ON DECK FOR FRIDAY, SEPTEMBER 11

KEY POINTS:

- Diverging markets face Brexit, US-China tensions

- Is the pandemic narrative wrong about US inflation risk?

- UK’s Johnson to address party following EU ultimatum

- Chinese financing exceeds expectations

- Markets ignore solid UK economy readings

INTERNATIONAL

There is a bit of a divergence between North American asset classes and Europe this morning as Brexit risks and US-China tensions hang in the air. Overnight releases offered little effect ahead of US CPI figures this morning.

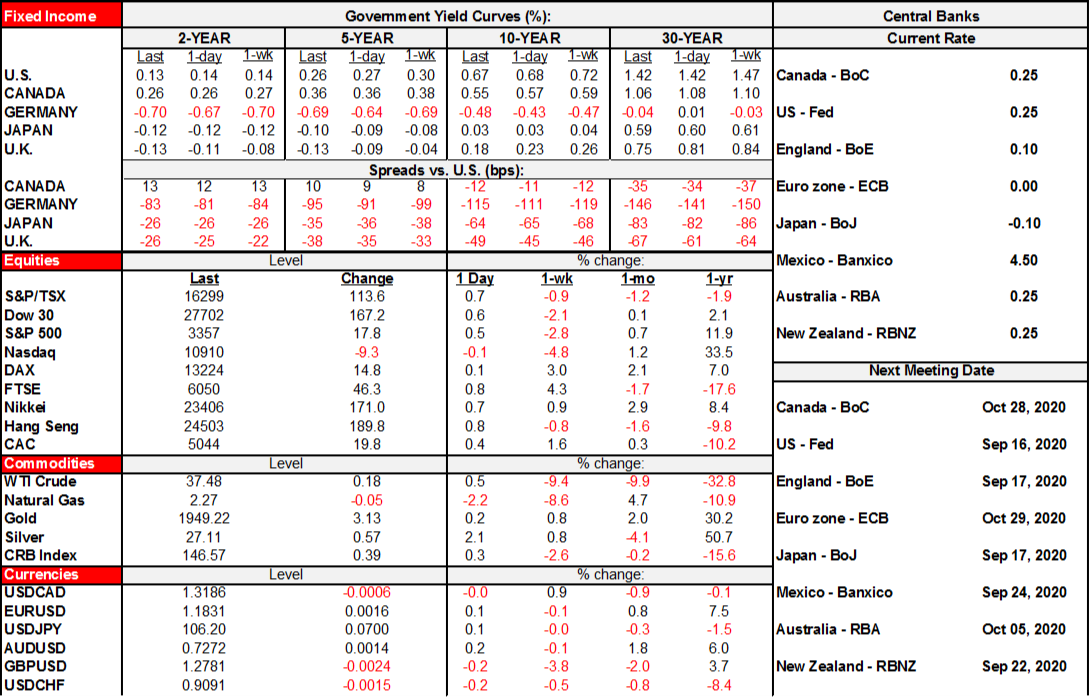

- US equities are up by between ½% (snps) and 1% (DJIA) with the TSX up by just over ½%. European markets are more mixed with the Dax and Milan flat, Paris and London up by ¼% and ½% respectively and Spain down ¾%.

- Sovereign curves are outperforming in Europe. US Treasury yields are generally little changed with a slight bid through the belly. Canada is slightly outperforming Treasuries at the longer end. Yields on gilts are down by 2–6bps in a Boris flattener. EGB curves are performing similarly with yields down 2–5bps in bull flatteners.

- Oil prices are up by 30–60 cents with gold flat.

- The USD is little changed overall but this masks wide deviations across individual crosses. Sterling is leading depreciating majors. Most other major and semi-major and also-rans are higher to the USD with other exceptions being the yen and won.

UK PM Johnson will address his party at 12:30pmET with no deal risk brought forward and amplified by his tactics that are seeking to unilaterally alter the Brexit agreement’s provisions for Ireland that have drawn a stern rebuke from party members at home and from the EU. The EU delivered a month-end ultimatum to back down.

China is taking retaliatory measures against US diplomats on the mainland and in HK following US actions but the exact actions are unclear.

