ON DECK FOR MONDAY, DECEMBER 12

KEY POINTS:

- Mixed risk appetite ahead of a packed week

- China covid risk shifts to anecdotes

- BoC’s Macklem is likely to repeat forward guidance

- Yellen downplays inflation concerns. Again.

- UK releases faded

- Global Week Ahead reminder

As a reminder please see the Global Week Ahead—The Alternatives Would be Worse. The publication link is here and the slide deck is here.

Key topics:

- Monepalooza week!

- The 3 worse alternatives to fighting inflation

- FOMC tail risks to a pre-set script

- US CPI expectations

- The ECB’s QT challenge

- BoE likely to downshift

- PBoC unlikely to deliver cuts

- BoC’s Macklem to keep door the open

- SNB to follow the ECB

- Norges Bank to sound more cautious

- BanRep to deliver mega-hike

- Banxico expected to follow the Fed and inflation

- BSP likely to hike again

- CBCT has a little more wiggle room

- Is Russia done cutting?

- PMIs: EZ, UK, US (S&P), Japan, Australia

- Other macro

Monepalooza week is starting off with somewhat mixed evidence on risk appetite and light calendars. The week’s action will be packed into Wednesday through Friday.

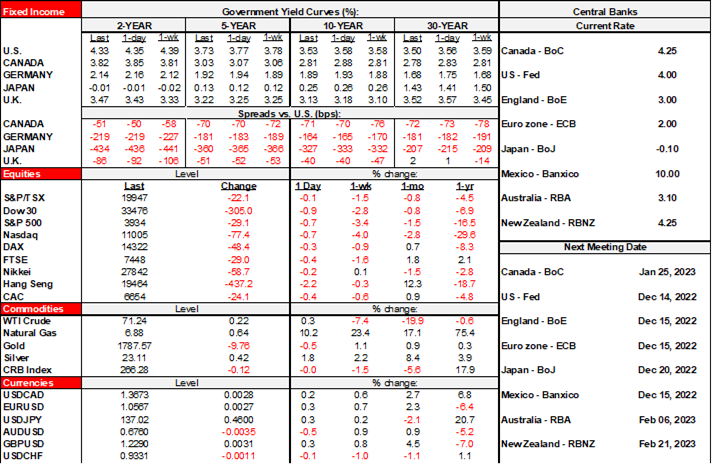

For now, stocks are mixed with N.A. futures in slightly positive territory and Europe little changed to slightly negative after Asian equities fell by up to 2.2% in HK. Oil prices are off by just under 1%. US Ts are richer by 2-5bps across the curve in a mild 2s10s flattener. Gilts are outperforming Treasuries and EGB curves are flattening. The USD is slightly softer and entirely due to mildly firmer European crosses.

There aren’t any great explanations for such mild moves. One theory may be that China’s relaxation of Covid Zero constraints is driving a more difficult to track surge in cases. Abandoning testing requirements has made that data unreliable. Anecdotal evidence is all we have to go by now and it includes remarks by health officials about pressures on the availability of medicines and services, hospital line-ups, reported hospital staff shortages, interruptions to other types of medical services etc.

Of course, another theory is just that there is such elevated risk into the back half of this week that sticking one’s neck out on risk appetite now risks a rude awakening in a few days.

Treasury Secretary Yellen said this weekend that there will be “much lower inflation” even in the absence of a recession by a year from now. Uh oh. In one sense that’s not really offering much since even just base effects and average monthly seasonal price changes would get inflation down to +/-3% y/y. What will matter in terms of tracking will be two more important factors. One is the m/m SAAR rates including breadth. Two will be not just the end of 2023 but over the full cycle ahead. In any event, recall that Yellen spent 2021 completely dismissing inflation as “small” and “manageable.”

A wave of UK releases generally exceeded expectations, but the data is stale, should be faded ahead of further downside risks, may have been distorted by the prior month’s holiday and period of mourning for QE II and is unlikely to matter to this Thursday’s BoE meeting. So there! Services expanded by 0.6% m/m (consensus 0.5%) in October. Industrial output was flat as expected. Construction output expanded by 0.8% m/m (consensus 0.1%). The trade deficit narrowed by more than expected. GDP was up 0.5% m/m (consensus 0.4%) as it rebound from the 0.6% prior contraction.

There is nothing terribly material on tap into the N.A. session. The US monthly budget update, India’s

BoC Governor Macklem delivers his annual holiday speech today. Headlines hit at 3:25pmET and there will be a press conference at 5pmET. I expect him to repeat much of last week's messaging especially on two counts. One is guidance that keeps the door to further hikes partially open on heightened data dependency which was made clear in the statement, the next day’s comments by DepGov Kozicki and also by former Governor Dodge. Second is to reinforce that there is a high bar that is set against acting in "forceful" manner again unless there is a material inflation shock (ie: returning to bigger hikes).

India will update CPI shortly after publishing (7amET) and Mexico will report industrial output for back in October at the same time.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.