ON DECK FOR FRIDAY, AUGUST 26

KEY POINTS:

- Markets may express relief on Jackson Hole day…

- …if Powell sticks to his narrative at the July FOMC presser…

- ...and after markets spent August aligning more closely to the SEP & dot plot

- US PCE inflation might land softer than CPI as an awkward segue into Powell

- US consumption likely grew on income gains

We’ll soon find out if this year’s Jackson Hole is a bigger deal for the cottage industry that has built up around it including media coverage than it is for the markets as the dominant consideration to end the week. Several other Fed speakers will continue to appear. Here is the full agenda that was released last evening and also continue to watch for possibly more from the sidelines over the next couple of days as that’s the only hope for any real global content. The formal agenda makes it clear that this is almost exclusively a Fed-focused and US-centric event that is lacking much of any global content as it takes until the final event tomorrow morning to bring out any foreign central bank participants and there are rather limited expectations for that four-person panel. We’ll see if the likes of Bailey, Kuroda and Macklem say anything meaningful from the sidelines.

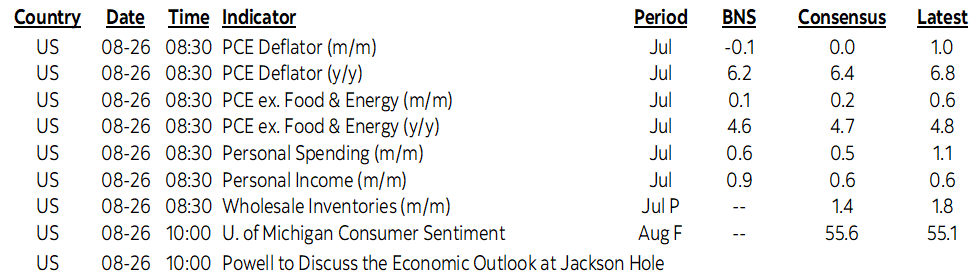

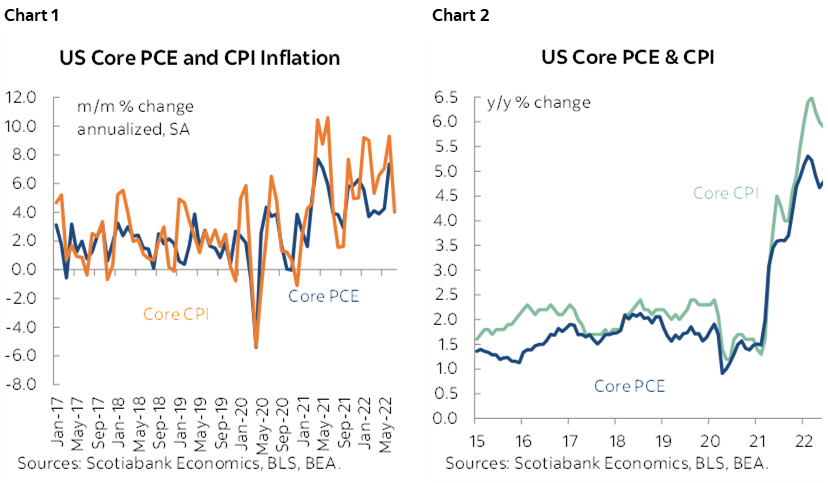

Data risk will primarily focus upon U.S. PCE inflation readings. See my estimates in the ‘on deck’ table. We know that CPI was flat m/m and core CPI was up 0.3%. We also know that PCE has been tracking more softly than CPI for a while in both m/m and y/y terms (charts 1, 2). Part of the reason for that is that PCE has a lower weight on some of the hotter and more resilient categories like housing drivers in addition to the fact that PCE shifts spending weights dynamically in accordance with changing spending patterns. Hence, I’ve gone below CPI for both headline and core CPI and a little below consensus which could be an awkward segue into Powell’s speech from a market standpoint. Otherwise, US income growth was probably strong in July given the gain in jobs and wages that should pop overall compensation higher. There was probably a decent gain in real consumption given a) softer price changes and b) a solid gain in the retail sales control group (+0.8% m/m).

Regardless, it’s JPow’s fancy dance moves that will no doubt captivate all of us. I hope he has good hips. He’s going to need them! Image. Speech at 10amET, no Q&A or presser. Several Fed officials will speak just before him, but I think we’ve heard enough from them of late with the focus upon Powell. Fwiw, Harker speaks at 9amET, Bullard at 9:15amET and then Bostic at 9:30amET with Mester batting in the bottom of the order at 11:30amET.

How might markets react to JPow? A trading maxim is to buy the rumour and sell the fact. For Treasuries, the opposite may be holding true into the speech in a buy the fact sense if he sounds no more hawkish than he did just a scant few weeks ago and relative to how markets woke up over that intervening period. If market conditions circa the end of July still held today, then it might be a different matter. Market movements so far this month, however, have brought Treasuries and the short-term rates trading complex much more closely in alignment with the June dot plot that Powell had said was still valid along with the rest of the SEP projections when he spoke during the July FOMC presser just a few weeks ago. It’s doubtful that he’s had another epiphany since then. In fact, I would expect much of his narrative to be similar in nature to what he said on July 27th including cautious optimism while emphasizing their sole focus is getting inflation under control whatever the consequences. If I were him, I would sink more effort into setting a high bar against prematurely declaring victory against inflation as job #1 tomorrow so he doesn’t ease financial conditions and to make it clear that they’ll hang out at a cycle peak for a lengthy period until they have high confidence that inflation *may* come in line with their 2% target. That’s because inflation has shorter-term drivers but also longer wave ones and I think the game has changed on the latter. If he doesn’t set a high bar to future easing then the FOMC’s inflation fight may look more like the keystone cops in action as they seek to tighten while forward-looking markets price easing.

