ON DECK FOR WEDNESDAY, DECEMBER 16

KEY POINTS:

- Risk-on driven by Brexit & US stimulus optimism

- FOMC: Codifying the obvious may be as good as it gets

- Sterling ignores CPI dip, rallies on Brexit talks

- Brexit progress has NAFTA 2.0 similarities

- European PMIs beat expectations

- US retail sales likely indicated a soft start to holiday shopping

- Canadian CPI: is core still sticky?

INTERNATIONAL

Happy Fed Day!

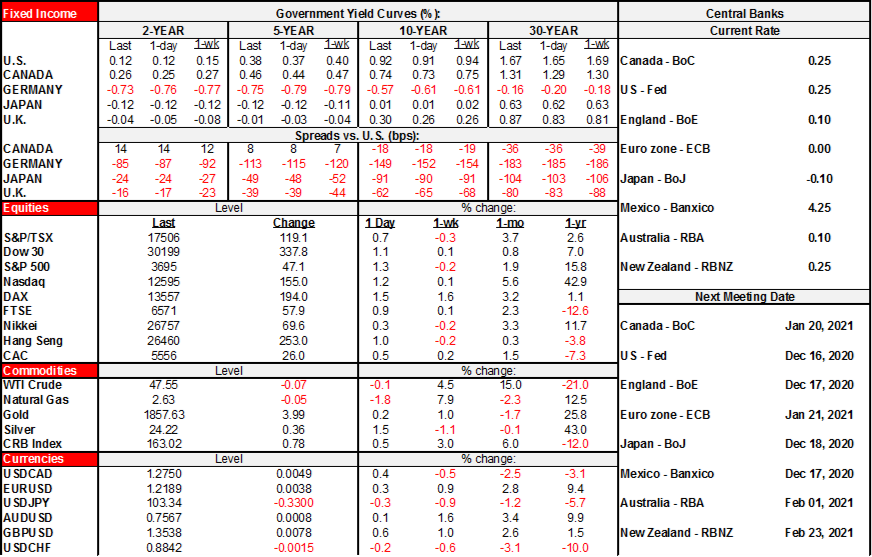

A risk-on bias gets Fed day off to a decent start. Part of the rationale for risk-on is derived from comments late into the evening by US Congressional leaders that reported progress in stimulus and funding talks that are expected to continue today. Another part is derived from bullish comments on Brexit negotiations that seem to have been narrowed down to the single issue of how to handle kippers. Macro data didn’t hurt either.

- US & Canadian stock futures are up by ¼% to ½% or so while European cash markets are up by ½% to just over 1½%.

- Sovereign 10s are 2–4bps higher. Gilts and EGBs are slightly underperforming Treasuries and Canadas.

- Oil is flat. So is gold.

- The USD is slightly softer overall. Sterling is among the biggest gainers on Brexit headlines.

It didn’t hurt that European PMIs were better than expected. The Eurozone composite PMI increased to 49.8 (45.7 consensus, 45.3 prior) indicating that the slip back into contraction in November abated in December. Manufacturing’s expansion accelerated, but the biggest mover was a slower pace of contraction in services.

The UK composite PMI improved by less than guessed to 50.7 and hence back into expansion above 50 (49.0 prior) as manufacturing accelerated (57.3, 55.6 prior) and services shifted to the boundary between expansion and contraction at 49.9 (47.6 prior).

As charts 1–4 indicate, the overall takeaway from global PMIs overnight is that Australia’s economy faces rising upside risk as Q4 closes and enters Q1, while Japan remains stuck in soft contraction and Europe’s Q4 downside risk into Q1 abated somewhat.

UK inflation fell by more than expected and added to the case for BoE easing. Core CPI unexpectedly fell to 1.1% y/y (1.5% prior, 1.4% consensus). That was lower than 26 of 27 economists anticipated and it maintains a volatile but generally downward ongoing trend that has been in place for three years now. Headline inflation also fell by more than expected to 0.3% y/y (0.6% consensus, 0.7% prior).

Still, sterling shook off CPI and is firmer this morning on Brexit optimism. EC President von der Leyen said that aside from fisheries, “a way forward on most issues” had been found. They’ve made progress on state aid, standards and enforcement which is notable. This feels like the CUSMA/USMCA talks as one by one an issue is getting resolved. Just as the NAFTA 2.0 talks came down to micro issues like dairy, I can’t think they’d be so foolish as to scuttle an agreement without striking compromise on fisheries.

CANADA

Canada freshens up CPI inflation for November at 8:30amET. I’m softer than consensus, but a wildcard involves how missing/incomplete markets are handled given renewed restrictions and lockdowns. Consensus expects 0% m/m and I’m at -0.3% m/m, while consensus sees the year-ago rate at 0.8% y/y and I’m at 0.5%. Recall that Canada’s polling for month-ago CPI is in seasonally unadjusted terms. Drivers of my estimate include a combination of lower gasoline prices, typically weak seasonal pricing in categories such as clothing and how the prior month’s strong gains in select categories may be challenged to repeat. Watch the shelter component as one of the hottest drivers of inflation alongside food prices through ongoing supply chain disruptions.

The bigger issue is whether core CPI remains sticky at around 1.8% y/y or so. That’s much harder to gauge given by definition the full distribution of prices needs to be laid bare to know what to exclude from the basket in deriving a trimmed mean estimate, or what might shift the weighted median point and the methodology around common component. For eight months now we’ve been trending around 1.6–1.8% average core CPI and I can’t see that changing on today’s print such that the operational guide to hitting the 2% headline target is likely to remain close to the target.

UNITED STATES

The FOMC statement will be joined by not only the standard projections and dot plot but also new graphs showing the participants’ assessment of the balance of risks and how it has changed over time plus the full Summary of Economic Projections all at 2pmET. Chair Powell’s press conference will follow 30 minutes later.

Guess what, the Fed’s not going to end bond purchases next quarter and is no longer just buying Treasuries and MBS to repair markets. If that shocks anyone then I guess 2pmET might be surprising. It probably shouldn’t. The FOMC is expected to codify a move away from buying bonds just “to sustain smooth market functioning and help foster accommodative financial conditions” and with a purchase horizon “over coming months” and toward buying until it is closer to achieving its dual mandate goals which implies a longer but uncertain time horizon for purchases. Big whoop. So much ink spent by this little cottage industry of Fed watchers on the blindingly obvious. If they don’t do it in today’s statement then I would expect the press conference to basically say that’s what they’re doing. The minutes have indicated that officials want to move toward beefing up the description of their purchase intentions. Some voting members might dissent if they want more flexibility, as Kaplan and Kashkari did in September when rate guidance was altered.

What the FOMC probably won’t do is to alter the US$80B/month of Treasury and US$40B/month of MBS purchases or the maturity composition of purchases and hence the targeted weighted average maturity.

On guidance, I would expect Chair Powell to sound more upbeat, but cautiously so while emphasizing a long road ahead toward repairing conditions.

A pair of US macro releases will garner some attention before the Fed. US retail sales during November (8:30amET) are expected to be on the soft side of the pandemic path to date. We already know that auto sales fell, while tracking of core sales seems soft. Scotia’s pick is for a 0.2% m/m drop in headline sales with ex-autos up by a comparably small amount.

US Markit PMIs for December then follow up at 9:45amET. Consensus is thin for this one and it’s a less impactful release than ISM. Still, it wouldn’t be surprising to see some downside risk given restriction effects, but then again, that was the concern the last time and it beat.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.