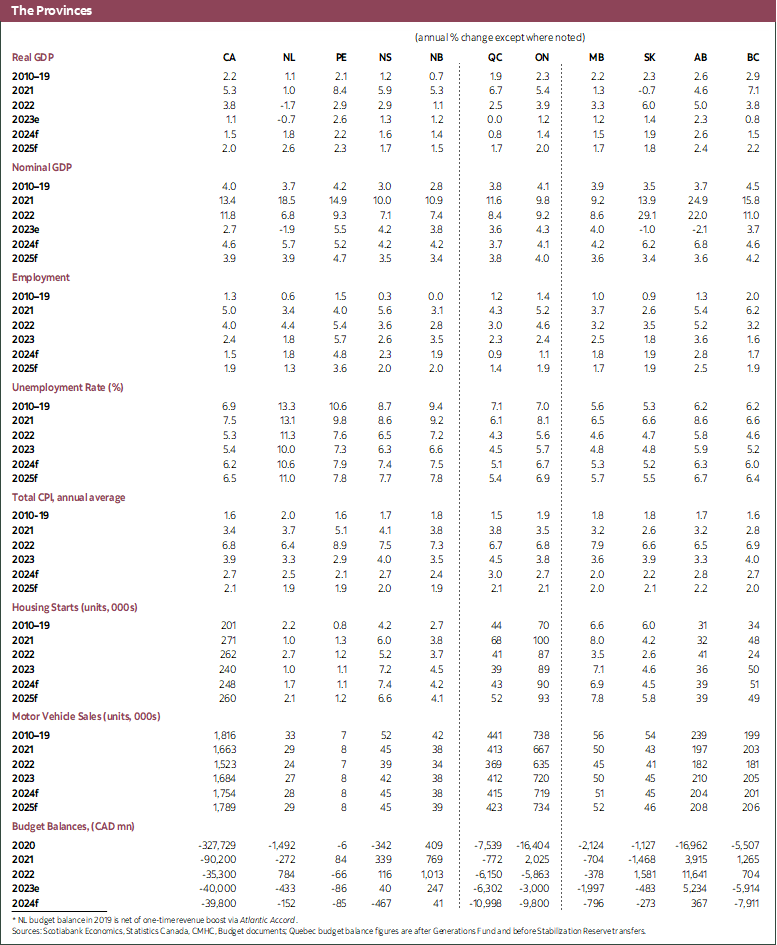

HIGHLIGHTS

We have revised up our 2024 growth projections across the board, reflecting robust momentum observed in the first quarter. The economy is on track for a broad-based rebound in Q1 as sentiment ticks up and fast population influx persists. Strength builds up beyond the first quarter as a stronger commodity outlook and an stimulative fiscal position give growth a lift this year. Overall, real growth is expected to exceed last year’s subdued 1.1%. Despite a better start to the year, economic activity is nevertheless expected to slow in the coming quarters, albeit a shallower downturn than previously anticipated. Provinces continue to weather the restrictive interest rate environment differently, exhibiting varying levels of resilience, while encountering further headwinds such as the cap on international students and the intended reduction of foreign workers.

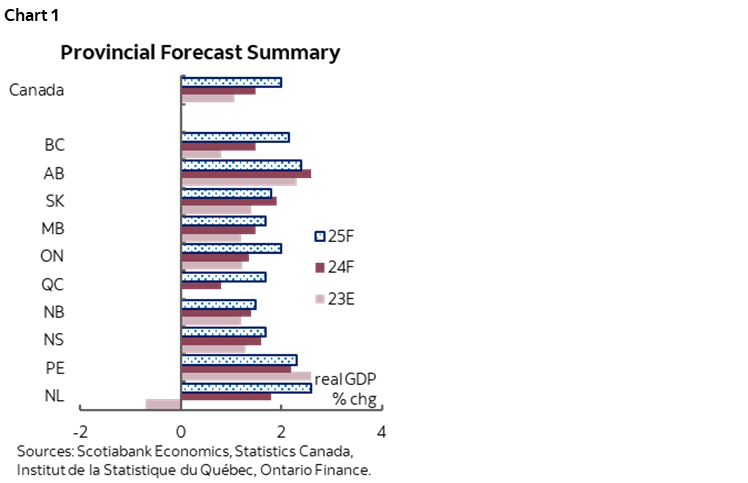

Although all provinces now expect better growth in 2024, not all strength is created equal (chart 1). Strong momentum persists in Alberta and PEI and the two provinces will likely continue to top growth ranking with impressive real growth above 2% in 2024. A more favourable commodity outlook combined with capital investments in major projects should give Saskatchewan and Newfoundland and Labrador a boost. After some notable deceleration and likely meagre growth last year, activities in BC are picking up, supporting a rebound this year. On the other hand, weaknesses in Ontario and Quebec continue to play out but the descent seems to be stabilizing, especially in Quebec as the economy gets past a few disturbances.

