ON DECK FOR TUESDAY, JANUARY 18

KEY POINTS:

- US-China yield curves diverge on relative central banks

- PBOC signals further easing ahead

- Markets place ~70% odds on a BoC rate hike next week

- BoJ’s dovish Kuroda dismisses market rumours

- UK job markets a little less resilient after furlough program

- Eurozone investors looking through omicron

- Trivial N.A. data on tap

Global markets are in risk-off mode this morning. Equities are lower by either side of 1% across N.A. futures and European cash markets with weaker than expected US bank earnings not helping. The US returns from a day off and is catching up to developments. US-China yield divergence is the dominant theme across fixed income markets as the US front-end cheapens with 2 year yields up another 5bps in a bear flattener while PBOC comments drove an overnight rally in Chinese rates. European yields are little changed. The USD is a touch stronger except against CAD given BoC bets that moved higher after yesterday’s surveys (recap here). Canada’s curve is slightly adding to front-end rate pressures but the bigger move was yesterday; OIS places the odds of a 25bps BoC hike next week at ~70%.

PBOC guidance that further easing measures are likely sent China’s yields lower by 7bps in 2s and 4–6bps further out along the curve. My things have changed in China compared to strident earlier remarks that lambasted policy easing abroad while digging in at home. Deputy Governor Liu Guoqiang said the PBOC will “open monetary policy toolbox wider, maintain stable overall money supply and avoid a collapse in credit.” He left the door open to further modest reductions in the required reserve ratio. Next up may be a reduction in the 5-year Loan Prime Rate tomorrow night (eastern time). The whole PBOC narrative has shifted over December into the new year as mounting downside risks to China’s economy have paired with no inflationary pressure and rising risks to financial stability related to soft growth and problems in the property finance market.

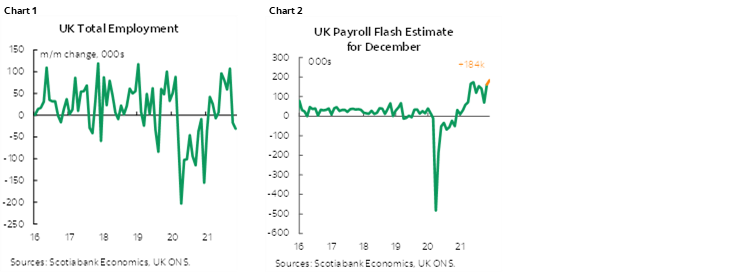

UK job markets lost some of their resilience in the wake of the end of the furlough program in September as payroll employment appears to have posted steady gains but total employment has recently softened. 184,000 payroll jobs were added in December, although the prior month’s gain was revised lower to 162k from 257k previously. Total employment lags by a month and it fell by 31k in November after falling by 17k the prior month and gaining 107 in September for a three-month net total gain of only ~60k. See charts 1 and 2. Wage gains ebbed a touch in touch with expectations are 3.8% y/y ex-bonuses (4.3% prior).

Bank of Japan Governor Kuroda lashed out at the “sources” behind a news article last week that intimated the central bank is working toward priming markets for eventually tighter policy in light of alleged inflationary pressures. Kuroda flatly said “Raising rates is unthinkable.” So there! He added “We’re expecting long- and short-term policy rates to remain at the current low levels, or fall even lower.” There were no policy changes at this meeting, as universally expected. Forecast changes were in line with expectations. Inflation forecasts were revised very slightly higher but at 1.1% y/y in 2022 and 2023 inflation is forecast to remain well below the 2% target. Risks to the inflation outlook are now judged to be more balanced, but that’s a far cry from being hawkish given the requirement of sustained 2% inflation before tightening. Growth forecasts were revised slightly lower.

In a sign that investors are looking through omicron, German and Eurozone investor expectations increased sharply in January’s ZEW survey. The Eurozone tally nearly double to 49.4 which is the highest reading since last July. Germany’s ZEW expectations measure also hit its highest since July.

The main focus into the N.A. session is Goldman’s rare miss on earnings. Trivial N.A. data is on tap. Canadian housing starts will likely pull back after a surge in multiples temporarily popped the prior month’s tally to its highest since March. The US Empire manufacturing gauge kicks off another month of tracking conditions on the path to the next ISM-manufacturing report. Watch for omicron-fed supply chain and price pressures.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.