ON DECK FOR FRIDAY, DECEMBER 4

KEY POINTS:

- Risk appetite holding into nonfarm

- ECB rumour mill heats up on PEPP guidance

- Another vaccine entry combines with further Brexit cautions

- US nonfarm payroll indicators lean more toward downside risk

- Canadian jobs face more downside in the next report

- Germany’s factories have almost fully recovered

- RBI stays on hold as inflation ties its hands

INTERNATIONAL

Markets are bracing for US payrolls, considering the ECB rumour mill and digesting vaccine and Brexit headlines. Risk appetite is holding so far. Glaxo announced it is entering into a trial period for its late arrival to the vaccines race. Brexit negotiations are at a “very difficult point” according to a UK spokesperson while German Chancellor Merkel said further compromise is necessary by both the EU and UK.

- US equity futures up by just over ¼% along with Canadian futures. European cash markets are up by as much as just under 1% in London.

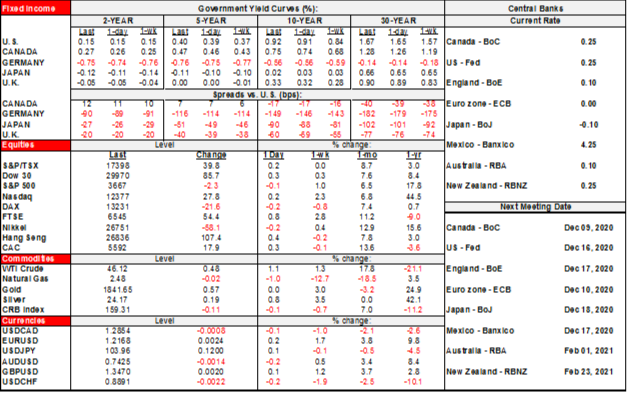

- The US Treasury curve is slightly bear steepening along with Canada's curve and the gilts curve. EGB yields are little changed.

- Oil is up another 1% on the back of the smaller than feared tapering of OPEC+ production cuts.

- The USD is mildly and unevenly depreciating.

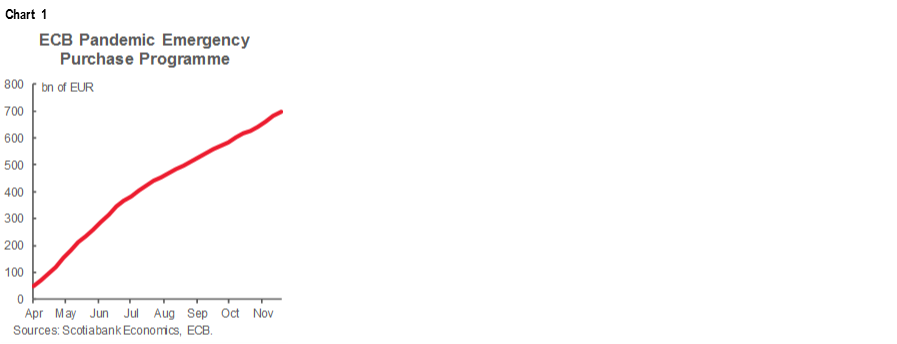

Anonymous officials at the rather leaky ECB are reportedly considering a one-year extension of its existing €1.35 trillion Pandemic Emergency Purchase Programme (PEPP) from “until at least the end of June 2021” to at least one year later. It sounds like garbled guidance to me with some preferring six months and some advocating a conditional withdrawal trigger should things really rip as I think they will. Presumably they might extend reinvestment guidance beyond “at least the end of 2022” if they are buying until mid-2022. Only half of the existing potential size of the PEPP has been utilized thus far and the rate of increase of the assets held within the program has slowed since July compared to prior months. Thus, the ECB might be viewed as saying whatever it wants on the scope of the program but one issue will remain focused upon implementation risk. Underutilized facilities are hardly a rarity across central banks including the Fed and the Bank of Canada as other examples. The euro shrugged at the headline in part because of prior guidance to expect multiple tools to be considered yet the rumour mill didn’t comment on other policy options. I don't think extending purchases by 6–12 months in the PEPP and leaving everything else unchanged would blow anyone's socks off.