China released financing figures for August that exceeded expectations. 3.58 trillion yuan of aggregate financing was extended (consensus 2.585T) which is the strongest tally since March and more than double the prior month’s flow. Most of the pick-up came through government bonds and yuan denominated loans.

The UK economy registered solid readings in July but markets looked the other way given more pressing Brexit developments. Industrial output was up 5.2% m/m (4.1% consensus) as manufacturing output grew by 6.3% (5% consensus). The monthly services index was up 6.1% (consensus 7.0%). Monthly GDP grew by 6.6% which was in line with expectations. The trade deficit in goods widened as imports were up by 5.8% m/m while exports were up 0.9% while the services surplus shrank.

Spain followed Italy with a stronger bounce in industrial output than Germany or France during July. Output was up 9.3% m/m which nearly tripled consensus expectations for the third strong monthly gain.

UNITED STATES

It’s probably premature to have great confidence in this, but has inflation risk been fundamentally misjudged by global central banks? Or is there a further and bigger disinflationary shoe to drop still lurking ahead? Markets are not so much caring about this debate today as other headlines dominate in driving rallies across sovereign debt markets. Nevertheless, this morning’s US CPI figures add further reason to question the whole narrative that the pandemic is a deflationary or at least sharply and sustainably disinflationary shock. It also gives pause for strategists and traders to continue to re-evaluate the deflation trade they drove in the early stages of the pandemic.

Core CPI landed on my guesstimates at a little above consensus expectations which matters to no one, but hey, take it where you can in this biz. Core CPI inflation has picked up by half a percentage point in just two months in year-ago terms (chart 1). The month-ago seasonally adjusted rise was strong as reopening effects and stimulus combined to result in greater pricing power. Three months of decline in seasonally adjusted core inflation in month-ago terms has since given way to three months of gains averaging 0.4% per month. Annualized, that means core inflation is running at about a 5% clip over this three month trend period.

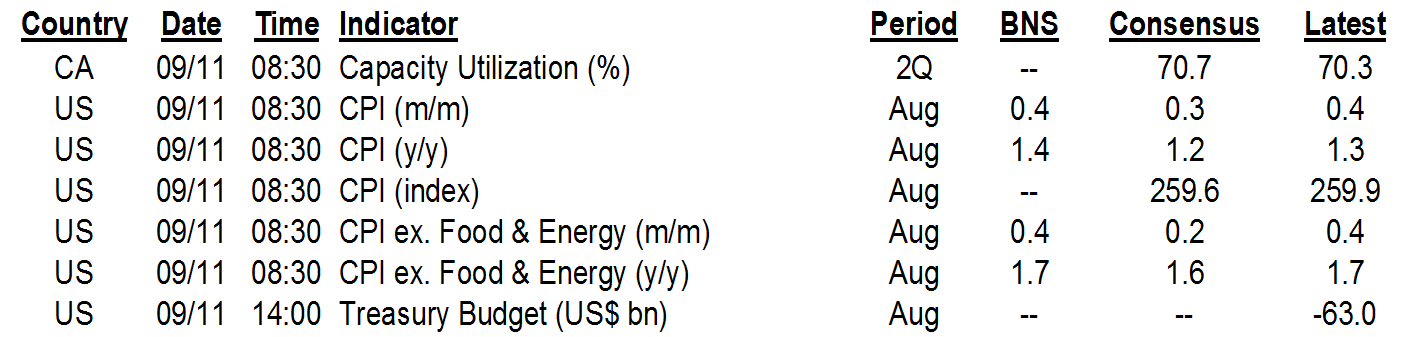

US CPI m/m % / y/y %, August :

Actual: 0.4 / 1.3

Scotia: 0.4 / 1.4

Consensus: 0.3 / 1.2

Prior: 0.6 / 1.0

US core CPI m/m % / y/y %, August :

Actual: 0.4 / 1.7

Scotia: 0.4 / 1.7

Consensus: 0.2 / 1.6

Prior: 0.6 / 1.6

The CPI figures still suggest that core PCE inflation is likely around 1.4% y/y and well below the Fed’s target. Even that, however, takes us up from 0.9% y/y in April to around 1.4% in August pending the PCE figures on October 1st.