BUSINESS INVESTMENTS PULLING BACK, YET SASKATCHEWAN, NOVA SCOTIA, AND ONTARIO BUCK THE TREND

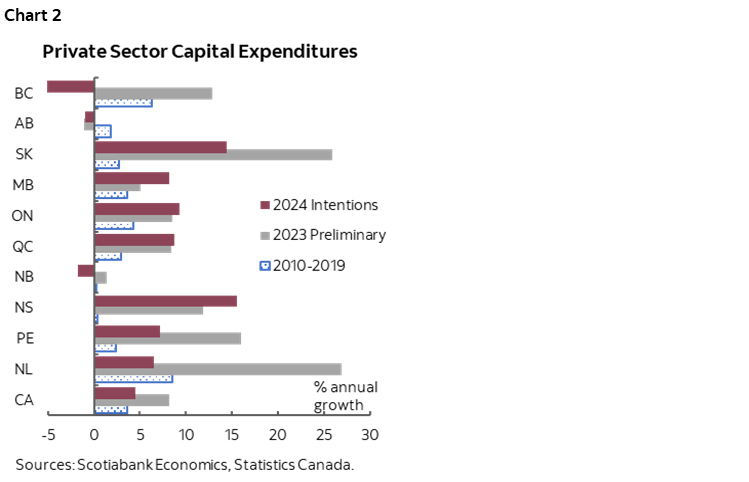

Most provinces are grappling with pullbacks in business investments as a result of restrictive interest rates, yet with upside surprises. Nonresidential capital investment started to contract in real terms over the second half of last year, turning into a drag to growth. The decline concentrated in the Prairie provinces as well as New Brunswick. While the general trend of descent continues into 2024, the year brings pockets of optimism with major investments in industries such as EV batteries and mining. According to 2024 capital expenditure intentions, private investment is expected to boost growth in some provinces, particularly in Saskatchewan and Nova Scotia, while remaining a headwind in BC, Alberta and New Brunswick (chart 2). Public investment is anticipated to receive a significant boost this year, offsetting some weaknesses in private capital investment, notably in Ontario, BC and Saskatchewan, where governments have announced substantial infrastructure spending plans.

GOVERNMENT SPENDING LARGELY SUPPORTS GROWTH, LESS SO IN ONTARIO

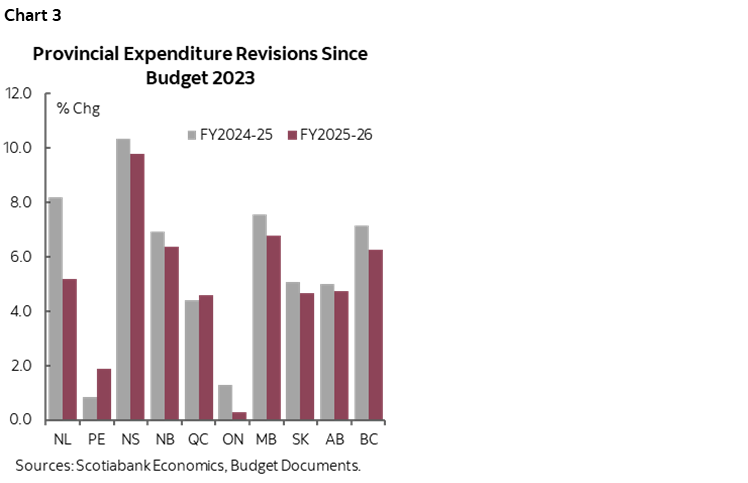

Provinces have largely ramped up spending in the 2024 budget season, boosting growth this year and next (chart 3). The provinces collectively announced $44 bn (1.5% of nominal GDP) in incremental outlays, evenly split over 2024–2025. Revenue windfalls supported by robust economic momentum provide room to lift spending in Nova Scotia, New Brunswick and Alberta, whereas BC and Quebec opted to run larger deficits to fund increased outlays. Ontario stood out as an outlier with the government maintaining a tight grip on spending amidst a downward revision in tax revenues. Most of the increases stem from rising operational costs resulting from public-sector wage negotiations, with the remaining funds directed toward critical priorities such as improving provinces’ healthcare systems. Increased outlays boost growth directly through government consumption of goods and services, and indirectly through increased demand from public sector wage increases.

CONSUMER RESILIENCE PERSISTS IN THE MARITIMES AND ALBERTA

Household consumption continues to be more resilient than expected across the board, buoyed by population growth and a robust labour market. Growth in real household spending remained firm at 1.05% on an annualized basis q/q in the last quarter of 2023 as per capita spending continues its descent at an annualized rate of -2.05%. Household balance sheets appear generally stabilizing heading into 2024, with early data suggesting continued strength in household consumption in the first quarter of 2024. Savings rates remained elevated at 6.2%, well above the pre-pandemic average of around 2%. The household debt service ratio rose to all-time highs in mid-2023 but appeared to be stabilizing in the second half of 2023 due to deleveraging in consumer debt. Regional differences persist into 2024 as suggested by retail sales data, yet relatively minor given the widespread strength. Consumer sector growth stalled first in BC and Ontario following BoC’s rate liftoff and remained muted throughout 2023. Maritime provinces and Alberta continued to see robust growth in retail sales. With a relatively low debt burden and savings rates well above other jurisdictions, Quebec’s consumer sector has displayed incredible resilience compared to the rest of the country but cracks have started to appear as the impact of significant government income support dwindles.