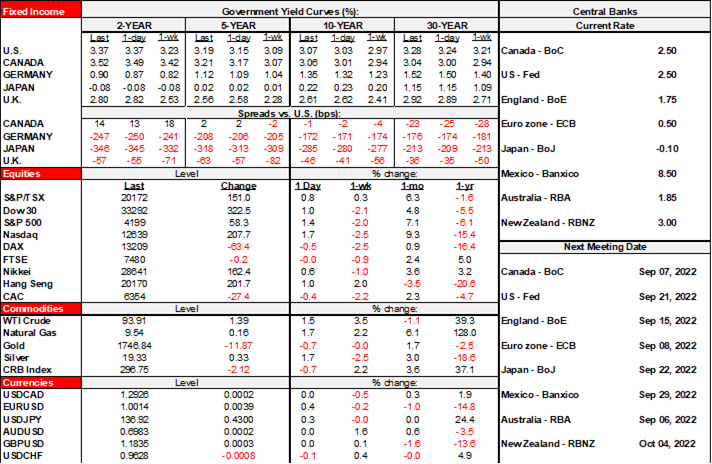

Fed funds futures are priced for a peak 3¾% policy rate which matches the median FOMC don’t-call-it-a-forecast, although perhaps a touch too slowly. Some of the prior market bias in favour of rate cuts has been pushed out and tamped down with just a little over a quarter point of relief now priced for later in 2023. That’s probably still aggressive at least given my bias that the Fed realizes it will break a few teacups without being knocked off course and will set a high bar against prematurely declaring victory against inflation. At this stage I wouldn’t even begin to contemplate rate cuts until at least 2024 and only modest ones. For now, I think a reasonable range for this year is 3.5–4% with strong risk of going over 4 and my year-end 3.1% US 10s forecast is finally looking a little better these days.

For now, central bankers are likely to be more focused upon inflation risk than attempting to be overly confident in forecasting actual inflation and that’s likely to keep them sounding hawkish. The Fed knows that it sucks at forecasting inflation; hence how we got here as models are incapable of dealing with today’s drivers. Monetary policy has to be managed toward addressing the direction of inflation risk relative to the target and I think inflation risk is still skewed higher. Think drought in Europe and the US and the connection to basically everything you and I eat going forward. Think sundry energy market risks from Europe’s looming winter to talk of a triple dip “La Niña” winter effect in the north to lower US crude inventories to the Saudis and my personal hope that the hawks in Congress shoot down any second attempt by Biden at Obama’s naïve and wishful thinking toward the West-haters in Iran’s regime. Think pass-through into core and the risk of a further unmooring of inflation expectations that could feed wage setting exercises in tight labour markets with US payrolls up by a whopping 3¼ million jobs ytd.

By the way, consensus predicted one million fewer jobs than that and so we’ve all been taken aback by the strength of the job market in 2022, although the household survey’s gains were entirely in Q1 before weakness in Q2. A clear caveat is that job growth is a contemporaneous indicator and the unemployment rate lags, so it’s a bit frustrating to hear some Fed officials intimating that present readings somehow inform future recession risk. That’s not only a violation of common sense economics as it’s also incredibly disingenuous by folks who know—or should know—better. Maybe they thought the GFC wasn’t going to happen because job growth was still positive until early 2008…errr… actually, never mind, that’s exactly what they thought at the time!! We’re in good hands folks….

And my thematic inflation narrative continues to emphasize how it is very early days for c-suites to be fundamentally revamping supply chains after serial shocks from Trump’s trade fights to the pandemic and the Ukraine war and sundry other regional geopolitical challenges from Iran to Taiwan. The old outsourcing model that was solely focused upon lowering operating expense has been replaced by heightened concern toward operating risk that raises financial distress costs including outright bankruptcy with stranded assets. To manage this, will companies boot JIT and hold higher inventories and pass on the higher storage and financing costs so that they still have product to sell the next time serial shocks arise? Hire locally and produce locally at lower economies of scale? Come closer to home? Invest much more to revamp everything? And pass on all of the higher operating expenses as a trade off to lowering operating risk? China has more to lose here if so than most others and perhaps more so for its cheaper neighbours.

Add to this the possibility that other structural drivers of inflation are shifting higher. Like more restrictive trade policies. Technology may be less disinflationary through increased contestability and lowered information costs and now more about market power being exercised by concentrated firms that can afford it the most. Like aging populations and their impacts upon slower growing workforces and medical care inflation. Like carbon pricing. The point here is that it’s the uncertainty around the long-wave drivers of inflation that matter and models will only pick those up in lagging fashion to the reality just as they did on inflation’s downslope.

A final wish for Powell’s speech is that it will be free of any defensive nonsense. The Fed messed up, so move on. A more circumspect and balanced approach to inflation risk at a far earlier stage would have tightened financial conditions before being prepared to hike and this could have lessened inflation risk. Instead, all I heard until December last year was that inflation was definitely transitory and that the prime goal of monetary policy was apparently 110% inclusive employment. Well, we got the latter, alongside a regressive and nasty inflation tax.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.