ON DECK FOR WEDNESDAY, APRIL 7

KEY POINTS:

- Markets consolidate trades around the Fed’s exit plans

- FOMC minutes delivered on advance hawkish positioning

- Will the PBOC ease next week?

- Canada’s Federal Budget will be out of touch

- Mexican inflation lands a touch firmer than expected

- Bullard goes rogue

Easing clues out of China and consolidation of pre-FOMC moves are the dominant forces in world markets this morning. Regional developments will focus upon Mexican inflation and Canada’s Federal budget.

Earlier this morning, consolidation trades around the Fed minutes (recap here) were only slightly taking away some of the rates selloff that occurred in sessions leading up to the minutes that were expected to lay-out an aggressive balance sheet plan. And so they did. Those plans broadly met expectations so the rates selloff was capped. Some of this consolidation of market effects is already being shaken off. The US 10 year Treasury yield is back up to yesterday morning’s highs and about 25bps higher than where it exited last week. The US 2-year yield rallied by ~4–5bps since 2pmET but that takes us back to where we were on Tuesday morning with 2s roughly unchanged on the week. The USD is little changed since before the minutes, but about 1% dearer on the week so far. Some folks call that a dovish reaction to the minutes, whereas I would just call it a consolidation trade in relation to the market’s prior hawkish positioning ahead of the minutes that were broadly validated.

Language from China’s State Council motivated speculation that the PBOC could cut its medium-term lending facility rate next week. The Council said that downsides risks that in some respects have exceeded expectations would merit using some form of monetary policy response without providing firm guidance on timing or how. China’s economy has been facing serial downside shocks for quite a while now and with no end in sight. Its monetary policy was always too tight into the shocks given its status as having among the world’s highest positive real policy rates with inflation far below target, while property financing risks, rolling COVID-19 shocks and policy responses and the impact of COVID-19 and war upon its key export markets combining with a negative terms of trade shock as a commodities importer. Overly tight policy has not been helpful in the context of such challenges and is the greater risk to stability than easing.

German industrial output landed weaker than expected due to revisions, but it’s stale pre-war data anyway. January’s 2.7% m/m rise was revised down to 1.4% and so that negates the fact that the 0.2% rise in February was in line with consensus expectations for that month.

Mexican CPI inflation landed in line with expectations largely because of the running head start provided by virtue of the fact that bi-weekly gauges are available. CPI landed at 7½% y/y (7.3% prior) and marginally higher than expected. Core inflation hit 6.8% y/y (6.6% prior) and also marginally higher than expected.

St. Louis Federal Reserve President James Bullard delivered this presentation this morning. Markets largely shook it off despite his increasingly hawkish positioning relative to the rest of the FOMC and given his status as a voting member this year. Bullard provided scenarios using Taylor rule assumptions that could merit a fed funds terminal rate of 3½% this cycle and with bi-directional risks that net out to positioning himself above his colleague’s estimates of the terminal rate as provided in the March dot plot and Summary of Economic Projections.

US weekly claims fell by much more than expected with downward revisions, but the effects should be faded. Claims fell to 166k last week (200k consensus) and the prior week was lowered to 171k (202k prior). The BLS explained that major adjustments were made to how seasonality is addressed. In essence, the BLS has reverted back to the way seasonal adjustments were being made before the pandemic when they switched up methods to address the unique distortions brought on by it. I would fade the decline in claims a) because of this methodological change, b) because it’s unclear how much of the drop is genuine, and c) because claims are not a greater indicator of what to expect for nonfarm payrolls in any event.

CANADA’S FEDERAL BUDGET WILL BE OUT OF TOUCH

Canada releases its Federal budget when the Minister of Finance Chrystia Freeland stands to commence her speech and the embargo lifts shortly after 4pmET. Scotiabank’s Rebekah Young will be in the lock-up all day doing her write-up for release soon after the embargo lifts. Her advance preview is here and her updated perspectives were offered in my Global Week Ahead here. There has also been a fair amount of new information on offer through media outlets in the past week. Many of the budget’s core features have been communicated in advance as per the common practice that is designed to control the spin with favoured journalists and to turn it all into a week-long affair—and then some!

