The following article was written by Raymond Wong, VP of Data Operations & Mahek Shah, Senior Research Analyst, National Research Insights at Altus Group.

The Scotiabank Women Initiative® is committed to supporting women in commercial real estate. We have collaborated with organizations like Altus Group to provide resources to women-led businesses, allowing them to scale and grow in a challenging industry. Altus Group, an industry leader, can help you connect data points to provide a clear picture of the marketplace, helping your real estate business pivot on-demand and to make those critical decisions at the right time.

The Canadian commercial real estate market faced a lot of challenges through 2021 but is seeing an uptick in momentum with elevated activity levels across the major asset classes with the exception of hotel assets in Q1 2022. National investment volume was recorded at $ 25.2 billion as of Q1 2022, an 61% rise as compared to Q1 2021. Supply chain issues experienced throughout 2021 have continued to persist, with added pressure attributed to the current geopolitical climate and high commodity pricing. The impacts of these factors on investment activity will continue to become more apparent as the year progresses, however, a notable slowdown in activity is not anticipated. Investor confidence is returning to the market and this is apparent with the rise in investment volume, as well as halted transactions from the second half of 2021 brought to execution.

Resurgence of Office: While compared to the first quarter of 2021, the Q1 2022 national office availability rates have risen slightly (within a percentage), they have stayed steady as compared to Q4 2021. Cities such as Vancouver, Ottawa, and Quebec City are beginning to see a dip in availability rates as compared to Q1 2021. This implies that the revitalization of the office market is rapidly emerging. Leasing activity continues to remain strong, with no big lease cancellations in the first quarter of 2022, and availability rates for new completions in hot markets like Toronto and Vancouver dropping as compared to Q4 2021. Moreover, a lot of the activity in Q1 2022 is reflective of the second half of 2021 with delayed deals brought to completion. This is due to a lag seen once the deals are finalized, as well as a lockdown in the second half of Q4 2021 halting activity. However, the office asset is going through a transformation in the way in which it is used. While people are returning to their offices, the preference for the hybrid work model remains. This is shifting the use of offices from spaces to do all of one’s work in, to a space used primarily for collaboration, and talent retention. As resurgence in the office asset class occurs, office assets will continue to remain sensitive. Despite interest rates rising, activity in the office asset class had momentum in Q1 2022 but the asset class will remain sensitive to volatility. The impact of the rising interest rates, the pandemic, and other macro-economic factors on office assets will become more apparent in the second half of 2022.

Industrial Demand Remains Sky High: The industrial asset class has been an investor favorite over the last year and continues to remain so through the first quarter of 2022. All industrial assets are experiencing pent-up demand and make up three of the top five preferred products throughout 2020 and 2021, as well as the first quarter of 2022 according to Altus Group’s Investment Trends Survey. With supply continually falling short of consumer needs. This is exacerbated by global supply chain bottlenecks, with added pressure from current world events as well as the popularity of e-commerce. Availability rates for the asset class has continued to tighten into the first quarter of 2022, dropping to 2.2% nationally, as compared to the 2.9% seen in the first quarter of 2021. They have dropped across all major markets, with the exception of Montreal, which has remained steady. Moreover, new supply is being absorbed as soon as it is available. This can be seen in Vancouver and Southwestern Ontario. In the first quarter of 2022, Vancouver had 0% availability for its new completions, with Southwestern Ontario sitting at 5.1%. The challenge that the industrial sector will face will not be a slowdown in activity catalyzed by rising interest rates, rather the square footage available as developers chase every parcel of available industrial land for development. This pent-up demand and subsequent rapid absorption of space can be expected to remain throughout 2022 despite the rise in interest rates.

Preference for Multi-family assets: Multi-family assets were reported to be the second most preferred product by investors as of Q1 2022, according to Altus Group’s Investment Trends Survey. This is due to their nature as an essential asset, with potential for redevelopment. As the 2022-year progresses, the demand for multi-family assets is expected to grow, with vacancy and overall capitalization rates decreasing. Overall cap rates for the multi-family asset class were recorded at 4.09% as of Q1 2022, the lowest they have been since Altus Group began its data tracking. This can be attributed to housing unaffordability driving people towards rental housing, especially as the cost of borrowing goes up. Moreover, immigration levels are also rising, leading to higher population growth. As population continues to grow, inflation rises, and interest rates go up, the demand for rental units will grow, driving growth and stable returns, as well as strong investment activity throughout the year.

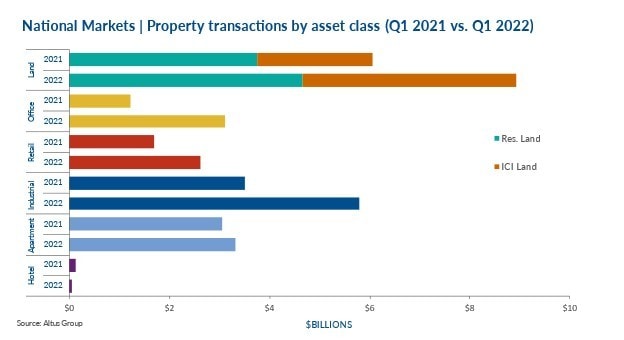

Land sectors continue their upward trajectory: Having grown the most in investment activity from 2020 to 2021, the Residential and ICI land sectors (especially industrial land) have also become an investor favorite. Recording a 27% and 88% increase respectively, from Q1 2021 to Q1 2022, not only are land assets in demand, but land values continue to skyrocket. In the case of industrial land, this is not just due to the rise in e-commerce and supply chain issues, but also to a shortage in the square footage available in prime location. With residential land, an increase in the demand for housing driven by immigration levels is causing prices to rise rapidly, especially in urban locations. As the 2022-year progresses, this trend is expected to continue, with interest rate increases putting a slight damper on residential land prices, and ICI land remaining, for the most part, unaffected.

The 2022 year has kicked off with a lot of activity occurring in the commercial real estate space. Offices are being put back to use, meanwhile the demand for industrial and multifamily assets continues to persist. The land sectors have shown rapid growth over the 2020-2021 years and continue to remain an investor favorite. As interest rates rise, and inflation remains high, it remains to be seen whether the Canadian economy will be subject to recession with a subsequent impact imminent on the commercial real estate industry. The 2022 year has begun on a high note; however, it remains to be seen whether the factors outlined above will allow us to keep up the momentum and surpass the investment volumes seen last year.

About Altus Group

Altus provides the global commercial real estate industry with vital actionable intelligence solutions driven by our de facto standard ARGUS technology, unparalleled asset level data, and market leading expertise. Altus empowers real-estate professionals to make well-informed decisions with greater speed and scale to maximize returns and reduce risk.