ON DECK FOR MONDAY, JANUARY 17

KEY POINTS:

- Mild risk-on bias fed by Chinese policy easing

- PBOC eases and there is probably more to come

- BoC’s twin surveys on tap; watch expectations

- US markets shut for MLK Jr Day

- Updated global COVID-19 hospitalization and mortality charts

- Please see the Global Week Ahead here.

Mild risk-on sentiment is being driven in part by Chinese policy easing while US markets are shut for Martin Luther King Jr day.

China’s rates curve slightly bull steepened to start the week after the PBOC cut a pair of rates and with more easing likely to come. Most of China’s neighbouring currencies generally depreciated as the spillover effects upon other regional central banks are being considered; some of them are stuck between a rock and a hard place given the mixed capital account implications to Chinese policy easing while the Fed moves to tighten. European curves entered the week in risk-on fashion by cheapening to the tune of ~2bps across the gilts curve and with EGBs bear steepening and driven by ~2bps increases in 10s. Canada’s curve is performing similarly. The USD is mixed against major currencies with some like the krone, CAD and A$ slightly firmer against the USD while sterling, the yen, won and rand weaken. Equities are slightly firmer by up to ¾% across European exchanges, although it was mainland China’s exchanges that led the way with a gain of ½% in Shanghai’s more SOE-driven market and 1½% in Shenzhen.

