ON DECK FOR THURSDAY, DECEMBER 1

KEY POINTS:

- Fed Chair Powell eased financial conditions…

- …that suggest less downside risk to growth…

- …amid a better-than-expected starting point for N.A. GDP growth

- US core PCE inflation softened…

- …but the debate remains whether that was a one-off or not…

- ...amid mixed evidence into the next update

- A decent month for US consumers

- US manufacturing contracted and so did price and job signals

- More China jawboning

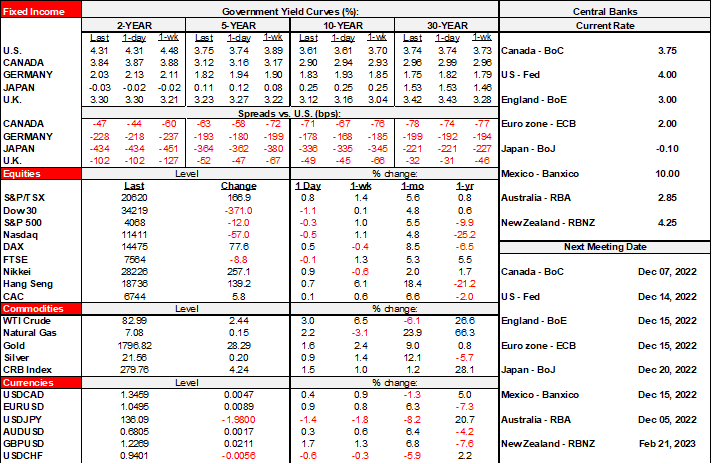

Spillover effects of Fed Chair Powell’s comments and developments in China are petering out as we transition into the North American session with early pricing indicating that both are now old news and so onto the next. US Treasuries are consolidating yesterday’s post-Powell richening with unchanged yields. Europe’s rates rally is simply catching up to the news that landed after local markets shut and so that’s why its curves are rallying. The USD is slightly weaker and mostly so in relation to Asian and European crosses as CAD softens and MXN is little changed. Oil prices are up by over US$2.

Why did Powell’s comments matter in a meaningful way? I’ll elaborate upon what he said below, but the main point is that when given the chance to lean against an easing of financial conditions over recent weeks he passed. In fact, he fanned further easing. The scorecard to date shows that the S&P has rallied by 14% since about mid-October, the US 10-year yield has declined by about 64bps from the peak in late October and driven a similar decline in the 30-year mortgage rate and the USD has depreciated by over 7% since late September on a DXY basis.

The question going forward is whether this is another Fed policy mistake at a still highly nascent stage of developments for inflation risk in the long game, or something that is durable in a more constructive sense. All else equal, easier financial conditions would support upside risk (or less downside risk) to growth projections that were established before these developments. This may, however, also suggest more upside risk to inflation and maybe that’s the signal that the Fed is sending in that it will tolerate some overshoot of its inflation target for some time yet and absent a desire to materially damage the other part of its dual mandate.

