ON DECK FOR FRIDAY, JANUARY 14

KEY POINTS:

- Risk sentiment sours on mixed US earnings

- Friday’s joke of the day is about the BoJ

- BoK hikes, guides more to come

- US retail sales, IP, consumer sentiment on tap

- US retail spending is soft partly due to bare shelves, services rotation

- Overnight macro round-up

US bank earnings and modest US data risk will follow an overnight session that saw Korea’s rates curve getting hammered by the BoK, a rather odd piece about the BoJ, and stale macro reports out of China and especially the UK that was very strong.

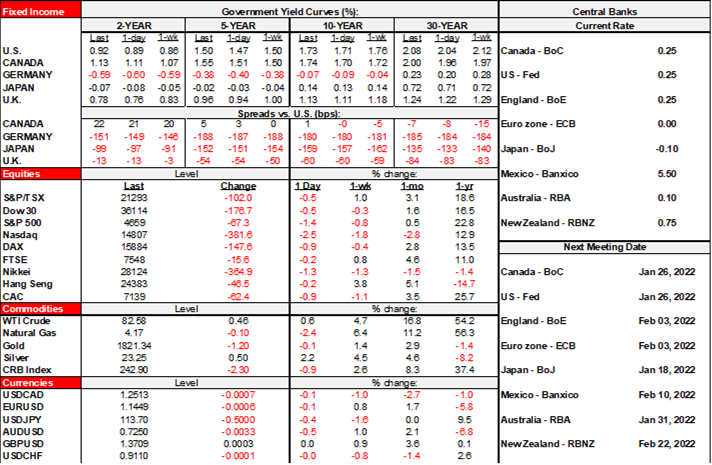

Sovereign yields are pushing higher across the board. US Ts are cheaper by about 4bps across maturities, yields on gilts are up by a similar 3bps or so, while EGB curves are slightly bear steepening with 10s up ~3bps. N.A. equity futures are in the red by about -½% after JPM released earnings, while European cash markets are off by up to about 1% after Asian exchanges followed yesterday’s US sell-off. The USD is little changed with outperformers led by higher beta commodity crosses like CAD, NOK and the rand. Oil was up by over 1% but post-earnings has shaved by about half. The yen is also firmer on the back of a story about BoJ tightening.

Here’s a recap of overnight developments before turning to what’s on tap for today.

1. Across central bank land there were two main developments and keep an eye on a possible third one this morning.

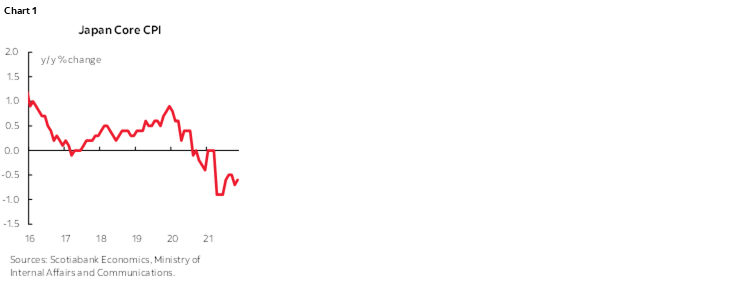

I. What is this, a joke? Absent a rumour, start one? “Sources” are saying the Bank of Japan is thinking of a rate hike at some point beyond this year and debating how to manage the messaging. The rationale? Inflation is picking up, or so we’re told. Right. Inflation was 0.6% y/y in November and next week’s expectation for December is 0.9%. Ex-food & energy, prices are lower at -0.6% y/y and falling (chart 1). The ‘sources’ say the BoJ never said they wouldn’t hike until hitting the 2% goal. Nah, they just massively eased for the heck of it… Onto next week’s BoJ meeting I guess.

II. The Bank of Korea hiked by 25bps to a 7-day repo rate of 1.25% as three-quarters of consensus had expected. Korea’s rates curve underperformed all others due to hawkish guidance. Governor Lee Ju-yeol guided that further hikes would be needed while stating that “inflationary pressures are expected to be much larger than earlier expected. There are uncertainties surrounding he pandemic, but they are unlikely to derail the domestic economy’s recovery.”

