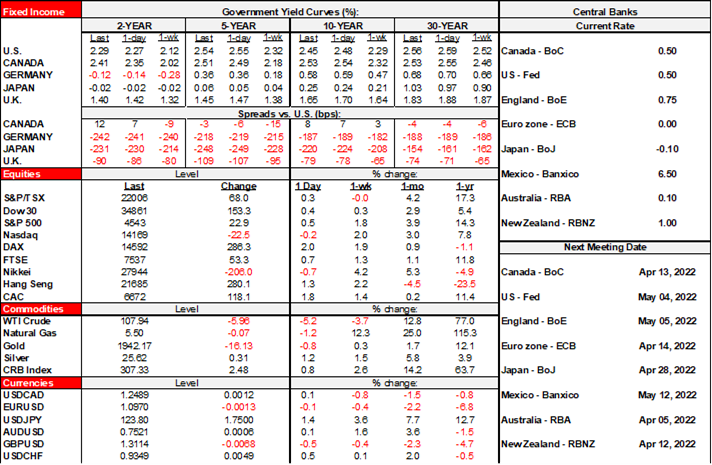

A fresh trading week is starting off with a continued bond market sell-off. Sovereign curves are mostly bear flattening with 2-year yields up ~7bps in Canada and 4bps in the US which puts Canada about 10bps above the US 2s yield. Friday’s BoC speech (here) and an anticipated heavy-spending Budget are driving this move. The gilts curve is slightly flattening as 10s are rallying by more than 2s; 2s were selling off aggressively earlier this morning before BoE Governor Bailey’s remarks (see below). EGBs are slightly bear flattening. The USD is strengthening particularly against the yen after the BoJ’s moves (see below). Oil is off by about $6/barrel likely on the effects on oil demand of China’s lockdowns (see below). Stocks are mixed with US futures up a touch, TSX futures a touch lower and following oil prices and with European cash markets up by between ¾% (London) and around 2%. Shares fell in Tokyo and Shenzhen, were up by 1.3% in HK and were flat in Shanghai and Seoul.

There are five main considerations behind the market moves to start the week:

1. The Bank of Japan stepped in to defend the upper limit of its 10-year yield target of 0% by offering to purchase unlimited amounts at a yield of 0.25% through operations over the next three days. At 0.24%, the 10-year yield has risen by about 10bps this month and hasn’t been around 0% since last August. The 10-year JGB very slightly cheapened overnight as yields pushed higher particularly at the long-end (+5bps). The announcement hit the yen that fell by just under 2% to the dollar (~122 to ~124.4). On net, JGBs mostly shook off what was just a repeated gesture to defend the 10 year yield ceiling but the signal toward expanding money supply contributed to yen softness alongside the more dominant Federal Reserve effects on the dollar.

2. Shanghai entered lockdown in order to conduct a mass COVID-19 testing operation. Half the city will shut for the first four days of the week and the other half will shut for the next four days. This includes curfews. It invokes deeper supply chain concerns and inflationary implications. I suppose that among the uncertainties could be concern about what the testing results may look like and any associated policy response, plus whether this will be a template for expanding measures elsewhere.

3. The PBOC again provided a net liquidity injection. This time it provided 150 B yuan in 7-day repo as 30B matured. This follows Friday’s move of 100B that netted 70B. Quarter-end liquidity provision is among the motivators. Lockdown fears are probably another catalyst for injecting liquidity.

