ON DECK FOR THURSDAY, FEBRUARY 24

KEY POINTS:

- Russia invades Ukraine, risk-off sentiment ensues

- China further alienates itself with support for Russia, incursions into Taiwan’s airspace

- The Fed and BoC should stay on course with planned exits for now

- Fed officials may weigh in on the consequences, BoC in blackout

- Alberta’s budget revisions have started before the budget’s delivery!

- Light US releases & CDN bank earnings don’t matter

That markets were naively expressing hope earlier in the week that Putin might come to his senses is rather convincingly being exposed as sheer folly this morning. The brutal Russian dictator has indeed launched a full invasion of Ukraine with the stated goal being to “demilitarize” Ukraine. Hearts out to Ukrainians including the large community in Canada that is the world’s third largest population of Ukrainians. Watch for crippling sanctions today that are very likely to exclude Russia from the Swift global payments system, block all access to the USD, tighten Russian access to western technology, apply more sanctions against individuals, and it’s thankfully the final nail in the Nord Stream pipeline that Germany never should have pursued in the first place.

Apart from sanctions that will again cripple the Russian economy, there are countless related issues that arise including a very limited list as follows:

- As events unfold and markets further digest the consequences, we’ll see if the sustained effects on risk appetite are similar to the modest and fleeting effects of 2014, or something deeper. That’s hard to judge at this early stage. I certainly don’t know and find it impossible for anyone to know at this point, but I have to admit that my bias is to treat it as having limited consequences versus irresponsibly fanning mass hysteria by assuming this develops into a series of escalating moves.

- Apart from words and sanctions, it’s unlikely the West has much appetite for a direct confrontation unless by accident. Ukraine is not a NATO member and so there is no treaty-bound requirement to translate the huffing and puffing and sanctions into anything more than weapons offers and moral support.

- I don’t think one should assume Russian victory and I don’t know how that would be defined in any event. Even if devastation ensues as a first order outcome, has Putin put himself into a long conflict with no prospect of exiting? To “demilitarize” certainly sounds like an occupying force for the long haul. Could this be his grandest blunder? Might Ukrainians pay the ultimate price for what could eventually turn into Putin’s downfall? We’ll see what price Russians put upon their view that Ukraine is indeed theirs as the Russian economy implodes and the oligarchs’ wealth plummets but thoroughly cutting off Russian from the world is the west’s best policy hope here.

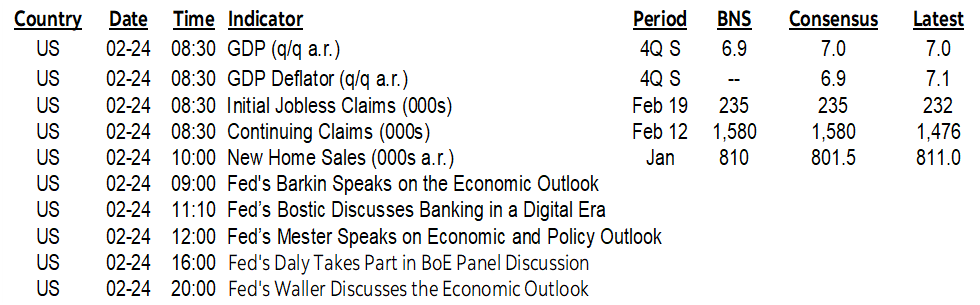

- Will central banks like the Fed and the BoC (next week) stay on course with planned tightening, or will they suspend plans? I would think that at least for now the plans are set for March. The Fed may look at the additional inflationary impulses from higher oil and the lower bond yields and view them as unsuited to domestic conditions much like they argued in 2014. Watch for comments from Fed officials today but with the BoC in blackout. Barkin speaks at 9amET, Bostic at 11:10amET, Mester at 12pmET, Daly at 4pmET and Governor Waller at 8pmET.

- As for next week’s BoC decisions, I would expect them to emphasize that the direct ties between the US and Canadian economies and that part of the world are de minimis in nature, while noting that Canada is getting perversely positive imported effects upon its economy through lower borrowing costs, mild depreciation in CAD and higher oil prices. If Canada were at a point still marked by material slack and low inflation then it might be a different matter, but such influences from oil, yields and CAD at a point of full employment with a shut output gap and inflation at a record distance above target are very likely to keep the BoC focused upon its guided path toward a hike and carving out a planned reduction in reinvestment as soon as Q2. The bias could be carefully managed as data dependent and dependent upon the further course of events.