For my two cents, I already think the Budget is going to miss the mark in relation to what the economy needs. With inflation soaring, productivity tanking, deep challenges to housing affordability, the bond market puking and war raging, it seems likely that we’ll see a plan that offers more spending, more government incursions into the private sector and more tax subsidies to housing demand all of which may well further reinforce the need for tighter monetary policy. Market effects around Canadian federal budgets are usually scant to none partly because other factors swamp their significance and because the effects are leaked out in dribs and drabs against other more dominant global and domestic market forces. Still, such market effects can be informed over time and what markets don’t want to hear now is a bias toward fanning inflation and concomitant risks to borrowing costs.

Some concerns and some kudos are offered below.

Stale Forecasts

The budget will be based upon private sector economists’ forecasts that were sought by Finance before the war broke out and before pressures upon inflation and bond markets intensified. Why updates were not solicited is unclear, but at least it’s not as bad as the Biden administration’s Budget reliance upon CBO forecasts from last November because by its own admission the CBO said it has been simply too busy to update them….

Fiscal Policy and Monetary Policy in Competition

For one, while the Bank of Canada finally pivots toward getting serious about inflation, Ottawa’s spending focus will go the other direction over time and in such fashion as to pit monetary and fiscal policy against one another in efforts to manage soaring inflation. It would do so even by maintaining present elevated spending before considering further spending increases. Uncoordinated policy will make the inflation fight more complicated and prolonged in ways that will add to what Canadians pay in interest on their debts.

Plunging Productivity? Meh!

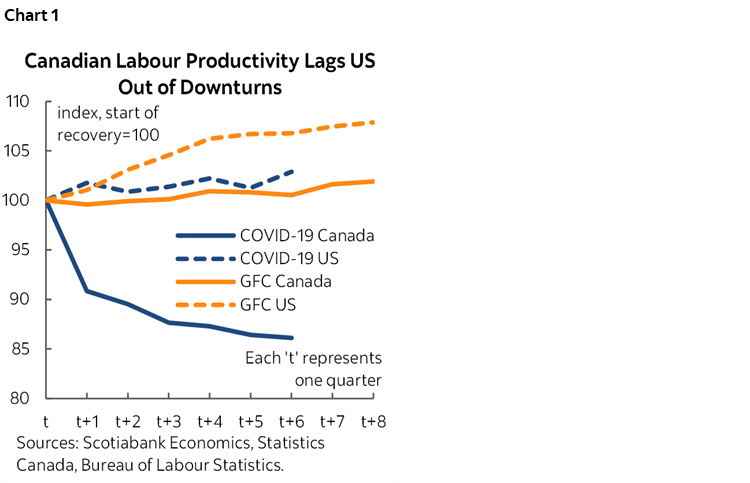

For another, nothing I’ve seen will even attempt to address the nation’s #1 economic challenge: moribund productivity growth. It is plunging in Canada in absolute terms and relative to the US (chart 1). Over time, sagging productivity growth harms longer run living standards. Governments cannot spend their way to prosperity with social programs. Some policy stances may worsen the effects on productivity.

Housing

Further, Ottawa is going to throw more stimulus at a housing market that doesn’t need it and that will complicate the Bank of Canada’s efforts and those of OSFI to cool it all. I’m ok with more money for affordable housing given serious shortfalls but stimulating first-time home buyers is misguided given the need to cool interest sensitives if we’re to have a chance at cooling inflation.

Ottawa’s plan to introduce a new First-Time Home Savings Account that offers tax free savings and a $40k withdrawal limit may worsen affordability over time. It adds to tax subsidies to housing that already include the Homebuyers’ Plan that offers a tax deduction on the RRSP contribution, then up to $35k withdrawal limits (twice that if a couple) and with the weak obligation to eventually repay it but without making up the lost time value of money. Further, the Tax-Free Savings Account does not offer a deduction but shelters investment income from taxes with a $6k annual contribution limit indexed to inflation and the withdrawn proceeds can be used for absolutely anything including down payment on a home.

Key are the first- and second-round effects on house prices in that the market adjusts to a new equilibrium every time they tinker with housing subsidies. Housing is likely to get more expensive at entry levels and with effects that bluntly sweep across the land given no effort to tailor them to local housing market conditions.

And who benefits the most from the tax subsidies? Arguably the folks who don’t need them. The ones with parents who can transfer/gift down payments one way or the other and let their kids apply tax leverage. The higher income earners who are better able to sock away the contribution limits to such programs. The ones who can borrow through other channels to get the tax leverage. The ones who are couples over singles amid the explosive rise of single-occupant households. All the while the after-tax cost of housing is favoured over other investments while cannibalizing other forms of saving.

