ON DECK FOR WEDNESDAY, APRIL 20

KEY POINTS:

- Signs of relief across asset classes

- French leaders’ debate this afternoon

- Canadian CPI set to rise again

- China’s banks leave LPRs unchanged as expected

- BoJ’s unlimited buying pledge shaken off by JGBs

- A positive macro spin on Netflix’s results

- Headline risk ahead of late week G20 FinMin/CB meeting

- More Fed-speak

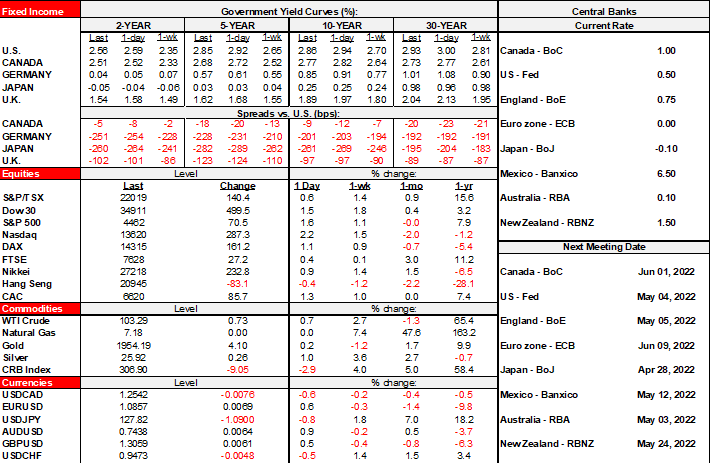

There are a few signs of relief spreading across global financial markets this morning. The USD is broadly softer and among the gainers is the yen that for at least one day has halted its slide since early March. Sovereign bonds are richer across N.A. and Europe as 10-year yields drop by 5–7bps in the US, UK and across the Eurozone. Front-end yields are also generally richer, but mostly in the US and UK. Stocks are mixed with N.A. futures little changed but European cash markets up by between 0.4% (London) and over 1% elsewhere. Some of that is a European catch-up to the accelerated gains in the US after Europe shut yesterday afternoon.

The day’s main market event—at least in Europe—may be the French leaders’ debate at 3pmET ahead of Sunday’s final run-off between President Macron and Marine Le Pen. The main issue of global consequence concerns European unity versus the divisions and softened stance toward Putin that Le Pen would sow if she wins. Rather suspect Macron will go after her on Putin ties including her party’s financing…

There were few notable developments overnight after yesterday’s dull session that only offered up IMF updates to its six-month old forecasts that were last done in October. Not surprisingly, when you only bother to forecast once every six months—by committee at that—you’re going to have pretty big revisions!

China left its 1-year and 5-year Loan Prime Rates unchanged at 3.7% and 4.6% as expected. A cut had been expected before the PBOC unexpectedly left its 1-year Medium-Term Lending Facility Rate unchanged last week. When it didn’t, consensus became stale and cuts to the LPRs were largely out of the question.

The BoJ pledged to buy an unlimited amount of JGBs to enforce its 0.25% ceiling for the 0% 10 year yield target, but the intensified yield curve control efforts failed to influence the 10 year yield that held right below 0.25%. The signal is also that the BoJ isn’t terribly fussed by yen weakness to date.

Watch for any headline risks as G20 FinMins and CB heads arrive in Washington ahead of the meetings on Thursday and Friday. If Russia attends—as seems likely with Putin’s oil-cycling henchman FinMin Siluanov confirming his participation—then the US has said they will boycott the meeting which means western Europeans will argue with Russia and amongst themselves while China, India and Brazil stare at the floor or sleep. The war, covid, the yen’s plummet etc make for a variety of potential tape bombs.

The economist’s positive spin on Netflix’s earnings disappointment is that perhaps everyone is finding something else to do these days! Enter the great post-pandemic rotation toward rediscovering at least some aspects of life pre-2020. Fortunately, Netflix has only about a 0.4% weight in the S&P500 index and so on its own it should be flicked away like a pesky mosquito. Netflix is among many digital services that are raising prices to try and keep revenues afloat as volumes soften. The effects of price hikes on volumes will be important into Q2 as well. The various hiking services include Netflix, Amazon, Disney+, Sirius, Peloton, Crave etc as shown in the chart within the global week ahead.

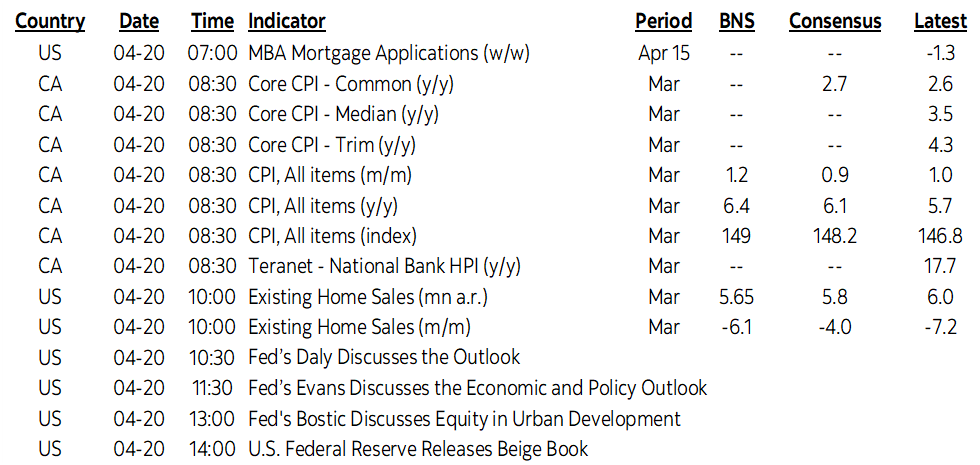

Canada updates CPI which will matter to BoC watchers (8:30amET). My estimate is a bit higher than consensus for this one as I expect 1.2% m/m (consensus 0.9%) and 6.4% y/y (consensus 6.1%). Food and gasoline should see significant hikes in case there’s anyone out there who doesn’t eat or drive. The rotation toward Spring lines and folks returning to offices may have also driven clothing prices higher unless one’s general sensibilities resulted in tossing clothing at the same time as masks! A reopening effect is expected for some higher contact services and housing is expected to be a significant contributor again, although the main housing input only arrives in a separate release at the same time as CPI. See the Global Week Ahead here for further elaborations.

Endless Fed-speak will continue but relief is in sight with the blackout period commencing this Saturday ahead of the May 3rd – 4th FOMC meeting. Daly (10:30amET), Evans (11:30amET) and Bostic (1pmET) will speak ahead of the Fed’s Beige Book (2pmET) that has become of little consequence in the age of constant Fed-speak. Tesla reports in today’s after-market and his Twitter distractions may be further embellished. The only US release will be existing home sales that are likely to slip following softness in pending home sales (10amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.