- The serious prospect of a full humanitarian crisis has to be considered as some Ukrainians stay and fight, while some flee toward the border with Poland (a NATO member) amid risks that the conflict spills across borders.

- China is likely to further alienate itself across the West with comments like this morning’s sympathetic remarks from the country’s foreign minister who said he understands Russia’s “reasonable” security concerns later enhanced by some ministry hack’s remark that such concerns are “legitimate” and that “the US recently has been escalating tension and hyping up war.” Right, reasonable and legitimate, like what China does to the Uyghurs. China will be an indirect casualty of this development across the world’s political capitals. Taiwan’s announcement that 9 Chinese military aircraft were detected in its airspace this morning will only fan the risks.

- Russia’s ability to retaliate against sanctions with cyber attacks was less developed 8 years ago and with that we are potentially in uncharted waters insofar as the risk of a cyberwar is concerned. If the military conflict is regionalized, then it seems to be that the risk of cyberwars and how the rest of the world may respond could be more significant.

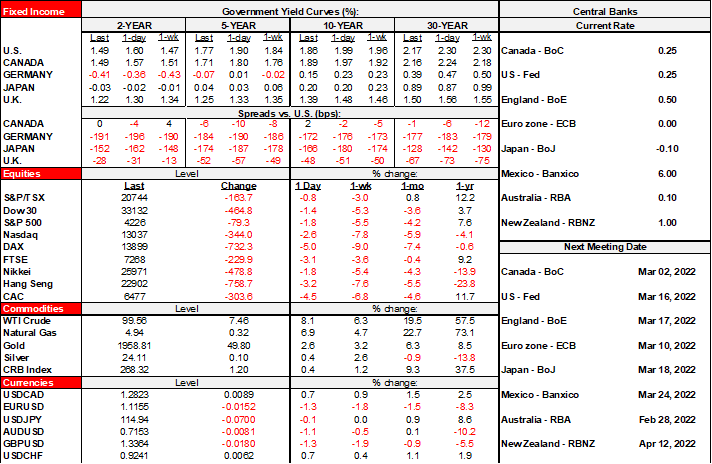

For now, you can see the market response with your own eyes. European stocks are down by 3–5% across the board. N.A. equity futures are down by 2 ½% -3% in the US, 1 ½% in Toronto no doubt as the energy weight is helping to insulate against bigger losses. Oil prices are soaring with WTI and Brent up about US$7–8/barrel. US Treasury yields are plummeting with the whole curve down about 9–12bps. Gilts are ~8bps richer, EGBs are rallying by between 3–8bps across different countries and parts of their curves. The USD is clearly the hands down winner along with the yen, while European crosses are falling leading decliners. The ruble is down another 4% to the USD and has depreciated by almost 15% in two weeks while Russian 2s are up by over 500bps over this period in anticipation of expedited monetary policy tightening. Russia’s central bank is going to have to expedite monetary tightening (see chart). Kiss goodbye Russia’s economy in potentially more serious fashion than how it went flat in 2014 and then mildly contracted in 2015. As for Russian inflation, at the time of the 2014 invasion it was running at about 6% y/y and soared to about 17% in early 2015; the starting point this time is already higher at almost 9% so we’ll see how Russians feel when inflation hits 20% or maybe higher. The ability to use higher oil prices to mitigate some of the effects depends upon there being a big enough market for Russian oil abroad which there might be in China and some EMs but not if UK PM Johnson’s pledge to end European reliance upon Russian energy winds up as something more than just empty words.

Clearly nothing by way of calendar-based risk is at all relevant today. Light data includes US GDP revisions that met expectations for a 7% annualized growth rate in Q4 which is up just a tick from the initial estimate. Weekly jobless claims fell marginally to 232k from 249k with continuing claims falling to 1.476 million from 1.588 million. US new home sales (10amET) could slip given advance readings on model home visits, and jobless claims. Canada’s lagging payrolls release usually does not garner much of a following. Fed and BoE speak is likely to be more of the same in terms of the general tone.

Canada’s bank earnings parade started this morning with RBC first out of the gates. They beat expectations with adjusted EPS of C$2.87 (consensus was C$2.72). Meh, good for them. Now back to Russia…

Alberta’s budget lands this afternoon (probably ~3:15pmET). Marc Desormeaux will be covering. The budget revisions are in play before the budget has even been released. Whatever oil price assumption they included in the pre-set projections that were established some time ago is going to be stale and hence so will be the projected fiscal balance.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.