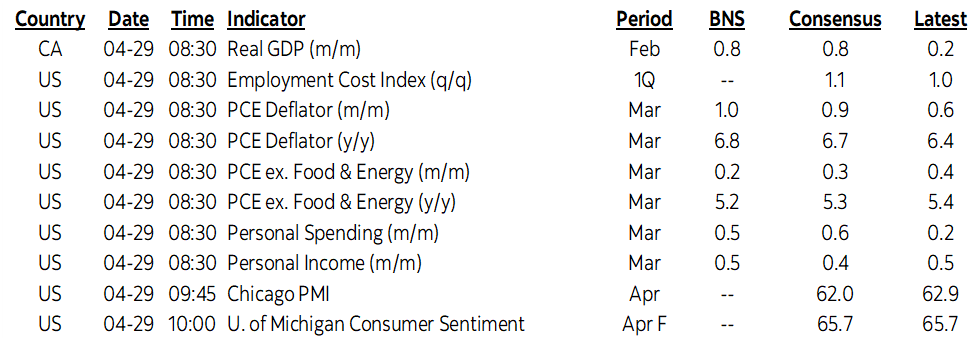

ON DECK FOR FRIDAY, APRIL 29

KEY POINTS:

- Cheap talk drives risk-on sentiment

- China needs action to follow through on stimulus talk…

- …as it doubles down on Covid Zero and support for Russian aggression…

- …that won’t win friends in its key export markets

- Yields up as eurozone core inflation rises more than expected

- Canada’s economy is outpacing the rest

- Eurozone economy squeaked out a mild gain in Q1

- US ECI, PCE, incomes and spending on tap

- Mexico’s economy rebounds by a little less than expected

- Russia’s central bank rate cuts will be like pushing on a string

- BanRep expected to hike 100bps

Talk may be cheap and actions speak louder than words, but so far talk is working at least from the standpoint of short-run market effects. China’s leaders jawboned policy stimulus again overnight with what seem to me like empty words. That combined with signalling that it is easing up on its regulatory assault on internet and tech activity was enough to drive mainland and HK stocks up by 2½% to 4% with spillover effects into western markets this morning. In order to sustain these gains, China’s going to have to follow through with something more than just hot air especially given the doubling down in their comments this morning on Covid Zero and inflammatory rhetoric about its support for Russia that won’t make any friends across China’s key export markets. Some of this unusual mid-day jawboning may have been to prepare everyone for tonight’s PMIs that are widely expected to crater.

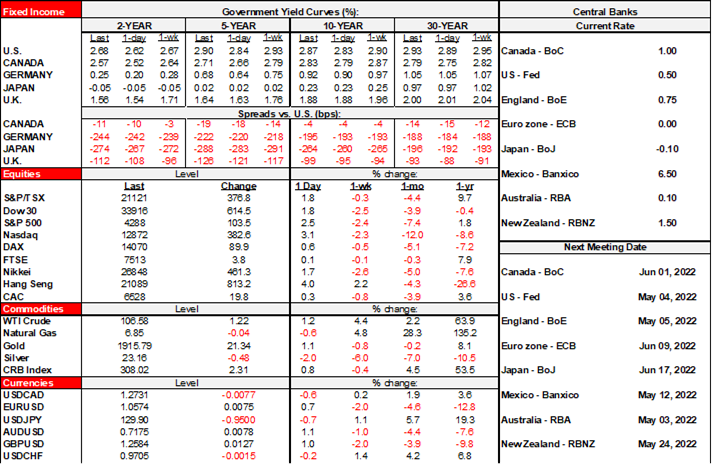

And so into the N.A. open we have the USD dollar on the run as all major currencies are gaining on it. Oil is up by $1–2 on the China effect. Sovereign bonds are cheaper with US yields up by 4–6bps but less at the long end, EGBs cheaper by 3–5bps with a little more in Italy but with the gilts curve little changed. The fly in the ointment is that US and Canadian equity futures are negative with the snp down ¾% and the TSX a touch softer perhaps given the rally across N.A. equities yesterday and the mixed after-market earnings.

Eurozone CPI inflation held steady at 7.5% y/y as expected but core inflation edged up by more than expected to 3.5% y/y (3.2% consensus, 2.9% prior).

Eurozone GDP growth met expectations at 0.2% q/q SA non-annualized in Q1. Germany met expectations with a 0.2% rise. France was unexpectedly flat (0% q/q, consensus 0.3%). Spain’s growth was half of expectations at 0.3%. Italy contracted by 0.2% as expected.