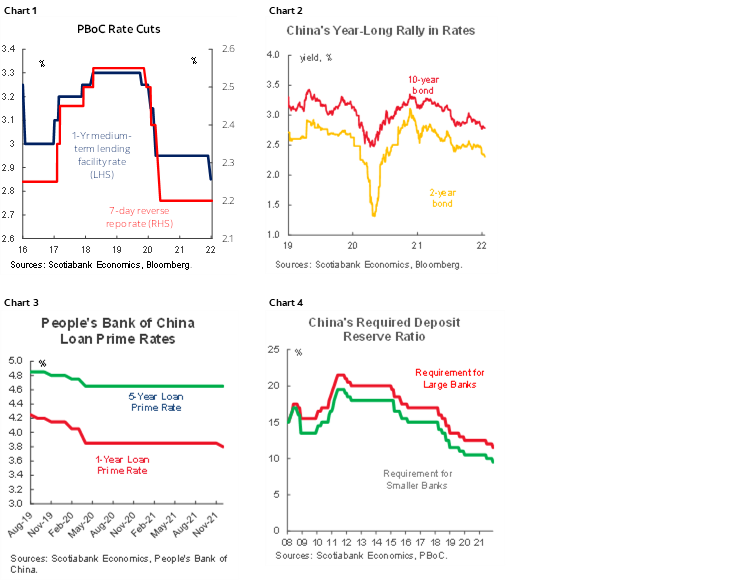

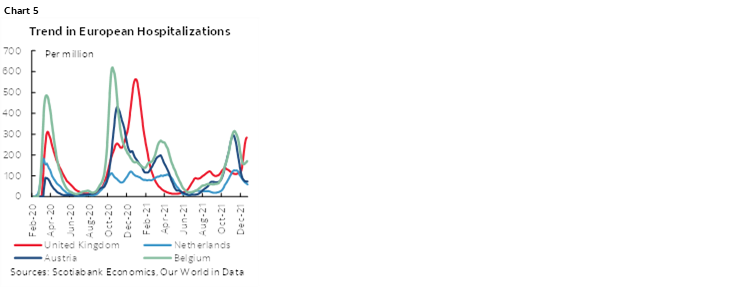

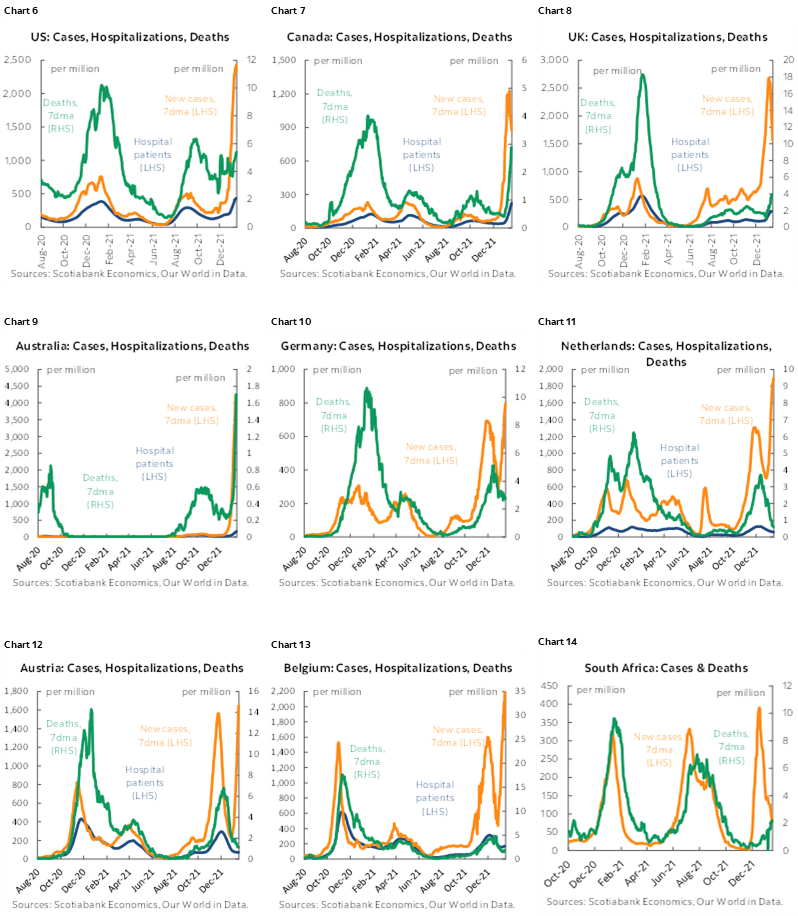

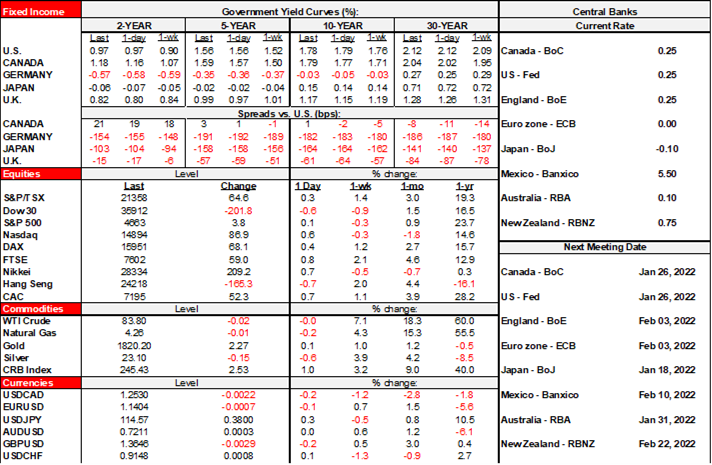

The PBOC teased with a 10bps cut to the 1-yr Medium-term Lending Facility Rate (now 2.85%) and a 10bps reduction to the seven-day reverse repurchase rate (now 2.1%) as shown in chart 1. The moves have been long in the making as China’s rates curve has been rallying throughout the past year (chart 2) and reflect lagging policy adjustments that have been guided to expect for some time now. These moves leave the door open to reductions in at least the 5-year Loan Prime Rate and perhaps also the 1-year LPR on Wednesday evening eastern time (chart 3), to further subsequent rate reductions as a monetary policy easing cycle continues and to additional cuts in required reserve ratios after the reduction in mid-December (chart 4). The 10bps cut to the MLF exceeds the 5bps cut to the 1-year LPR that banks drove in December and so we could see them add another cut this week and carry-through with a first reduction in the 5-year LPR. If the PBOC is intent upon addressing mounting downside risks to China’s economy in the context of no inflationary pressures, then -10bps won’t do anything material to address the fact that it still has among the world’s highest real policy rates. Chinese monetary policy remains overly tight and the bigger risk to stability stems from an overly tight policy stance. After having dragged its feet through much of 2021 while criticizing easy policy elsewhere, the shoe is arguably on the other foot now.

China’s macro updates were soft with mixed outcomes relative to consensus expectations. They were also stale as zero COVID and the rising impact of omicron on China’s key export destinations is more of a 2022Q1 story. So for what it’s worth, Q4 GDP was a bit firmer than expected at 1.6% q/q SA (1.2% consensus) and 4% y/y (3.3% consensus). The quarter ended with mixed readings as retail sales grew at less than half the expected paced (1.7% y/y, 3.8% consensus) and industrial output was up a little more than expected (4.3% y/y, 3.7% consensus).

On tap today will be the Bank of Canada’s quarterly business and consumer surveys (10amET) after a stale report on manufacturing shipments in November that I expect to post a rise of ~3% m/m based on advance guidance (8:30amET). The survey periods pre-date omicron’s impact since the cut-off was in early December and the BoC always takes forever to turn these small sample surveys around 1.5 months later. Still, it will be the expectations measures for inflation, wages and house prices that may matter given a) they were already moving higher and if they rose even more before omicron, then they might do so even more in the face of the supply shock implications, and b) the BoC has emphasized it is closely watching measures of expectations.

Also see the updated charts 5–14 that show trends in COVID-19 hospitalization and death rates.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.