III. ECB President Lagarde speaks about the 20th anniversary of the Euro, its achievements and the future of the euro at 8:30amET.

2. A series of macro reports were generally stale readings before omicron injected at least near-term downside risk.

I. China’s export figures for December were stale on arrival in the face of omicron’s impact at home and abroad, but fwiw exports were in line with expectations while imports were softer. Exports advanced by about 21% y/y in USD terms (consensus ~21%) and imports were up by about 20% y/y (consensus ~28%). The trade surplus unexpectedly widened again to a new record high.

II. The UK economy was doing rather well before omicron as illustrated by stale November readings. Monthly GDP advance by 0.9% m/m (consensus 0.4%). Industrial output was up by 1% m/m, or five times consensus. Construction output was up by 3.5% m/m, or nearly six times consensus. The services sector advanced by 07% m/m (consensus 0.5%). Last, the country swung toward a trade surplus partly fed by positive revisions but also because November’s exports were up by 9.3% m/m and imports were up by 4.7% m/m. Then omicron and Boris’s issues with sound judgement hit….

III. Lastly, Swedish inflation generally landed a tick above expectations but much of the pressure was driven by soaring electricity prices. Headline and underlying CPI were both up by 1.3% m/m (consensus 1.2%) but underlying ex-energy was up by just 0.4% m/m. With underlying CPI ex-energy inflation at 1.7% y/y, I’m not getting some of the commentary about how the Riksbank needs to sound more hawkish anytime soon—especially given its checkered history.

Incremental risk into the N.A. session will be primarily driven by bank earnings with macro reports that may be treated as a stale assessment of the pre-omicron world.

I. The Q4 earnings season kicked off in earnest this morning with the usual early focus upon financials. BlackRock posted a small beat with EPS at US$10.42 (consensus $10.15). So did JP Morgan Chase, but its shares got hit by lower than expected FICC and equity trading revenues. Wells Fargo beat expectations with EPS of $1.38 (consensus $1.12) and the pre-market generally likes the details. Citigroup is up next at 8amET with consensus EPS at US$1.62.

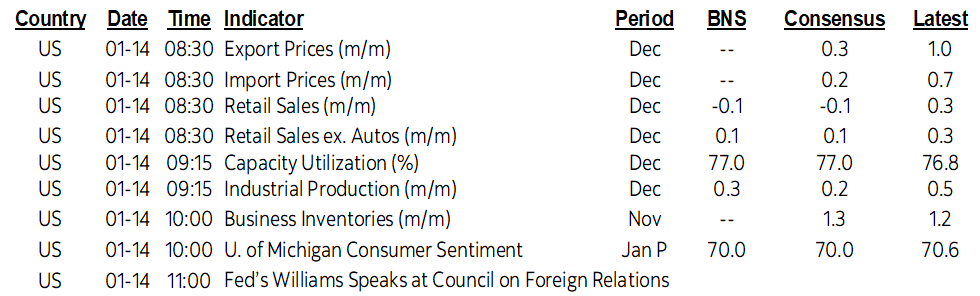

II. Retail sales for December (8:30amET) are expected to be little changed with downside risk given the decline in auto sales and gas prices. Key will be core sales (ex-autos & gas) as an indication of the holiday shopping season after November’s core sales were only up 0.2% m/m. Downside risk will persist as omicron takes effect into January’s numbers. December may have seen total consumption outperform retail sales as budgets rotated toward services spending before omicron hit and as seen in the CPI figures.

III. Also watch the UofM’s consumer sentiment gauge for January (10amET) as a litmus test of how the US consumer mindset is holding up (or not).

IV. Also keep an eye on US inventories-to-sales as a supply chain indicator (10amET); October’s reading was tied with March 2011 for the lowest on record since at least 1980 (chart 2). Very lean inventories are part of the inflation narrative near-term. P.S. Still waiting for our new stove...we could have had another child in less time!

V. US industrial output in December is expected to grow slowly (9:15amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.