On tap for today will be the following.

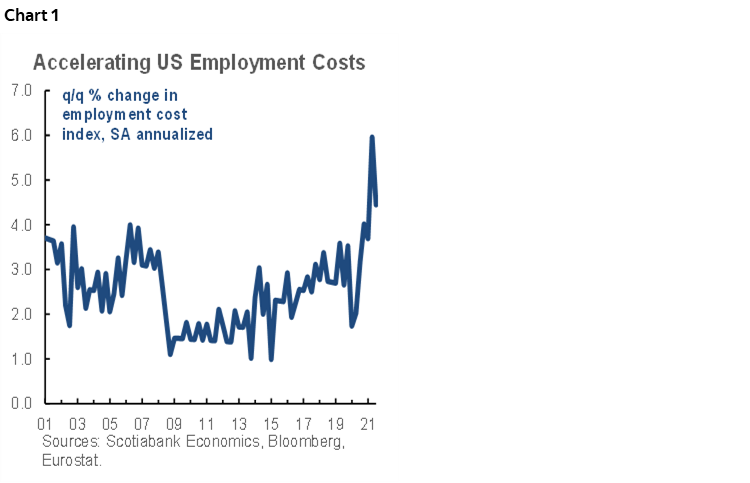

1. US macro releases (8:30amET): Key will be PCE inflation that should broadly follow the earlier CPI release in terms of a strong rise in headline and modest gain in core (March data, unlike the EZ’s April releases). Watch the employment cost index as well (chart 1) as it is expected to jump by another ~1% q/q in Q1 and recall that Powell said late last year that its prior jump to over 1% q/q in Q3 was part of what motivated his pivot on inflation (and then we got another 1% in Q4). Nominal income gains should be solid but decline in real terms. After yesterday’s Q1 GDP accounts, either March real consumption was down a fair bit (like -0.6–0.7% m/m) or there were revisions to the composition within the quarter, or both.

2. Canadian GDP (8:30amET): February was already guided to be a strong month (+0.8% m/m) but advance guidance for March will be more important. The solid rise in hours worked during March should be a good sign along with gains in retail sales and manufacturing shipment volumes. Canada seems to be bucking some of the weakness elsewhere not only in Q1 but also in terms of how the quarter’s math is handing off to Q1. The simple regression equation that I run spits out 0.8% m/m for February followed by 0.4% in March. That would bake-in 2.1% q/q annualized growth in Q2 before we get any data after Q1 growth that my equation suggests would be about 4½%. Canada’s economy is benefitting from a positive terms of trade shock that began before the war and got an added kick from it.

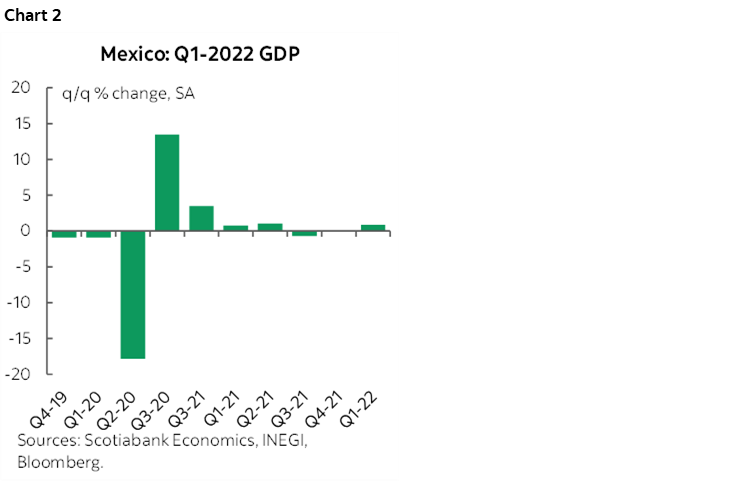

3. Mexican GDP: The economy advanced by a little less than expected in Q1 (0.9% q/q, 1.1 % consensus). Still, that’s a nice bounce back from no growth the prior quarter and contraction before that (chart 2). Mexico (and Canada) were among the beneficiaries of the US import surge over Q1, as well as higher oil prices.

4. Central banks: Russian currency manipulation through capital controls gives its central bank room to ease and it cut by 300bps this morning (200bps consensus). Not allowing the ruble to act as a shock absorber combined with the likely coming western oil embargo will probably mean that rate cuts will be like pushing on a string. BanRep is expected to hike by 100bps to counter escalating inflation (2pmET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.