ON DECK FOR THURSDAY, JUNE 23

KEY POINTS:

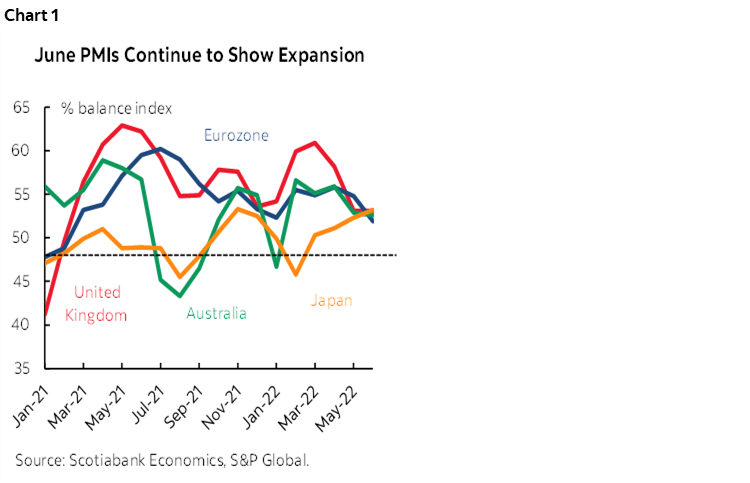

- European risk aversion follows PMIs

- Eurozone PMIs disappoint…

- …while UK, Japanese and Australian PMIs held firm

- US to update the PMIs the Fed doesn’t watch…

- ...after jobless claims were unchanged

- Fed’s Powell returns for round two of ‘wasn’t me’

- Banxico poised to hike 75bps

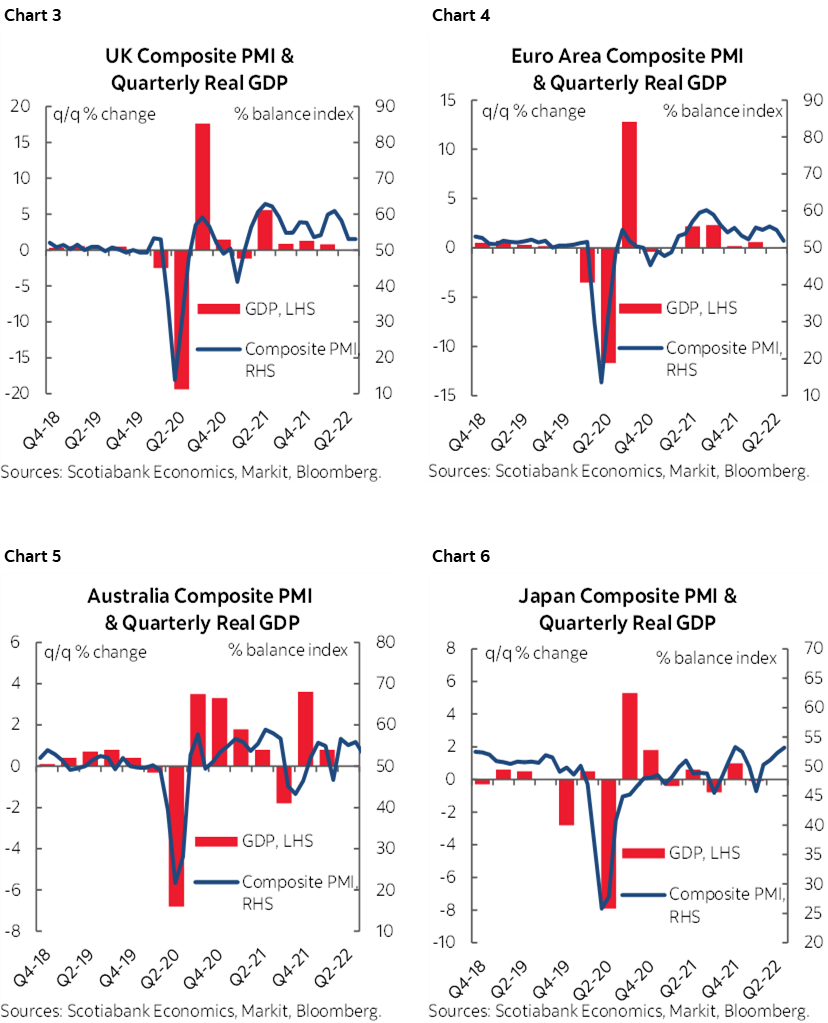

- Norges Bank hikes 50 and raises forward rate path, krone didn’t care

- Bank Indonesia stands pat, Philippines hikes

- Canada registers mixed preliminary gauges for May

Mon Dieu! Safe havens are all the rage this morning, thanks to France (see below).

With yields coming off their peaks one would think there would be pause for reflection upon recession risk as automatic stabilizers strengthen. The US ten-year yield—a key driver of the 30-year mortgage rate after swapped out—is about 36bps off the recent peak and rallying about 4bps this morning. EGBs and gilts are outperforming with bigger moves into the double-digit declines in yields across maturities as they’re closer to the epicentre of what’s obsessing markets at least for today. Stocks are similarly divided with more positivity on this side of the pond than across all the naysayers in Europe; European cash markets are more positive now than they were when the data first began to hit and range from flat in London to down ½% in Frankfurt with mild gains elsewhere, while N.A. equity futures are up by between ½% and ¾%. The yen and USD—in that order—are the preferred crosses but CAD is outperforming most other crosses partly buoyed by yesterday’s inflation blow-out and BoC expectations but also joined by MXN ahead of Banxico’s decision.