Some may cry out that more housing subsidies are needed because of higher interest rates. Huh? Higher interest rates are designed to cool interest sensitive sectors like housing and the associated inflationary impulses. That’s the whole point of tightening monetary policy. In any event, the rate pressures at the point of qualifying are not that much higher than what the market had already adjusted to under B20. Qualifying had already adjusted to the 5 ¼% B20 guideline given that for years it was the de facto qualifying rate when the contract rate plus two percentage points was persistently running beneath 5 ¼%. With the bond market having significantly adjusted to market expectations for the BoC’s neutral policy rate, today’s 5-year mortgages around 3 ½% or a little higher plus the 200bps B20 buffer now make the de facto qualifying rate 25–50bps higher than what the market had already adjusted to. In other words, if folks could qualify at 5 ¼% and still drive hot housing, then an added 25–50bps on the qualifying rate isn’t going to tank the market especially as more fiscal stimulus and higher immigration are added to tight supply.

Hitting Canada’s International Reputation

A two-year ban against foreign ownership of Canadian residential properties is xenophobic fear mongering. It scapegoats folks who represent a tiny share of the local housing market that is instead being driving higher and higher by domestic buyers responding to overly generous tax subsidies and far too low borrowing rates that are now adjusting to the inflation realities. Banning foreign ownership of Canadian housing is a black mark against Canada’s international reputation and it’s something I’ve long been ashamed of seeing at provincial and federal levels of government.

Taxes

I’ve written for years that the tax code discourages growth in part by creating discrete jumps in rates of taxation beyond certain thresholds. It’s encouraging to see that one measure in the budget is likely to be to flatten out at least some of this effect. When you penalize companies for crossing growth thresholds by hitting them with higher tax rates you discourage the incentive to pursue that additional contract or adopt further investment. Ottawa deserves high markets for listening to small business for seeking to remove some of this effect although the devil may lie in the details we’ll get.

Still, there has long been significant evidence that productivity challenges are particularly acute across smaller producers in both Canada and the US but that Canada has a bigger weight on these challenges because of the larger relative size of its small business community. We’ll see what other tax measures will be in the Budget.

Umm, There’s a War Going On!

Further, Canada’s economy is a wartime beneficiary of the pain and tragedy in Ukraine through the impact upon the commodities that Canada produces and exports. Various metals, potash, oil, gas and grains have all seen higher prices. Higher prices mean higher tax revenues at least for some time. Spending those amounts on social programs with only a token increase in defence spending that continues to result in Canada shirking its NATO responsibilities seems out of touch with today’s geopolitical landscape to me.

Fiscal Anchors

Stabilizing debt:GDP—given that plans to reduce it are likely to be immaterial—isn’t doing enough in my view. When stimulus continues to get applied and debt:GDP is maintained at elevated levels in good times, then the forecasts based upon years of continued good times are vulnerable to the risk that something goes wrong. When something goes wrong, discrete jumps in the debt:GDP ratio occur off of a starting point that did not pursue fiscal repair when it had a chance to do so. That’s how debt:gdp escalates over time, until it can’t without higher taxes, lower spending and market disruption all of which tends to result in regressive outcomes.

Populist Assaults

As a bank economist I’d be remiss if I didn’t share my thoughts on the proposed additional tax levy against banks. I fully agree with our CEO’s take on the matter and not just because he’s the CEO or that I work for a bank! I suppose folks will decide for themselves according to their priors, so I’ll stick with the arguments.

It’s bad economics. Full stop. It’s left wing populism at it’s worst. First, banks already pay umpteen billions in taxes measured in the teens per year. Second, banks make up about 22% of the TSX so when you buy Canadian stocks you’ll pay the tax in the form of lower after-tax returns for your retirement savings for the majority of Canadians who own bank shares. Third, banks are driven by living breathing people who are customers, investors, employees, suppliers and shareholders. Tax incidence 101 says that higher taxes get paid by some combination of this grouping. It’s easier for Ottawa to beat on banks than to be direct in raising taxes on these various groups of individuals. It’s also in keeping with what I have long found to be the disturbing tendency in Canada to push down successful sectors like banking and energy and make folks who proudly work in those sectors feel targeted in negative ways versus championing important sources of prosperity. That approach doesn’t hold water with the full emphasis upon carving up and redistributing the pie toward political aims. It also sends a signal to international markets that Ottawa has an underlying policy bias that is unfriendly toward some of the country’s most successful and economically important sectors.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.