ON DECK FOR TUESDAY, JUNE 14

KEY POINTS:

- Markets consolidating Fed-motivated sell-off

- Fed to hike 75bps tomorrow…

- ...as the WSJ sets up a Fed whisperer trade...

- …though it’s not a slam dunk…

- …and would pose a bigger communications credibility challenge

- UK data beats

- Swedish inflation tops estimates

- German ZEW gently rising off bottom

- US producer prices land a smidge weaker than expected

- Canadian manufacturing shipments beat expectations on revisions

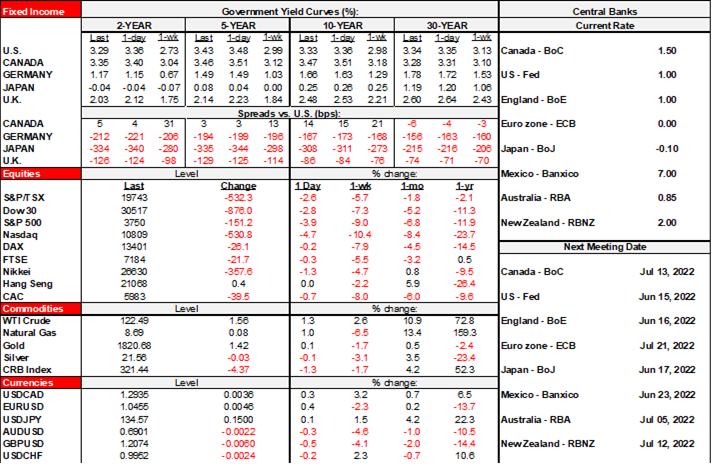

Markets are consolidating yesterday’s repricing of tomorrow’s FOMC communications. Sovereign bonds are slightly rallying in the US, Canada and UK after yesterday’s rout, but so far it’s a minor move lower compared to the scale of yesterday’s selloff. The USD is more mixed this morning and losing ground to the euro and related crosses, but generally holding onto most of yesterday’s rally. US equity futures are up by around ½% following yesterday’s 3.9% plunge by the S&P. TSX futures are up ½% after yesterday’s drop of over 2½%.

I hate the feeling around doing this but now think the Fed will hike 75bps tomorrow instead of 50bps. I’ve long preferred seeing a faster pace of front-loaded hikes and although it’s not a slam dunk, the case for accelerating the size of hikes outweighs the case against while nevertheless making inter-meeting Fed forward guidance largely useless. The supporting points include:

a) Last Friday’s CPI report showed no indications that inflationary pressures are abating at the margin as evidenced by high m/m readings and very high breadth. Being in blackout, the Fed couldn’t officially respond to another upside surprise to consensus. As previously argued, this raised the risk of 75.

b) Unless they are being super mischievous, then we may be back to the times when the Fed communicated through preferred financial media outlets. Note the WSJ piece that started it all yesterday afternoon before other outlets basically ran with the same points which either suggests copycat behaviour or that the Fed pushed out the same messages to each outlet. If the Fed doesn’t hike 75 then the WSJ and its reporter are toast as Fed whisperers. If the Fed does hike 75 then what ever happened to the requirements set by our regulators to engage in full and open disclosure?? Do as I say not as I do, I guess.

c) It would no longer surprise markets given that it’s fully priced and so the fear of sparking market turmoil has already come and gone. By corollary, not going 75bps would risk awkward optics around easing financial conditions with inflation ripping and after a jobs beat unless they really hit forward guidance much harder than is already priced which is tough to see given we have 3½ – 3¾% priced for year-end now. In other words, if they pass on 75 and don’t go to 3¾% by year-end then headlines on dovish market reactions relative to what’s priced would be super awkward optics for them;

Other arguments don’t hold water in my view. The argument that the Fed realizes it is behind and must pick up the pace is a bit of a joke as they’ve been behind for basically a year now and so why the sudden epiphany. The argument that the language used by Powell and in the last statement left open the possibility of a 75bps move tomorrow is equally farcical. The explicit guidance was 50 right up to the blackout and markets took the “nimble” and data dependent guidance as being more about the future path after tomorrow while hoping they could at least count on explicit one-meeting ahead guidance.

Hiking 75 is not going to be a costless move by the Fed. If they do indeed hike by 75bps tomorrow, then even their one-meeting ahead forward guidance will become utterly useless. Every meeting will become open season on the Fed and power to drive market volatility will be handed over to media outlets. Every blackout period will be open to speculation to the benefit of the WSJ et al which seems to me to seriously violate full transparent disclosure. We’ll be going back to the days when WSJ reporters were made stars solely because of their preferential access and that’s just plain wrong if that is indeed what is happening here.

Swedish inflation exceeded expectations. Headline CPI was up 1.0% m/m (consensus 0.8%) and underlying inflation was exactly the same. The figures reinforced pricing for a more aggressive Riksbank hike of 50bps at the June 30th meeting.

The UK generated 75k jobs in April which pumped the 3-month moving change up to 177k, handily beating consensus expectations for a 106k rise. Wage growth ex-bonuses also exceeded expectations at 4.2% y/y (4% consensus) but was unchanged from the prior month, although including bonuses saw wages up 6.8% y/y which was softer than consensus that had 7.4%. The May payroll figures were up 90k (consensus 70k) but with a mild downward revision to 107k from 121k for the prior month. In all, it seems pretty strong to me, though markets took at as evidence the BoE would continue to lean toward a 25bps hike on Thursday instead of a larger one.

German ZEW investor expectations improved by a little less than what is a total guesstimate by consensus. That’s two months in a row of gentle improvements off the April bottom.

Canadian manufacturing shipments exceeded expectations due to upward revisions. While April landed on the screws at +1.7% m/m, the prior month was revised up from 2.5% m/m to a full percentage point higher. Sales were up by 0.9% m/m in volume terms during April such that the gain was not just fed by higher prices.

US producer prices landed a smidge weaker than expected but were still strong. Headline final demand prices were up 0.8% m/m and on consensus, but the prior month was revised a tick lower to 0.4% m/m. Core producer prices ex-food and energy were up 0.5% m/m and the prior month was revised down to 0.2% from 0.4%. All-in, that says final demand prices were up 10.8% y/y which was a tick softer than both consensus and the prior month.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.