ON DECK FOR TUESDAY, SEPTEMBER 22

KEY POINTS:

- Equity sentiment mildly improves

- Constructive US macro releases

- Powell’s testimony is unlikely to yield surprises

- BoE’s Bailey pushes back timing on negative rates

- EGBs impacted by seemingly baseless Brexit rumour

- Would Biden really be better for Canada?

INTERNATIONAL

Broad market tone is a little more positive today than yesterday but catalysts for this stability are few and far between. There was nothing by way of material releases out overnight. BoE Governor Bailey jawboned negative rates and said that supporting technical work will take some time which implies no sense of immediacy. That caused the gilts curve to flatten. RBA Deputy Governor Debelle also jawboned options for further action and emphasized additional bond buying across longer maturities, currency intervention but not given where the A$ sits at present, lower rates but without going negative and negative rates despite his assessment that the evidence on their effects is mixed. The A$ broadly shook that off. US macro releases were not first tier market movers, but were generally favourable as Fed Chair Powell and Treasury Secretary Mnuchin begin their testimony. I’ve also addressed some opinions on whether Canada would unambiguously fare better under a Biden presidency; in short, nope, but that’s by no means to be misconstrued as a Canadian endorsement of Trump’s policies toward Canada and other allies!

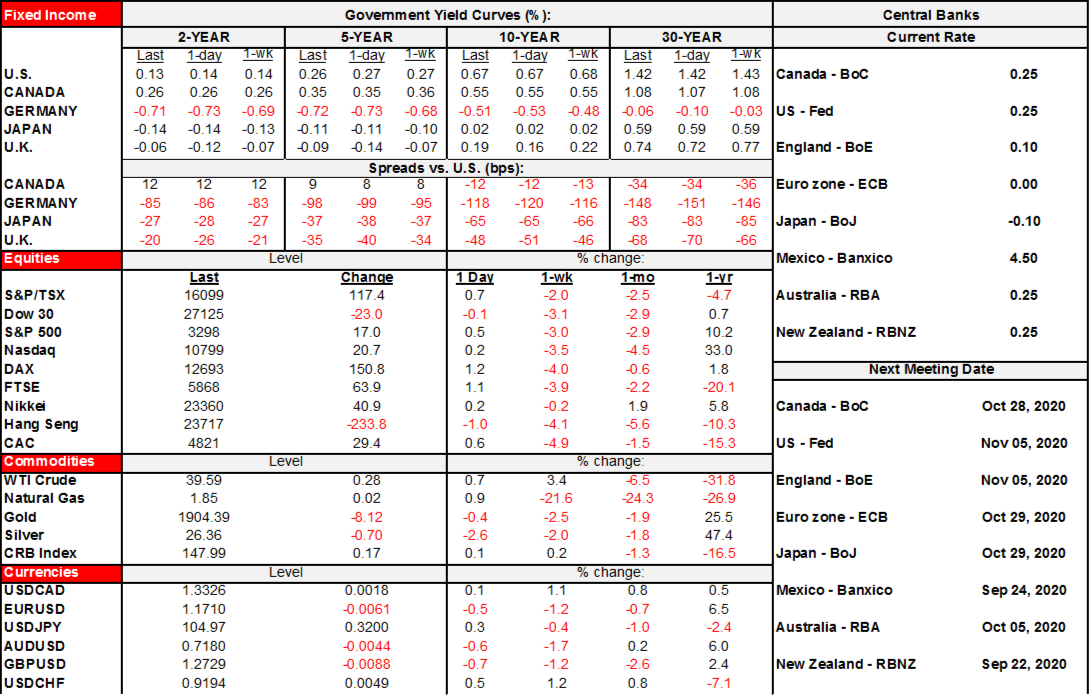

- Stocks are gently higher across North America and Europe. US exchanges are up by approximately ¼% to ½% and the TSX is up by ½%. European exchanges are trading ¼% to almost 1% higher with Germany leading. Overnight Asian exchanges slipped in lagging fashion to the quickened North American sell-off into yesterday’s close.

- Sovereign bonds are generally little changed in North America. Gilts are cheaper by 3–6bps in a bear flattener move as the front-end sells off on reduced negative rate expectations. Italian and peripheral spreads over bunds are materially narrower in part on unconfirmed if not flat out empty media headlines that Brexit negotiations are running a little smoother. I’ll believe that when I see it.

- Oil prices are up by about 1% across Brent and WTI with gold flat.

- The USD is a touch firmer on a DXY basis this morning. It is gaining on most crosses except for CAD that is flat.

