ON DECK FOR TUESDAY, AUGUST 30

KEY POINTS:

- Possible drivers of risk-on sentiment

- German CPI likely to land on consensus

- Soft Spanish inflation matches consensus

- Higher yuan fix fizzles

- US consumer confidence might improve: watch jobs and inflation readings

- US JOLTS to further inform coming nonfarm softness

- Canada: business conditions survey, last of ‘big five’ earnings

Risk-on sentiment is being restored so far this morning while the rates complex settles down somewhat. There are multiple possible theories other than just late-August noise, but no clarity on which one(s) and possibly others may be on the mark.

- Maybe we’re at the point at which markets realize that Jackson Hole is best treated as something to fade soon after its conclusion given the track record of guidance that we’ve heard from the event through the pandemic to date.

- And/or maybe sentiment is guided by preliminary Eurozone inflation readings that are at least no worse than expected (see below).

- Maybe lower oil prices are helping inflation sentiment and hence yields and equities. There is speculation around the margin on supply disruptions that is at least temporarily positive (Iraq, Libya). I would tend to think the pressures on oil prices are still pointed higher on net going forward.

- Or maybe it’s the relatively dovish waffling by ECB Chief Economist Lane who prefers a slow and steady approach on rates in order to evaluate the effects of hikes. This follows comments from other more hawkish ECB officials over recent days. In my view, Lane’s approach might have been more suitable 6–12 months ago. His stance may overly downplay the facts that inflation is running at multiples of the ECB’s target and likely to move higher yet, the euro has been sliding which adds to some imported pressures, and the policy rate is still highly stimulative at a great distance beneath any estimate of the neutral rate range. If the ECB has an inflation target that its serious about then it arguably should already be at neutral but it seems to have the most laid back stance of any notable central bank.

- Also, China tried to lean against yuan weakness once again overnight which may be interpreted as an effort to stabilize local markets. Once again it didn’t work out so well as the FX forces that are being fought are more powerful than can be handled by repeatedly adjusting the fix (see below).

- And lastly (for me at least) we’re getting toward month-end rebalancing after a month that involved large moves across fixed income and so traders might be salivating toward more attractive entry points soon enough.

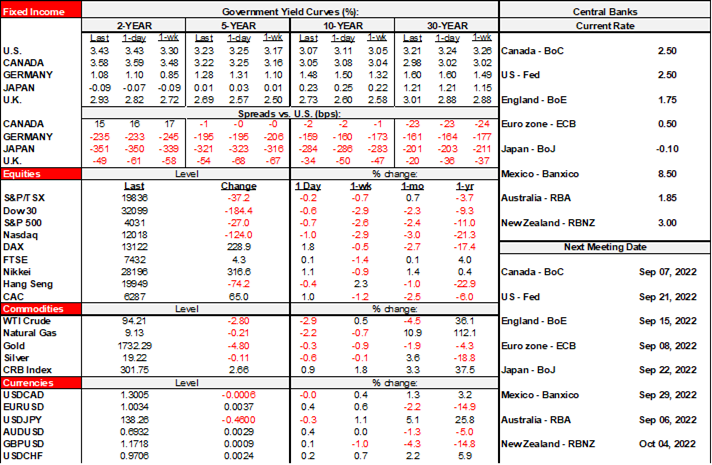

Whatever the driver(s), US equity futures are up by almost ¾% with TSX futures up by half of that and European cash markets mostly 1–2% higher. London is an exception with flat equities and a double digit rise in yields on gilts as it catches up from yesterday’s holiday. Other sovereign yields are mildly lower with US Ts and Canadian GoCs slightly bull flattening in 2s10s and EGBs richer across the curves. Broad USD softness is occurring against most major crosses with a largely ineffective higher yuan fix being mostly shaken off. Oil is off by about three bucks.

Germany and Spain are reporting headline inflation figures that are close to consensus expectations.

Spanish CPI was in line with expectations on an EU-harmonized basis. CPI was up 0.1% m/m and 10.3% y/y. German CPI was up by 0.4% m/m which met expectations. Individual states had all landed at 0.3–0.4% earlier this morning in advance of the national add-up and so there is no incremental surprise. That’s not to say that Germans will take inflation at 8.8% y/y lightly, but at least it’s not an incremental shock today. France and Italy arrive on Thursday just ahead of the Eurozone add-up. Reasons to fade the numbers include probable coming upside risk to inflation readings given risks around Russian energy supply into winter and the impact of drought across Europe (and North America).

China set a higher fix for the yuan again overnight. Once again it didn’t help much as the yuan rose slightly against the USD but is underperforming other crosses amid general dollar softness this morning. A combination of a hawkish Fed and China’s multiple downside risks to growth continue to drive a weakening trend for the yuan that continues to trade just beneath the psychologically important 7-handle with about an 8% depreciation since April.

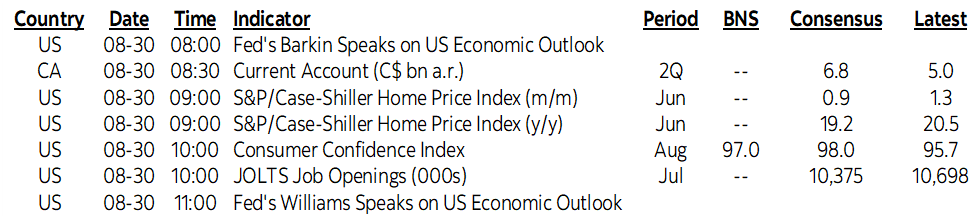

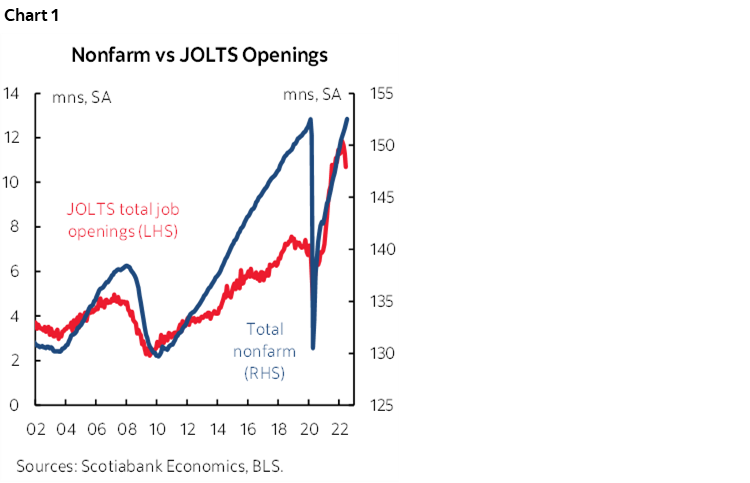

US job openings will also be updated with lagging July figures (10amET). Openings have pulled off the peak which tends to lead a decline in nonfarm payrolls so watch for any further erosion this morning (chart 1).

US consumer confidence will be updated at the same time (10amET) with an August set of estimates and is expected to improve given strong labour markets and lower gasoline prices. It also contains measures like job availability and 1-year ahead inflation expectations. There will also be some light Fed-speak with Barkin (8amET) and Williams (11amET) on the docket.

Statcan will update the Q3 edition of the Canadian Survey on Business Conditions this morning that assesses business sentiment across a variety of variables over the coming quarter.

BMO was the last of the ‘big five’ Canadian banks to report earnings this season and it disappointed expectations with adjusted EPS of C$3.09 (consensus $3.15). That makes for 3 misses and 2 beats across the individual banks’ Q3 results for a generally soft overall tone.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.