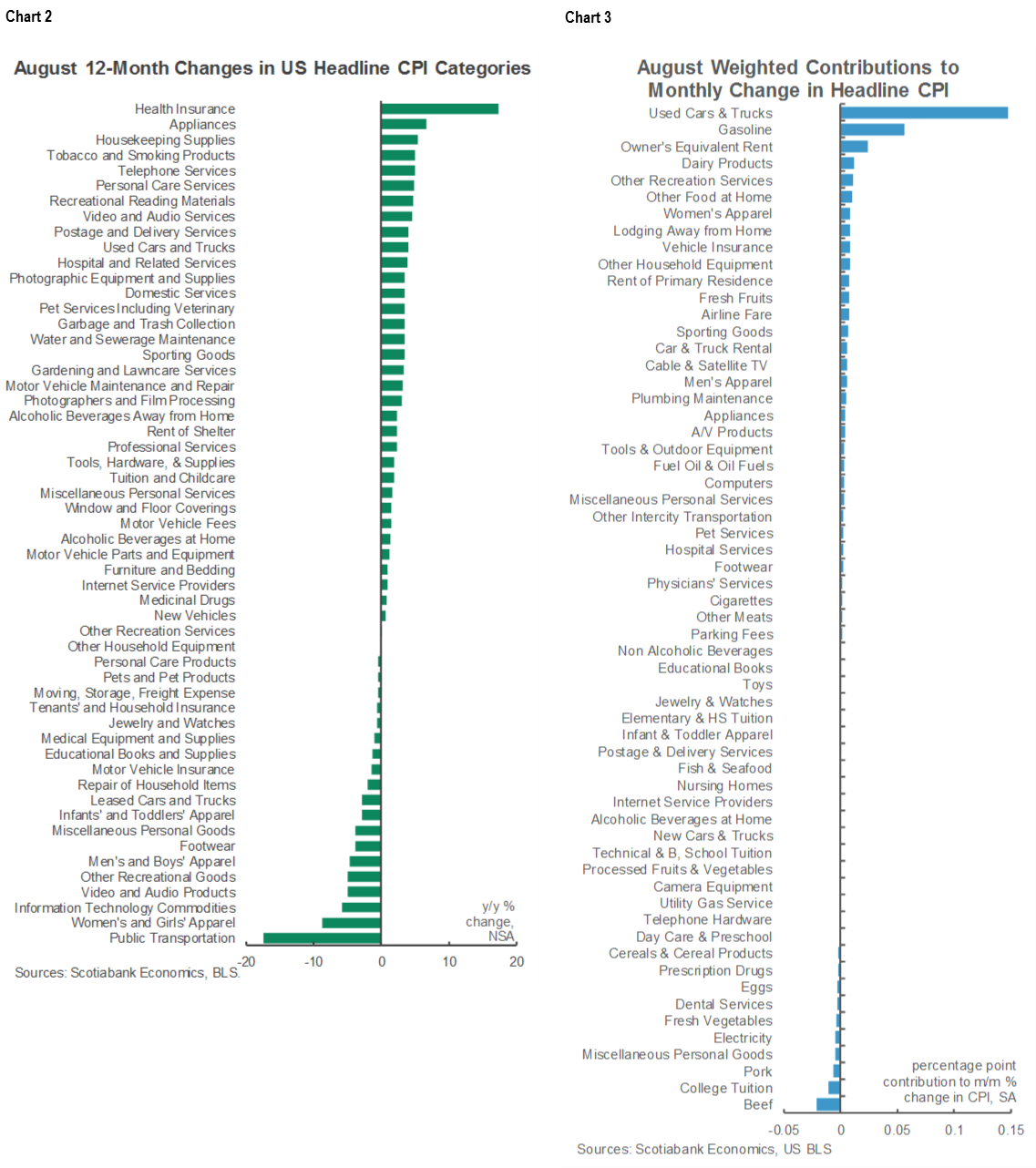

The year over year drivers of CPI inflation are shown in chart 2 in terms of weighted contributions by source. The month-ago seasonally adjusted drivers are shown in chart 3, again in terms of weighted contributions.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.