UNITED STATES

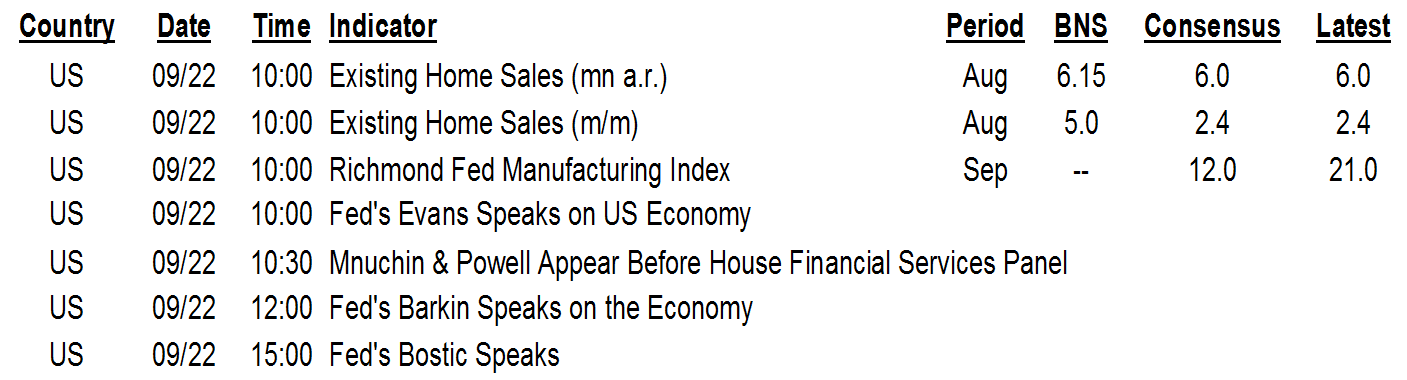

US macro releases were constructive this morning. Existing home sales landed bang on the consensus guess at +2.4% m/m in August (+24.7% prior) and in keeping with the momentum shown in pending home sales. The Richmond Fed’s manufacturing index increased a bit to 21 (18 prior, 12 thin consensus) and the gain was driven by a jump in new orders (27 from 15) with a faster pace of hiring (23, 17 prior).

Richmond’s gain combines with the strong beat in the Empire gauge (17, 3.7 prior) and the little changed Philly Fed metric (15, 17.2 prior).

Fed Chair Powell and US Treasury Secretary Mnuchin are commencing their quarterly CARES Act testimony before the House financial services panel as this publication is being distributed. The written testimony that was released after markets closed yesterday yielded no surprises (here).

CANADA

There are no releases out of Canada today. BoC SDG Wilkins’ media interview is still pending publication and it isn’t known if it is policy- or career-related but there is probably low market risk around it.

Here are a few more contributions to the debate on what the throne speech should strive toward from individuals who are well known to Canadian observers (here, here and here).

As an aside, would Joe Biden be better for Canada? One might be tempted to assume as much after years of damaging insults and protectionist salvos launched by US President Trump. Nevertheless, while actual policy can morph into something dissimilar from an election platform, it’s not the least bit clear to me that Biden – albeit more polished – would be a better friend to Canada.

- Tax competitiveness: The Biden and Harris campaign pledge to raise taxes on corporations and upper income earners. On first round effects, this could make Canada relatively more tax competitive, or at least less uncompetitive. Canada’s statutory corporate tax rate is higher than the US, but the marginal effective tax rate on capital which focuses upon taxation on new investment is lower in Canada than the US, the G7 average and OECD average. Biden has pledged to raise the statutory corporate tax rate to 28% from 21% and to raise the top marginal income tax rate to 39.6% from 37% (analysis here). On second round effects, however, Canada’s government may see such changes as an opportunity to crowd-in tax room without necessarily harming relative competitiveness. The current Canadian federal government repeatedly emphasizes ‘fairness’ and in an effort to rein in very large deficits may capitalize on tax policy changes in the US by raising taxes in Canada. The other second round effect is how equities would take higher rates of taxation on capital gains. You could, however, argue that mammoth deficits could require a Trump administration to ultimately contemplate tightened fiscal policy one day and that higher taxes could be on docket regardless of who wins in November.

- Keystone: Biden has said he would rescind the permit for the Keystone XL pipeline. This may just be election hype that could change, given that the horse has already left the barn with parts of the full length already operational and the rest already under construction, given that modern pipeline technology is safer than alternative modes of transporting oil and given that it’s hard to see how the world would be made a better place if more oil was produced by Putin, MBS and Maduro instead of Canada. Nevertheless, the 830,000 barrels per day that would be transported from Hardisty, Alberta straight to the US Gulf coast would help to alleviate discounts driven by bottlenecks at existing distribution points and give a boost to Canadian exports and particularly Alberta’s struggling economy. Thwart its progress and more trains and trucks may be rumbling through Canada’s and America’s backyards.

- NAFTA: Thank heavens the NAFTA 2.0/CUSMA/USMCA deal did not include sunset clauses that would not have served any of the three countries well and was generally little changed from NAFTA 1.0 in terms of broad substantive matters. But that doesn’t mean trade disputes between the countries would go away in a Biden presidency. Sector-specific disputes that have already dragged on over the years under both Republican and Democratic Presidents (e.g. softwood) could be very likely to continue to do so under a Biden administration.

- Global trade policy: I still find this piece to be a useful breakdown of where Biden would be better than Trump on global trade policy, the same, worse, and what we don’t know. Further, Biden (and previously Obama) have subscribed to their own versions of made in America policies. On net, the tactics and delivery may be very different, but it’s not the least bit clear that Biden is a globalist.

- Carbon taxes: This could be a key one for Canada both directly and indirectly. Biden has pledged to introduce a carbon tariff against countries the US deems to be failing to pursue policies that are favourable to the environment. Most trading partners would likely view this as one part hypocritical, one part arbitrary and one part just another tariff by any other name and could therefore retaliate with their own tariffs. If used as a protectionist tool—or not—then it could further inflame global trade tensions while creating multiple adverse incentives and distortions to world trade. The direct effects on Canada—if directly targeted—and the indirect effects on world trade, growth and commodity prices could be damaging in part depending upon how they may be implemented and how America’s trade partners take it. On the latter count, it’s likely exceptionally naïve to assume that trade partners will oblige the claimed quest for a cleaner planet and submissively roll over.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.