ON DECK FOR FRIDAY, JUNE 17

KEY POINTS:

- Global markets licking their wounds after the week’s central bank moves

- EGBs react to Lagarde’s guidance on spread limits…

- …as central banks can’t resist continued meddling with price discovery

- The BoJ did….absolutely nothing!

- BoE’s Pill flags wages, pricing behaviour as conditions to act ‘forcefully’

- Powell on tap ahead of industrial output

Global markets are spending Friday licking their wounds after all of the central bank developments this week that had them fully awakening from their prior sleepwalking through soaring inflation. Consolidating positions ahead of the US ‘Juneteenth’ long weekend that will see stocks and bonds shut on Monday is probably an added factor amid light calendar-based risk and few notable developments.

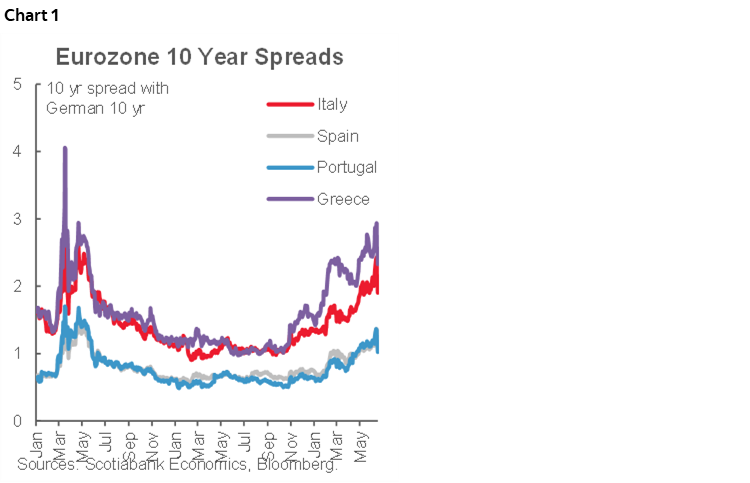

EGBs are rallying particularly through tightening Italian and broader peripheral spreads over bunds in what I think is reaction to Lagarde’s comments that hit after yesterday’s European close on how a new anti-crisis tool would target limits to how high bond yield spreads could go across the periphery. The ECB seeks to limit ‘irrational’ moves in spreads, whatever that would be. Chart 1 shows those spreads are back to around levels witnessed when the pandemic first struck. We’re left to interpret remarks from individual ECB members on this ‘irrational’ limit to spreads with Italy having a natural funding incentive to argue it should be lower. Get your bumper sticker now, ‘Free money for Italy!’ If markets are merely engaged in price discovery and rationing credit in differential fashion as monetary policy tightens then is that ‘irrational’? Seems to me we’ll never escape the period in which central banks think they should be imposing their judgement on markets and interfering with their fundamental functioning by picking winners and losers. Some of their actions have caused more problems than solutions.

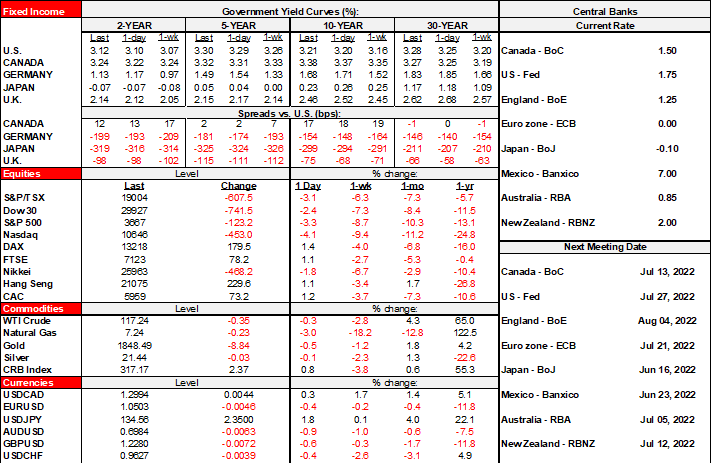

The US front-end is a touch cheaper with the 2-year yield up 3bps and less movement across longer term yields. The USD is slightly firmer and mostly against the yen’s reversal (see below). Stocks are broadly higher with US and Canadian futures up about 1% and with similar moves across European cash markets. The Nikkei followed yesterday’s declines across western markets and largely looked through the BoJ communications.

The Bank of Japan did…wait for it….absolutely nothing! As pretty much universally expected. Loose speculation going into last night’s Bank of Japan decisions had put a bid to the yen that subsequently fully reversed after the communications hit, leaving the yen little changed on net over the past couple of days. The yen is moving in on 135 to the USD. Governor Kuroda rejected a need to conduct another policy review and said that the sustainability of its 25bps yield curve control stance toward 10 year JGBs is not at risk while adding it would not be appropriate to tighten monetary policy that could cause an economic contraction. The statement noted that in the context of many uncertainties facing the Japanese economy, “it is necessary to pay due attention to developments in financial and foreign exchange markets and their impact on Japan’s economic activity and prices.” Some only picked out the foreign exchange part of that sentence. The BoJ to date has looked through yen weakness due to transitory effects on inflation that are incompatible with its medium-term inflation goals.

BoE Chief Economist Pill gave an interview saying that it’s up to markets to interpret what is meant by the insertion of “will if necessary act forcefully in response” to any indications of more persistent inflationary pressures. He added that ‘the trigger for this more aggressive action’ would be wage inflation and evidence that signs that inflation is becoming embedded in pricing behaviour of firms.

Fed Chair Powell will give welcoming remarks (8:45amET) at a conference in Washington on ‘the international roles of the U.S. dollar.’ There is probably low risk around this in the wake of Wednesday’s communications and given the Fed-Treasury arrangement on the dollar. We might also see a published commentary from KC President George on why she dissented on Wednesday.

The US will update industrial output for May this morning and it is expected to post a soft gain (9:15amET). And on this, I can only say: please don’t!! Yesterday’s speech on inflation by Canada’s finance minister might have been a tad pointless and a purely political effort, but another round of US stimulus cheques would only fan more inflation. Then again, economic logic hasn’t carried the day with the Biden administration as we can see on the Keystone snub to Canada while instead preferring to court MBS and Maduro. Further, if not for Manchin, Biden would have been rolling out more fiscal stimulus this year.

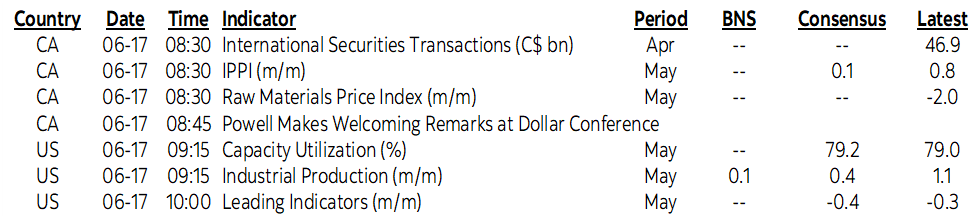

Canada’s calendar is dead quiet today. The focus going forward will be upon next Wednesday’s CPI release. I submitted estimates to newswires last Tuesday (1.2% m/m NSA and 7.8% y/y from 6.8% prior) but as yet there are no consensus estimates available.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.