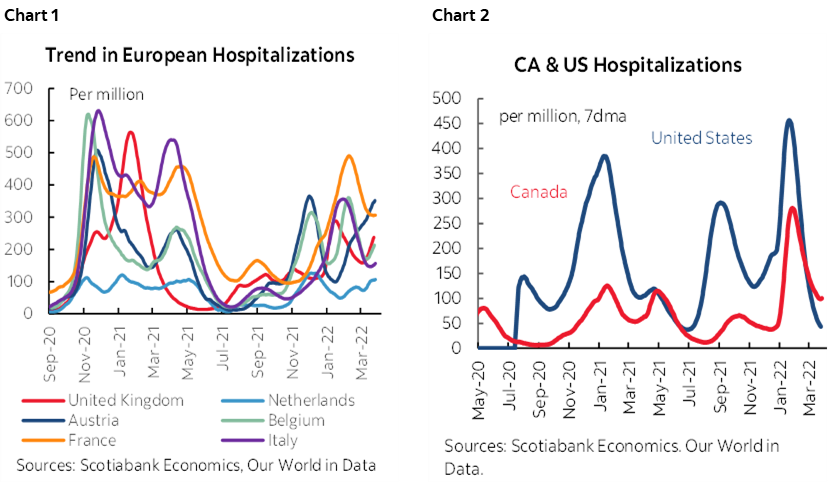

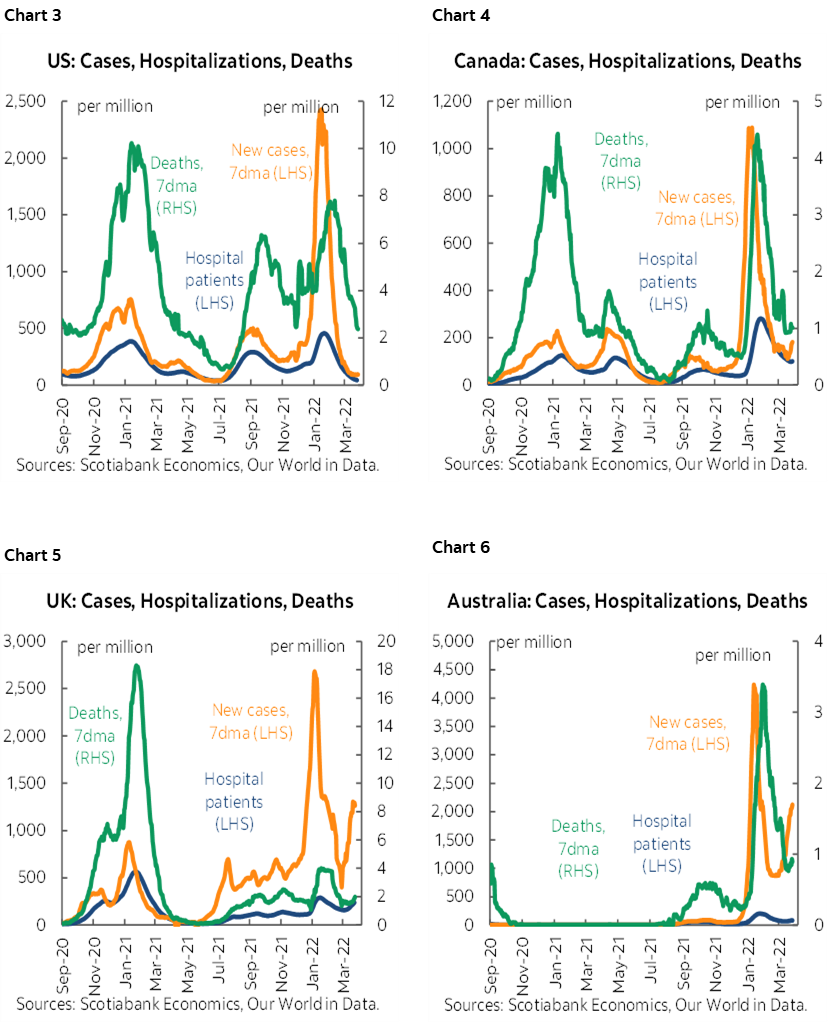

4. The more contagious BA.2 variant of the COVID-19 virus continues to rise and with it debate over whether it will be a wavelet or a wave both abroad and closer to home. Europe’s hospitalization rates are shown in chart 1. US and Canadian rates are generally stable as shown in chart 2. Ontario is seeing rising wastewater testing results and a very slight rise in hospitalizations among the unvaccinated over the past week (here). Quebec held an unusual press conference yesterday to warn of early signs that the BA.2 variant is on the rise. From what I saw, folks were very quick to ditch masks as restrictions lifted starting one week ago in Ontario. The test will come over the next 2–4 weeks post March-break and easing restrictions. A mild and transitory wave could prove to be constructive to sentiment. Across Canada, there has been a total collapse in vaccine doses being administered as only 47% of the population has received a third dose.