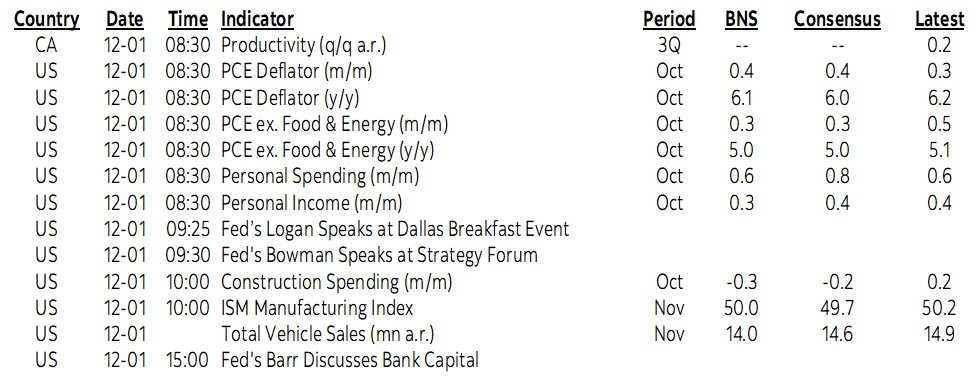

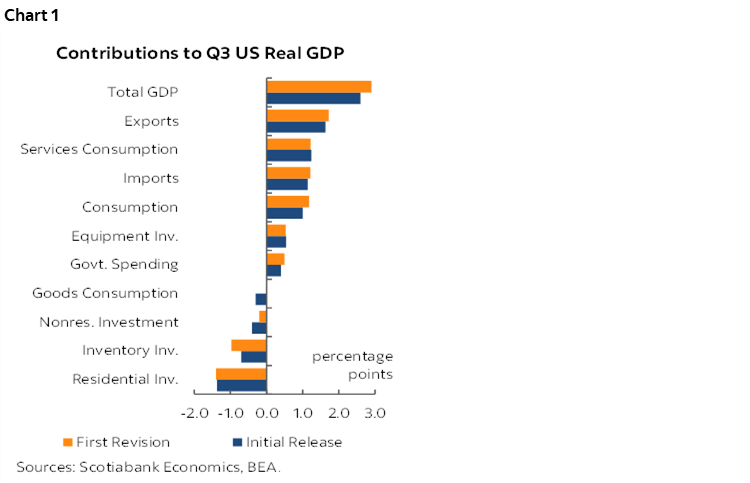

In addition to this, the N.A. economy is performing better than forecast of late. Our last house projections back in October expected the US economy to grow by 2½% in Q3 and we got nearly a half point more than that with fairly broad drivers (chart 1).

Our last house projection expected no growth in the Canadian economy in Q3 (+0.3% q/q SAAR) and we got almost three percentage points more than that with exports, services spending and government spending offering enough support to offset softer goods consumption and housing investment. I’ve seen some prominent folks dismiss Q3 GDP growth because it did have a strong export-driven component which I don’t understand. Canada is a trade dependent country benefiting from the terms of trade via commodities and currency influences. Much of the 1990s saw the trade side of the picture drive growth while the household sector was adjusting to the unwinding of prior excess. Why would you dismiss that driver now while also implicitly ignoring the strengths in services consumption and government spending? Some folks dismiss the latter as fake growth, but if the signal is that governments will keep on spending to support the economy then a dispassionate forecaster treats that as material information not to be ignored even while complicating the inflation fight.

On top of better starting points for GDP, layer on easier than expected financial conditions and, while tentative, one would have to think that the new information suggests that downside risks to developments are incrementally less acute from a firmer than expected starting point. Either that or the Fed is chickening out too soon and committing policy error; time and data will tell.

WHAT POWELL SAID

So what did Powell say? On the surface, Chair Powell's comments reinforced pre-speech pricing for 50bps in December and a 5% terminal rate by saying the September median estimate of the terminal rate could only move “somewhat higher.” That was enough to take out the tail view that it could move higher than that. Smelling weakness, ravenous markets even went a touch further as evidenced by the 15bps reduction of fed funds contract pricing for the terminal rate into Q2 next year (now 4.9% instead of 5.05%). All of this supports our expectation for 50 in December and another 50 in 2023Q1 and then stopping which means we’re getting closer to the point at which lagging pain on main street will rise through 2023 but when markets can continue to focus upon the other side.

But it’s the degree to which Powell left the door wide open to price easing that was arguably the bigger development. Powell said nothing obvious against easing next year by just saying policy will be "restrictive" for "some time" that he defines to mean real rates across the curve that are positive and above real neutral. That's a very wide interval and you could still be restrictive if a 5% Q1 terminal peak was cut later on in 2023. He could have more strongly leaned against any talk and pricing of easing but chose to leave it at saying policy will be restrictive for “some time” whatever that means. Markets have about 50bps of easing priced by the end of next year.

