ON DECK FOR WEDNESDAY, AUGUST 31

KEY POINTS:

- Bonds on the run as ECB bets intensify

- August’s bond market was more about the ECB’s later pivot than the Fed

- Eurozone inflation was stronger than expected…

- …prompting hawkish guidance and higher bond yields

- China’s PMIs weakened again

- PBoC sets another higher fix in a losing battle

- Canadian GDP to inform cooling narrative

- Ignore US ADP payrolls

- The FOMC gets a new voice

- Otherwise mixed Asian macro readings

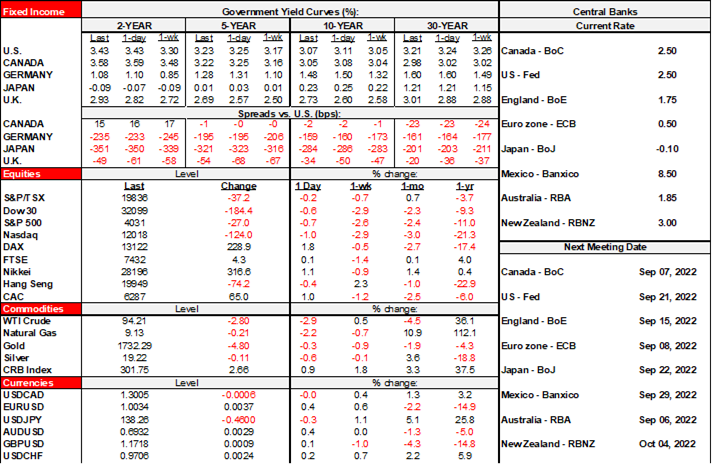

Sovereign yields are on the march higher again this morning and primarily due to Eurozone inflation and ECB bets (see below). Italy’s curve is leading the way with a bear flattener led by an 11bps rise in 2s, but significant increases are sweeping across EGBs. Yields on gilts are up another 10–11bps across the curve partly due to carry out of the Eurozone inflation readings and partly because the ONS stated that energy rebates won’t factor into CPI calcs. Spillover effects through carry are driving US Treasury and Canadian government yields higher by about 3–4bps across maturities. That’s hitting equities again although less so than earlier this morning perhaps given jawboning out of China (see below) with present European cash markets trading between little changed in Germany to down by as much as 1% in London. US and Canadian equity futures are performing a little better with Toronto flat while S&Ps are up by a mild ¼%. Oil is down another ~$3. The USD is picking up some safehaven flows along with the yen.

Eurozone CPI surprised higher and markets reacted by leaning a little further toward pricing a 75bps hike next week and adding a few basis points to the cumulative path over coming months. In fact, the cumulative changes in market pricing for cumulative ECB rate increases between now and next June has gone up by much more over the month of August than has been the case for the Fed that pivoted earlier (chart 1). Heck, for that matter, while almost all global central banks woke up to rising inflation risk too late, the ECB slept in the latest. Headline CPI climbed two-tenths to 9.1% y/y (9% consensus) with prices up 0.5% m/m (0.4% consensus). Core CPI was up 4.3% y/y (4.1% consensus, 4% prior). Chart 2 shows the readings flying off the y-axis. The firmer than expected reading was primarily due to Italy’s readings this morning. Italian CPI was up 0.8% m/m (0% consensus) and 9% y/y (8.2% consensus, 8.4% prior). France was a bit softer than expected at 0.4% m/m (0.6% consensus) and 6.5% y/y (6.7% consensus, 6.8% prior). This follows the other day’s German and Spanish figures that were largely in line with expectations. Inflation expectations over the longer run are on or slightly above target which should counsel policy normalization instead of a policy rate around 0% if the central bank treats its inflation target with any seriousness (chart 3).

ECB Governing Council member and Bundesbank President Nagel was quick to react. He said that “There is an urgent….to act decisively at its next meeting to combat inflation. We need a strong rise in interest rates in September.”

European consumers are feeling the pinch effects with French real consumer spending down 0.8% m/m in July (-0.2% consensus) after a flat June and a string of generally weak readings back to last year

China’s PMIs weakened again in the August readings that came out overnight and mainland equities fell. The composite PMI slipped to 51.7 from 52.5 and confirms that the improvement in June was a transitory reopening effect after which this indication of growth in China’s economy fell for the next two months. The non-manufacturing PMI led the way lower (52.6, 53.8 prior) as the manufacturing PMI held steady and was slightly in contraction territory (49.4, 49 prior).

Cooling Chinese macro readings in a weak economy and relative PBoC-Fed bets forced the PBoC to set a stronger yuan fix for the 6th straight session. The effect of the fix was to set the yuan back to basically where it was at this time yesterday as it continues to hover around 6.9 and hence about 9% weaker over the past six months. We’re also seeing some jawboning out of China about vague plans to add stimulus measures.

Asian factories put in a mixed performance. Japanese industrial output was up by 1% (-0.5% consensus) and retail sales were also stronger than expected (+0.8% m/m, 0.3% consensus) although in both cases we’re getting significant lift effects from prices and partly due to yen weakness. South Korean industrial output, however, gave back most of the prior month’s gain and fell 1.3% m/m in July.

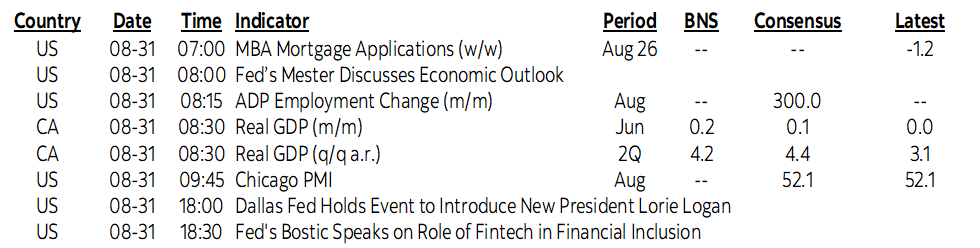

On tap for this morning is Canadian GDP (8:30amET). Watch for cooling momentum. Q2 should be strong (consensus 4.4% q/q SAAR, Scotia 4%), but the economy contracted in the month of May, likely squeezed out modest growth in June (consensus 0.1% m/m, Scotia 0.2%) as we get the more complete estimate, and then the first ‘flash’ reading for July probably faces downside risk. If so, then that sets up a weak Q3 with Canadian GDP growth having been brought forward into the H1 outperformance. That said, this is necessary with the economy having pushed further into excess demand in H1 so a lot more damage is likely required on the demand side going forward.

US ADP payrolls will be reintroduced after it was suspended in order to work on a new methodology. Again. Every time they do this it winds up being just as useless as before. Given that ADP has tracked private nonfarm payrolls very poorly over time it will take some time to assess whether the new methodology is of any use. Of course, like nonfarm, neither measure will capture what’s happening to most of the small business sector and so we still need to track the volatile household survey over time which has been the weakest of the bunch for several months now.

We might hear the new Dallas Fed President’s views that matter because she gets a vote when the calendar flips to 2023 and her views are not well known (6pmET). I’ve met her through meetings with the markets group at the NY Fed and she always struck me as thoughtful and measured. Cleveland Fed President Mester is also set to speak (8amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.