ON DECK FOR FRIDAY, APRIL 8

KEY POINTS:

- Risk-on sentiment has light catalysts

- China’s Li reinforces PBOC easing speculation

- China’s totalitarian COVID-19 measures

- RBI pivots toward market pricing for hikes

- Can Canada post another increase in employment...

- ...with wage growth rebounding?

- Canada’s thankfully useless new homebuyer incentive

- Russia’s central bank cuts…

- …after FX manipulation through capital account restrictions

A general risk-on bias did not have any significant catalysts behind it until China’s Premier Li spelled out the blindingly obvious point that the economy faces greater uncertainties and that policy measures need to be increased. That will further amplify speculation toward a PBOC rate cut next week. In fact, what may suggest incremental caution are accelerating lockdowns in China and more intense pressure to escalate measures against the murderous Russian government given more civilian bombings overnight. Other developments are affecting regional markets.

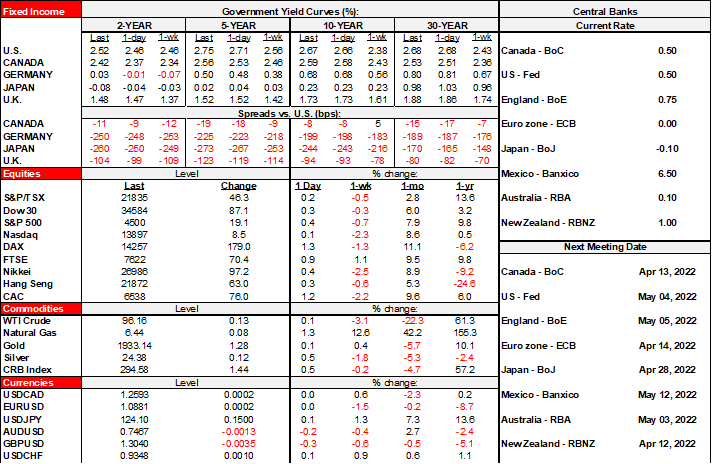

Regardless, stocks are in the black with European cash markets leading as gains of 1%+ are being recorded while N.A. futures are up by about ¼%. The USD is little changed overall. US Treasuries are underperforming other major markets with the 2s10s curve bear flattening as the two-year yield is up 6bps.

Hate COVID-19 restrictions? Count your blessings. China is rounding up hundreds of thousands of folks in Shanghai who test positive regardless of symptoms and anyone they interacted with and forcing them into isolation facilities. Oh the things you can make people do when they have no rights whatsoever…

Russia’s central bank unexpectedly cut its key rate by 300bps to 17% in an inter-meeting decision this morning. The central bank guided that further easing may be possible at its scheduled meeting on April 29th. The move is likely designed to address a strengthening ruble. The ruble has risen toward pre-invasion levels on central bank manipulation. The central bank had blocked USD withdrawals from bank accounts and banned the sale of all foreign currencies to residents while blocking foreign sales of domestic securities and hence rubles. This FX manipulation has given it the room to cut rates, but not without its costs. Restricting the capital account can foment domestic imbalances by not allowing a flexible exchange rate to adjust to shocks more effectively and can introduce welfare costs and deadweight losses to the economy.

The Reserve Bank of India held its repo rate at 4% as expected, but formally shifted toward a hiking bias. The main statement adjustment that indicated such a pivot was the removal of a line referencing how it would maintain an accommodative stance due to COVID-19 “for as long as necessary.” It also hiked its inflation forecasts given recent developments. The two-year Indian yield increased by 15bps overnight and the rest of the curve cheapened by 9–15bps as the rupee was little changed but outperformed other Asian crosses to the dollar overnight.

Circling back to the Canadian budget’s housing implications, one point of clarification is that the new Tax-Free First Home Savings Account (FHSA) is not new stimulus per se. In fact, we were all duped by yesterday’s budget when the propaganda failed to note key limitations. That’s because an initially buried detail is that you cannot use it and the existing Home Buyers Plan on the same purchase transaction. I think that’s a good thing because I don’t like more housing subsidies and it makes little sense to me to have monetary policy tightening interest sensitive sectors while fiscal policy overheats them. But what this will do may be to effectively kill the HBP and with it a significant chunk of each year’s RRSP contributions as the programs will compete against one another. The FHSA will be more attractive to some than the HBP because as near as I can tell you don’t have to repay what is withdrawn from the program, unlike the HBP where withdrawals must be repaid within 15 years but without making up for the lost time value of money. That said, the FHSA has no carry-forward on annual unused contribution room of $8k/yr which a) says use it or lose it each year unlike RRSPs, b) if one has a lot of unused RRSP contribution room then you still might prefer the HBP, and c) says that the phase-in period for the program will be a slow fuse over years that won’t do much for housing. And so with that, the FHSA’s cumulative limit of $40k and the HBP’s limit of $35k—both per person—are substitutes; you must pick one or the other, but not both. That makes it a wash in terms of housing effects and effects on related issuance and the rest of the initiatives they announced involve very small forms of token assistance to first-time buyers. That’s all good news, unless you would prefer worsened affordability pressures that would stem from higher taxpayer funded subsidies to home buyers!!

Otherwise, the Federal budget was a disappointment in my view. Rebekah did a fantastic job at turning out this piece right out of the lock-up. In my opinion, there was nothing material in the budget that was designed to address the real issues in the economy such as moribund productivity growth beyond a couple more cumbersome government agencies to be run by government types. Fortuitous revenue gains were spent on trinkets. Keeping some powder dry in the deficits likely makes sense given uncertainties around the outlook for the economy. Lowballing nominal GDP forecasts by using stale numbers, however, has the effect of lowballing the Budget’s estimates of future revenue growth. They may well wind up facing further revenue upsides that will give the government more money to spend and drive greater incursions into the private economy. Going forward, the improvement in the deficit-to-gdp ratio is welcome, but it’s the by-product of sheer luck through the inflation tax and commodities. The improved path may also very well prove to be a budget head fake; the left-wing collusion between the Liberals and NDP is likely keeping some powder dry to spend on trophy platform items like pharmacare closer to the next election rather than peaking too early. For now, the industrial policy remains hatefully maligned against successful and important sectors like energy and banking.

Canada updates job figures for March this morning (8:30amET).

- CDN jobs preview:

- Scotia: +125k

- Consensus: +80k

- Range: 0k to +125k

- Std dev : 38.1k

- Very wide dispersion of estimates across the whole range with slight clustering above 80k–120k.

- UR: 5.4% consensus, 5.5% prior, 5.2% Scotia.

- 95% confidence interval: +/- 58k

Drivers:

- every time we’ve had a gain of 337k or more like we did in February, the next month has been up by between about 90k–400k with an average of about 230k.

- Stringency measures declined across all provinces to the lowest since the early days of the pandemic. There was significant easing between Labour Force Survey reference weeks into March.

- Several mobility and business register gauges improved.

- the Ivey PMI employment gauge climbed in March to its highest reading since last September.

Also watch wages to see if they rebound from the stalled out growth in February, just as US wage growth rebounded.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.