German factory orders sailed past expectations but the fact it is October data had few thinking it mattered. Orders were up 2.9% m/m (consensus 1.5%) and they were revised up to a gain of 1.1% in September (0.5% consensus). The order book now stands only a smidge below the pre-pandemic peak in January.

The Reserve Bank of India kept its policy repo rate unchanged at 4% as universally expected in the context of well above-target inflation.

UNITED STATES

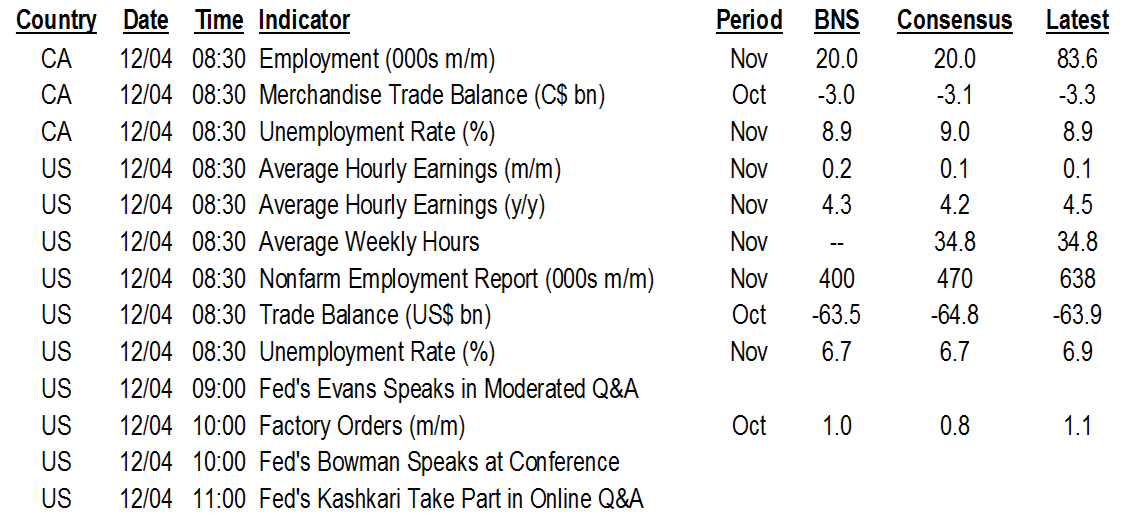

Most pre-nonfarm readings suggest more downside than upside risk. Consensus expects a gain of +475k with Scotia at +400k and the range mostly runs from +300k to +600k with the ‘whisper’ number at 505k. To the downside, claims progress between reference periods slowed (-50k or so). ISM-mfrg employment dipped back into contraction. ADP leans toward downside risk since there have only been about a half dozen times since methodological improvements in 2012 when private nonfarm payrolls have overshot by more than 140k compared to the current expected spread of 233k, although all of them have been in 2020 as ADP has performed especially poorly as a pre-nonfarm indicator this year! Government jobs are expected to fall on state/local firings but also the ongoing unwinding of Census employment since it peaked in August, so quickly look to private payrolls for a cleaner guide. The one upside risk comes from yesterday’s ISM-services employment gauge that modestly increased by 1.4 points to 51.5 and signalled quicker hiring. Nonfarm’s 95% CI is +/-110,000.

CANADA

Canada's jobs report is a dicey call. Consensus sits at +20k which matches my guess that was submitted before knowing consensus. The range runs from -50k to +20k and anything within that range would be the weakest of the recovery to date. Restrictions have tightened across the country, but Ontario waited until the Monday after the reference week to basically shut down Toronto and Peel regions so bigger downside risk might surface in the next jobs report. Further to this point, Ontario is expected to announce an additional tightening of restrictions when the Premier holds a press conference at 1:30pmET. This time it would be ahead of the Labour Force Survey reference week which is the week including the 15th of the month.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.