Powell’s remarks on the balance sheet were not new in that he further emphasized that SOMA roll-off will occur until the point at which reserves have been further reduced but not by pressuring estimates of the point at which they become scarce which the NY Fed’s analysis has tended to say is somewhere around US$2–2.5T. Reserves have already plunged from a peak of US$4¼ trillion in late 2021 to about $1 trillion less at present. Powell’s guidance married to the NY Fed’s estimate of optimal reserves would suggest that the Fed will pivot at some point in 2023 with a discussion favouring a tapering of the present US$95B/month pace of roll-off of maturing Treasuries and MBS.

So overall, my sense is that Powell’s comments signalled hike fatigue and did nothing to lean against materially easier financial conditions and hence fanned a further easing of financial conditions. We’re entering a wait-and-see period in which time and data will tell if inflationary pressures will durably subside in more than just year-over-year terms driven by base effects, or if easing financial conditions and a limit to the Fed’s resolve mean getting used to whippy guidance, volatile markets and persistent price pressures amid serial risks to inflation shocks for years to come.

CHINA DEVELOPMENTS

Other than the Fed, China’s propaganda machine kicked into higher gear overnight as a leading official who has guided Covid Zero’s implementation did not mention the policy and alluded to a different stage in combatting the virus. Vice Premier Sun Chunlan asks us to believe that China has vaccinated over 90% of the population with an effective vaccine and that merits a softening stance toward the virus. Uh huh. Credible studies indicate that its vaccine is vastly less effective than Pfizer’s and Moderna’s and unfortunately vaccine nationalism has compromised the health of its people. Nevertheless, she leveraged this point alongside noting that the omicron variants are generally less harmful in terms of outcomes to justify improving Covid Zero measures in small steps. We’ll see, as Beijing’s new Covid cases increased again overnight. The real test will come if cases continue soaring and further intensify pressures upon the healthcare system. It’s also well understood for quite some time that a main issue is the conflict between what Beijing says and what local officials do.

It’s unclear what narrative to subscribe to in terms of where China is going. I’m skeptical toward the end of Covid Zero narrative. I don’t trust many local analysts who operated within a heavily censored system that makes them afraid of questioning the state and yet that’s a lot of what we’re hearing out of China these days. But if China is truly pivoting away from Covid Zero in gradual fashion then get out of the way of a potential commodities steamroller in 2023 that would significantly benefit commodity dependent countries like Canada in the biggest gift that Xi Jinping could ever give to the country amid current tensions.

US INDICATORS

Indicators over the remainder of this week may further inform the balance of risks through Q4 forecasting and obviously with US nonfarm payrolls and Canadian jobs being the main focal points in that respect.

