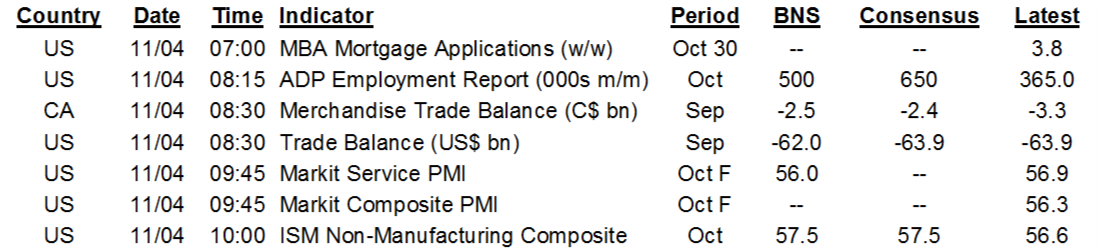

ON DECK FOR WEDNESDAY, NOVEMBER 4

KEY POINTS:

- Treasuries and stocks are both rallying post-election…

- …but discount all market reactions at this premature point

- No winners yet in the US election…

- ...but morning momentum may be leaning toward Biden...

- …and today will tell us whether the stragglers will even matter

- The state of play in the key remaining states

- US ADP strongly points to downside risk to nonfarm payrolls

- US ISM-services cools, but a composite PMI is likely stable

INTERNATIONAL

Like everyone else, we’re in watching and waiting mode in terms of the US election results. At present, no winner has been declared in the Presidential contest. Both sides are saying they see pathways to victory. Biden is winning the popular vote thus far, but the Electoral College vote remains in flux. Trump and the GOP have put in a much better performance than another apparent poll failure had been indicating, but you tell me if that’s because closet Trump supporters lied to pollsters, simply changed their minds on election day, simply got out more than the Dems did on election day, or poll methodologies blew it again. All are possibilities in my opinion. Whether the results are vindication for the GOP or a signal to the Dems—Sanders, AOC and Warren in particular—that too many of them are simply too far left for many Americans and for Biden to be able to control will be forever debated. With AOC calling herself a socialist she may as well have written Trump’s rally rants for him. The Senate stands at 46 seats for the Dems and 47 for the GOP and it is unclear who may take 51. The Dems retained the House which is presently tracking 180–171. Some newswires have Biden ahead by 224–213 and others are at 238 to 213.

The states where results are still outstanding leave pathways to victory for either Trump or Biden, albeit with a slim evolving margin very tentatively favouring Biden in my view. Vote tallies will continue today through to the end of the week at a minimum. Toward the end of the day, however, we should have a stronger sense of whether the stragglers where results might not be known until tomorrow or Friday or possibly later will actually matter or not. I’ve highlighted the current status of the uncertainties in the key remaining states below. The risk of a contested outcome is material after Trump did what most expected by prematurely claiming victory and saying that vote counting should stop as mail-ins continue to be counted. So is the risk that either candidate who wins the Oval office may be neutralized by the other party taking the Senate, but at this point, any combination for the Presidency and the Senate remains viable. Other developments are irrelevant this morning as markets looked the other way after US ADP private payrolls disappointed the consensus guess with ISM-services on tap.

In my opinion, it’s very premature to read too much into market reactions as all outcomes remain in play and markets are prone to initially overshoot and undershoot as the flow of information changes. At a minimum, however, the odds of a convincing ‘blue wave’ are sharply lower so adjusting current pricing for this makes sense but is being applied inconsistently across asset classes. Maybe stocks like lower discount rates and were looking ahead to a momentum shift as mail-in ballots get counted as the offset to the risk of lowered fiscal policy stimulus odds, but again, I wouldn’t spend much time fussing over the current state of markets that could easily swing in either direction as further information is digested. If, for example, it turns out that Biden wins and the Dems ultimately take the Senate then violent steepeners could come back into play.