5. BoE Governor Bailey spoke on the economy and emphasized a large negative shock to incomes, negative pressure on demand that should create bidirectional inflation risk and evidence of slowing growth while emphasizing that on net it remained appropriate to tighten monetary policy. His modestly dovish remarks sent the two-year yield down

Calendar-based risk will be very light today. UK Chancellor of the Exchequer Sunak testifies to parliament following his Spring statement last week (9:40amET). The US just offered an early glimpse at the merchandise part of its trade deficit that held steady at US$107 billion in Feebruary. US retail and wholesale inventories continued to expand during February by 2.1% m/m and 1.1% m/m respectively in what I still view as a constructive restocking effect from depleted levels as supply chains struggle to replenish bare inventories. The Dallas Fed closes out the monthly round of regional manufacturing reports (10:30amET) that started off poorly with the Empire gauge but then saw a round of increases across the Philly, Richmond and KC Fed measures. The Dallas measure tends to follow oil prices over time so I wouldn’t be surprised to see some upside.

Canada will be quiet and follow the global market tone today and for most of the week. We might get a date for the upcoming Federal Budget at some point this week. The main takeaway from last week is that the coming Federal budget is set to be a spending spree that tosses aside legitimate concerns about awful productivity and a soaring cost of living. The budget will be based upon private sector forecasts that pre-date the war in Ukraine and recent bond market developments. Canadian yields are above the US at the front-end and in 10s as the relative borrowing advantage continues to slip away.

There is no Global Week Ahead for this week as I was on vacay, but the one I sent out on March 18th for last week’s developments (here) had also included a short look-ahead to this week’s main features.

- Friday’s US payrolls (consensus 490k, trimmed range from about 350k to 550k) and Eurozone inflation will be the main highlights.

- The US also updates PCE inflation readings that should largely follow CPI higher, along with an expected gain in incomes and soft consumption figures on Thursday.

- Canada refreshes Q1 GDP tracking with January’s final estimate and February’s preliminary estimates on Thursday.

- A very light line-up of CBs will only include large expected hikes from Chile and BanRep plus no change from the ever-exciting Bank of Thailand.

