ON DECK FOR TUESDAY, DECEMBER 13

KEY POINTS:

- Risk-on bias could go either way after US CPI

- There is a wide interval of expectations for US core inflation…

- ...but it would be statistically unusual for nowcasts to materially overestimate again

- UK job markets mostly outperform expectations…

- …with a few dovish signals…

- …that keep most of the focus on tomorrow’s UK CPI ahead of the BoE

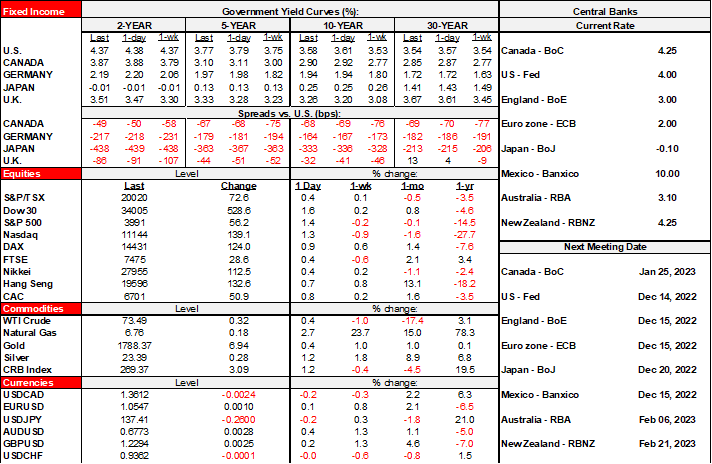

A mild risk-on bias will clearly be sensitive to whatever happens when US CPI lands and so take it with a grain of salt. US and Canadian equity futures are up by roughly ¼% to ½%. European cash markets are generally ¼% to 1% higher. Asian equities gained in Tokyo and HK, were flat in Seoul and Shanghai and fell in Shenzhen. Sovereign yield curves are slightly bull flattening in the US with gilts underperforming everyone else partly due to strong employment figures and uncertainty ahead of UK CPI tomorrow and then the BoE. The dollar is little changed on a DXY basis as it loses ground to Sterling and a handful of higher beta crosses. Oil prices are about 1% higher.

News that an economic policy meeting in China has been postponed due to surging cases in Beijing arrived after local markets had shut but is generally being taken in stride elsewhere. Ontario is starting to register a mild increase in wastewater testing results as indicated here. California’s wastewater testing results have surged back to June/July levels (here).

UK job market figures mostly surprised higher than expected on the eve of CPI figures ahead of the BoE’s decision on Thursday. There were a few mixed signals and it would likely take strong inflation readings to matter more toward a chance at another 75bps hike as markets are still pricing a little over a 50bps increase.

Wage growth accelerated to 6.1% y/y with a slight upward revision to 5.8% the prior month. That exceeded all estimates and is the first time in data since 2001 that earnings growth exceeded 6.1% with the exception of the distorted reading in June 2021. The number of employees on payrolls surged ahead by 107k in November for the strongest gain since August 2021. Total employment that lags a bit further behind was up by 27k (consensus -17k) on a 3mo ago basis as it gained 34k m/m.

The few dovish signals included the fact that the unemployment rate moved up a tick to 3.7%, jobless claims increased to 30,500 in November for the largest amount since February 2021 and job vacancies fell but only by 30k. Vacancies have edged lower since May but still remain very high.

US CPI lands at 8:30amET just before the FOMC’s two-day meeting commences today. FOMC members submitted forecasts last Friday but can alter views up to tomorrow evening. There is a high bar for any CPI surprise to affect anything in tomorrow’s communications until the press conference given a) 50bps is largely committed, and b) changing any dots/forecasts on one point would be unlikely. Any significant surprise is more likely to affect the tone of the press conference.

The breakdown of consensus views on core CPI includes 11 of us expecting 0.4% m/m SA, 32 expecting 0.3% and 22 expecting 0.2%. The Cleveland Fed’s CPI nowcast is above all of us at 0.5% m/m. See the global week ahead for more.

On the latter note, the Cleveland Fed’s nowcast overestimated inflation last month but it’s worth noting that this was a relative anomaly. The extent to which it overestimated headline CPI was a record outlier in the pandemic (chart 2). It also overestimated core CPI by the largest amount since the start of the pandemic (chart 3).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.