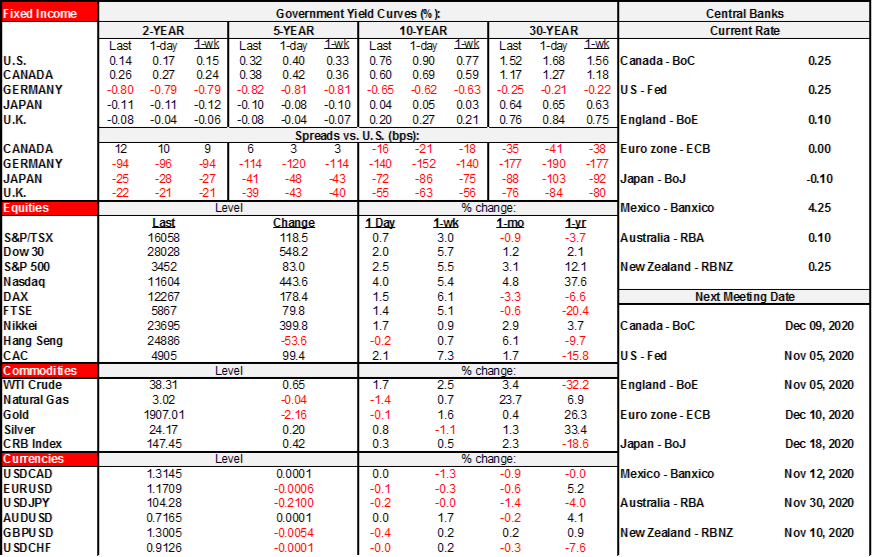

- The US Treasury curve is strongly bull flattening so far with 10s down 14bps and 30s -15bps. Canada’s curve is underperforming but also strongly bull flattening with 10s down 9bps. Ditto for gilts, while EGB 10s are only richer by about 2–4bps.

- That bull flattening might be helping equities with S&P500 futures up by about 2¾%. TSX futures are up by just under ¾%. European indices are up by 1½–2% almost everywhere.

- Oil prices are up by about 2%. Gold is flat.

- The USD is flat on balance as the yen, Euro and Mexican peso are little changed, but sterling and the A$/NZ$ and CAD are slightly depreciating.

UNITED STATES

Here’s a run down of where things stand in the key remaining half dozen or so states for the Presidential vote. Nothing is clear on net. Both Trump and Biden have pathways to victory. Momentum may be shifting toward Biden but it’s extremely tentative. Of the half dozen, at least a couple of states might not have results until tomorrow/Friday but we should have a clearer sense of whether that will matter in the hours ahead today.

- Michigan: 16 electoral college votes are at stake. The current vote margin is 49.4% to 49.1% for Biden. Momentum has swung in Biden’s favour this morning. There are still huge numbers of absentee and mail-in votes to be counted and the remaining votes may be in strongholds for the Democrats. We should have unofficial complete results by the end of today.

- Wisconsin: 10 votes. 3% of the vote remains to be counted. Biden up 49.6% to 48.9% with vote counting continuing. The momentum bias is toward Biden if mail-in votes continue to lean toward the Dems.

- Georgia: 16 votes. Trump is up 50.5% to 48.3% with 94% reporting. But the 8% of remaining votes to be counted are in Dem strongholds around Atlanta.

- Pennsylvania: 20 votes. 25% of vote to be counted and there is a three day grace period for mail-in ballots to be received and counted. Trump has a large lead at 54.1%–44.8% but a lot of absentee and mail-in votes still have to be counted in Democratic strongholds within the state. Guidance from local officials is that “If everything keeps up, we’ll have the total results in the next couple of days.”

- Nevada: 6 votes. Voting on hold, will resume tomorrow. Biden presently up 49.2% to 48.6%. 67% of the vote counted.

- Arizona: 11 votes. Biden up 51% to 47.6%. Vote counting is on hold.

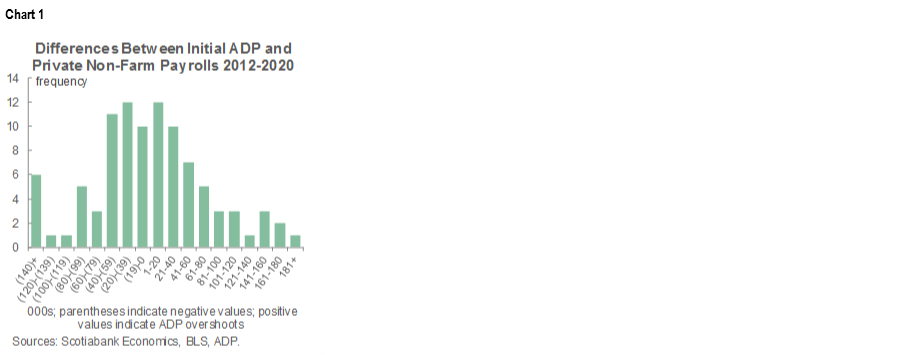

ADP private payrolls landed at 365k in October (643k consensus, Scotia 500k) and the prior month’s revision was small from 749k up to 753k. This implies high odds that the consensus estimate of 700k is far too high for private nonfarm payrolls on Friday. Chart 1 shows the rarity of such a large difference between initial ADP and initial nonfarm estimates.

ISM-services also disappointed for the month of October. It fell by 1.2 points to 56.6 (consensus 57.5) due to weaker new orders (58.8, prior 61.5) and employment (50.1, 55.4 prior) subgauges. The cooler reading likely offers further reason to expect downside risk to nonfarm payrolls in addition to what we learned from ADP. Still, however, after ISM-manufacturing climbed by almost four points, the 1.2 point drop in the more highly weighted ISM-services likely leaves us with little change in a composite PMI.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.