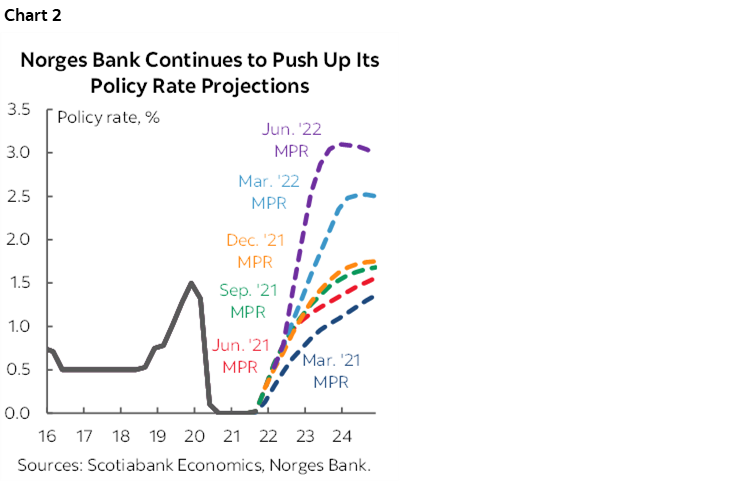

When France’s PMIs hit the ‘wires’ at 3:15amET they immediately triggered risk aversion as they tipped off greater downside than expected to the broader Eurozone PMIs that arrived about 45 minutes later. That effect waned as time passed. The Eurozone PMIs signalled slowing but still positive growth in the composite, services and manufacturing gauges. The fact that the UK’s and Japan’s PMIs surprised higher while Australia’s roughly held unchanged didn’t matter. See chart 1 for the composite gauges. It was the eurozone all the way. The charts on the next page show the PMI connections to GDP in each case. They are loose guides. Loose, as in underlined, italicized, and if you’re really feeling frisky then perhaps even bolded. See for yourselves! There is nothing about these gauges that will tell you about recession risk over the next, say, year or two. They tell you more about what’s going on in the current quarter and arrive earlier than other made up data.

Four central bank decisions were delivered overnight into this morning ahead of Banxico which is the only one that really matters to most of our clients.

- Norges: Hiked 50bps with the deposit rate set at 1.25% now. One-third of consensus got the call right, the other two-thirds expected 25 and will try harder next time. Forward guidance pointed to a 25bps hike at the next meeting in August while raising the cumulative rate path to 2% by the end of this year (previously 1.3% in the March forecasts) and 3.1% by the end of 2023 (previously 2.35%). Chart 2 shows the extent to which the central bank has kept revising its rate projections higher over time and it reminds me of the first time I practiced fly casting, minus the trees (don’t ask…). Maybe I’ve spent an unhealthy amount of time looking at charts in my lifetime. Anyway, the krone said phooey on all of that partly relative to what was priced and partly because of the weak Eurozone PMIs.

- Bangko Sentral ng Pilipinas hiked 25bps as expected.

- Bank Indonesia held its 7-day reverse repo rate unchanged at 3.5% as most expected.

- Erdogan’s central bank held at 14% as expected this morning. No one got fired this time though so the streak is still alive.

On tap into the N.A. session will only be a few developments.

Banxico is unanimously expected to hike 75bps this afternoon (2pmET). Officials have fairly strongly guided as much including DepGov Heath who said “For us, raising 75 is a lot, I don’t think raising 100 is possible, it would be better 75, two or three consecutive times.” With that, we may also hear forward guidance that leaves open such a path. Bi-weekly CPI surprised higher this morning with headline inflation rising to 7.9% y/y (7.7% consensus and prior) primarily driven by stronger core CPI at 7.5% y/y (7.3% consensus and prior).

Round 2 of Powell’s testimony kicks off at 10amET with the same statement, same grilling and similarly dour faces all looking to say inflation is the other guy’s/gal’s fault. Nothing changes from when you were kids, it’s still the same hot potato schoolyard antics. Every central bank statement these days can be neatly summarized in much shorter fashion with just the following words: Not me, I dunno, she did it, don’t ask me, and I’m telling you booboohead! Ah just go to your rooms for time-outs. No screen time today. And double veggies! But seriously, the cost to central banks’ ineptitude on the inflation front is rising recession risk and if you think a loss of faith in central banks has peaked then perhaps just wait.

The US also updates the S&P PMI measures (9:45amET) that are less watched than the ISM gauges the Fed prefers because the latter focus upon domestic economy considerations. Modest downside risk is expected to most of them. Weekly initial jobless claims were unchanged at 229k for anyone still reading.

A pair of preliminary estimates based upon incomplete samples indicate mixed results for Canada. Manufacturing sales fell 2.5% m/m in nominal terms during May mainly due to autos and primary metals but sales in the wholesale trade sector advanced 2% mainly due to food & beverage plus machinery and equipment with the latter boding well for business investment given that Canada imports most of its capital goods. These preliminary estimates are not adjusted for inflation.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.