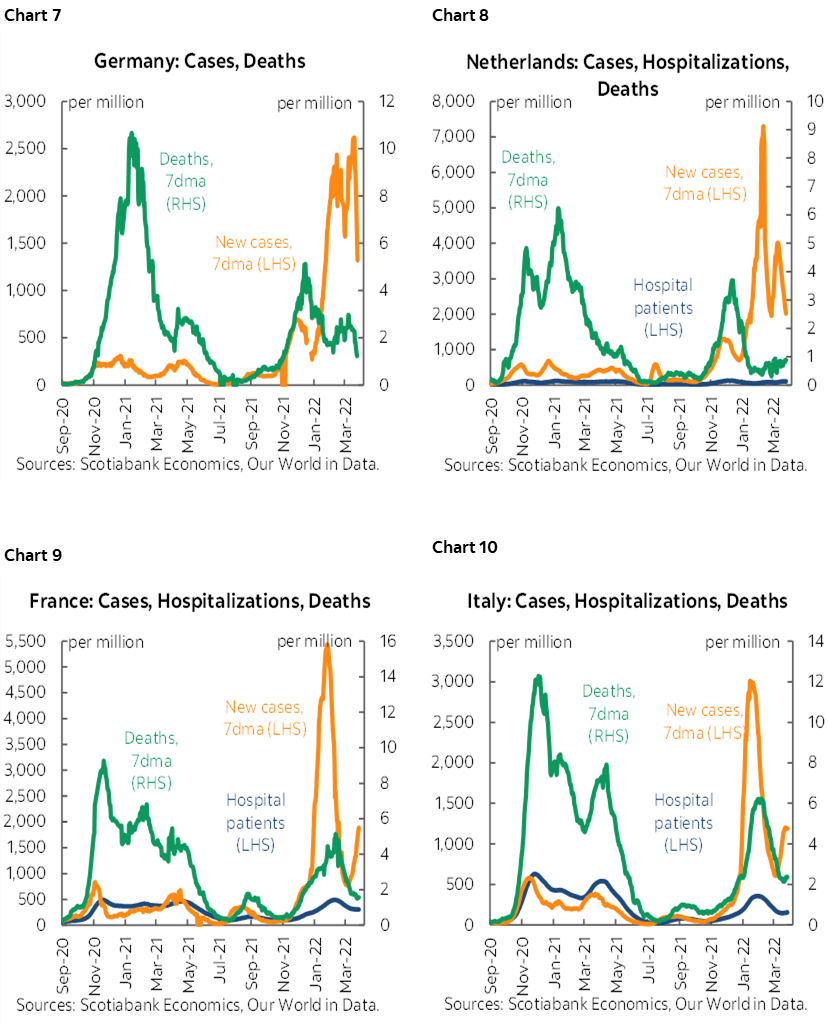

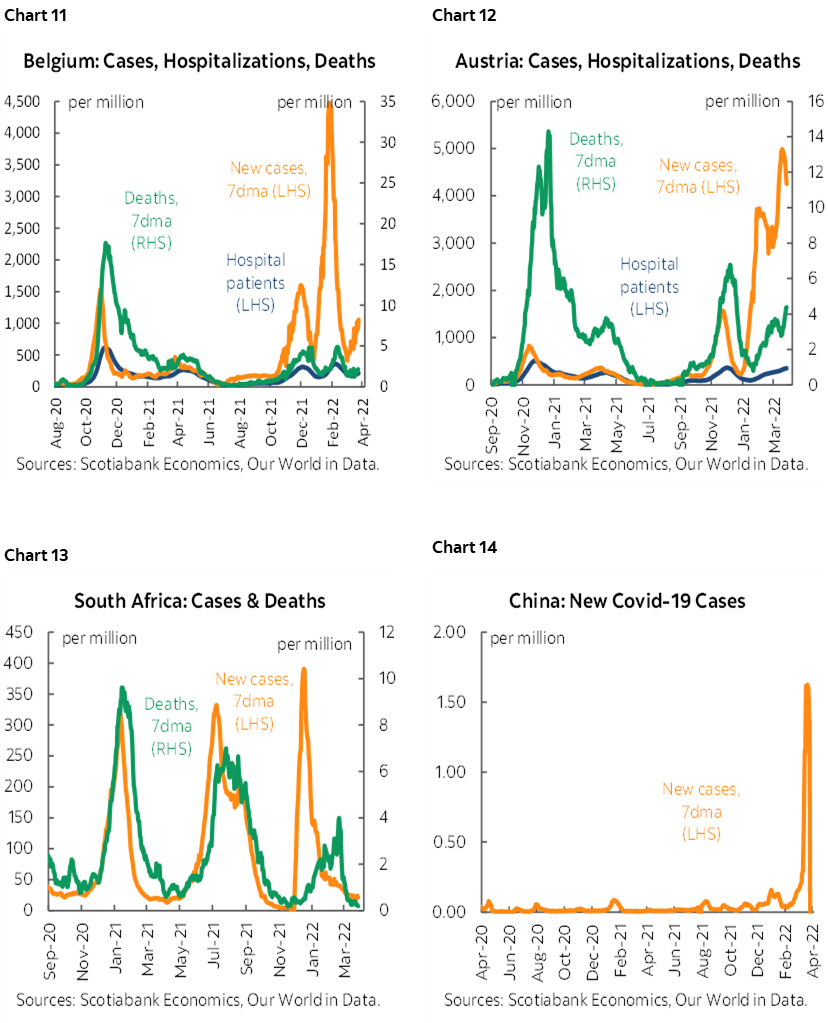

Please see the accompanying collection of global COVID-19 charts.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.