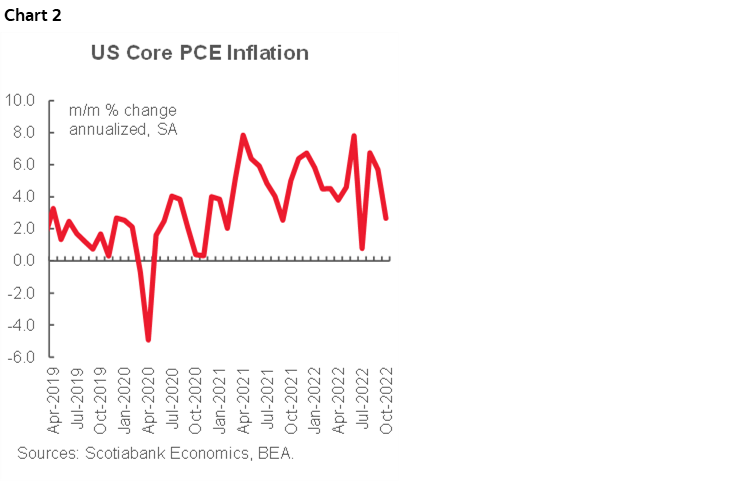

The main highlights today are coming through some US data updates. US core PCE inflation landed a tick beneath consensus at 0.2% m/m. The annualized rate slowed as per chart 2. The year-over-year rate ebbed to 5% from an upwardly revised 5.2% rate. Consumption grew by 0.8% m/m in nominal terms and 0.5% in real terms, both of which were in line with expectations on the heels of the strong gain in retail sales. Income growth was stronger than expected at 0.7% m/m (0.4% consensus). Jobless claims slipped back to 225k from 241k.

Now the debate at the margin is whether core inflation will be soft again in the November readings including CPI that lands the day before the next FOMC communications. The other two times this year that core inflation has slipped were both followed by renewed acceleration the following month. One argument for thinking the core PCE could be soft again in November is the discounting angle into holiday season sales.

The argument against that is as follows:

- we're seeing mixed evidence in the Cleveland Fed’s nowcasts. They show core CPI at 0.5% m/m SA but core PCE at 0.3% m/m SA. They're not infallible, but generally have a good track record.

- the discounting was late in the month. Inflation for November averages out the month.

- It's not obvious that the discounting was seasonally that much bigger across enough products this year to matter relative to discounting in the prior couple of years. See yesterday morning's note for the chart on that.

- Core PCE is likely to be more dominated by developments affecting OER and broader service prices that carry a much bigger weight than some of the retail goods categories.

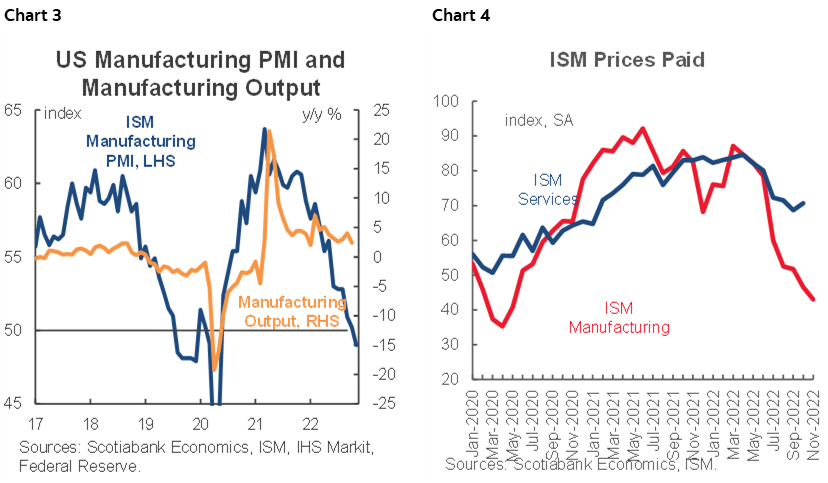

The US ISM-manufacturing gauge fell into contraction at 49.0 from 50.2 previously. Prices paid ebbed to 43 from 46.6 and employment slipped to 48.4 from 50.0. I could point to the very soft tracking these readings offer with respect to employment and prices, but that would likely fall on deaf ears in markets right now. For now, the decline in ISM suggests coming weakness for manufacturing production, but that measure is much less volatile than ISM (chart 3). Further, note that ISM manufacturing prices paid are falling much faster than services (pending ISM-services later) and ISM-manufacturing prices paid is mostly driven by commodities.

Canadian bank earnings season is now largely over with a hat trick of releases this morning that wraps it up for the so-called ‘big 5’ or ‘big 6.’ Two out of three missed this morning which means that for the overall season three beat (BNS, RBC and TD) while two missed (CIBC and BMO). CIBC significantly missed with adjusted EPS of C$1.39 (consensus $1.72). BMO also missed but by less than CIBC with adjusted EPS of C$3.04 ($3.07 consensus). TD beat with adjusted EPS of C$2.18 (consensus $2.06).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.