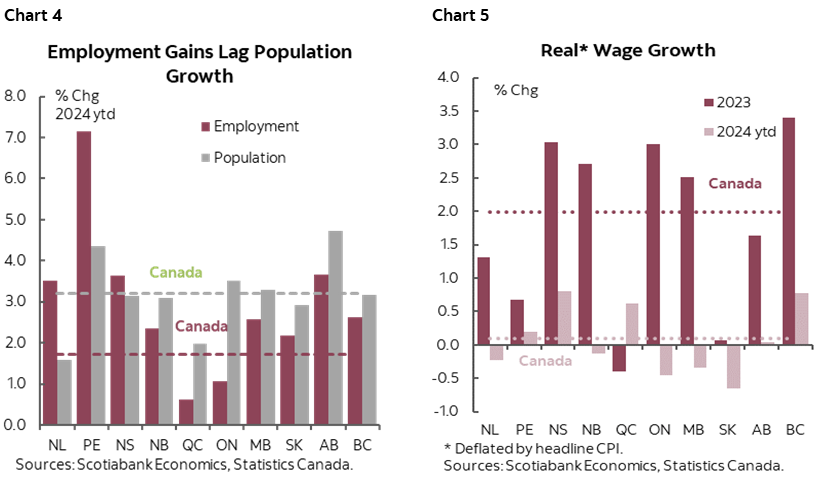

The labour market defies expectations given the stage of the rate-hiking cycle, although signs of cooling emerge, especially evident in Quebec and Ontario (chart 4). Employment gains have consistently lagged behind rapid population growth since early last year, driving up unemployment rates from coast to coast. The Atlantic provinces buck the trend so far with robust job gains outpacing strong population gains, suggesting remarkable economic momentum. We expect unemployment rates to rise further in all jurisdictions as growth slows over the course of this year, but likely to levels just above NAIRU (non-accelerating inflation rate of unemployment). Wage growth remains solid and continues to surpass inflation, leading to real wage gains, particularly in BC and Nova Scotia (chart 5).

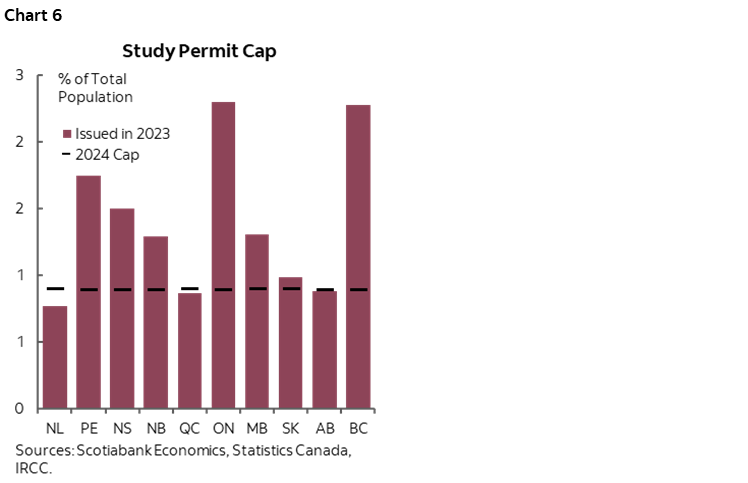

Strong population growth remains a key driver for growth in 2024, yet uncertainties arise from the federal government’s plan to reduce temporary residents. Population growth continued at elevated rates in the first quarter of 2024 amidst the federal government’s announcements regarding its intention to shrink temporary residents' share of the population to under 5%. With study permit issuance capped at 360k in 2024 and allocated by population share, Ontario, BC and the Maritime provinces will bear the brunt of the reduction, while Quebec and Alberta should see relatively minimal impact (chart 6). As a popular destination for migrants both domestically and internationally, Alberta is expected to sustain a high level of population growth. Manitoba and Saskatchewan benefit from strong international migration, but still experience material losses from inter-provincial migration.

COMMODITY EXPORTERS RIDE HIGH ON BRIGHTENING OUTLOOK

Oil prices have risen significantly in recent weeks, providing growth upside for oil-producing provinces. With recent gains, WTI averaged US$78.5/bbl year-to-date with potential for further gains expected due to anticipated supply deficits as OPEC+ continues output cuts into the second half of the year. The anticipated start of operations for the Trans Mountain Expansion (TMX) project in the second quarter is expected to add to growth through narrower light-heavy differentials and increased export capacity. The WCS-WTI differential could drop from historical levels of US$17–$19/bbl to US$13–$15/bbl. Anticipated momentum in energy prices and expanded egress support continued strong activity in the oil and gas sector. Alberta’s Budget 2024 anticipates a 7.4% increase in oil and gas capital investment this year as oil production continues to expand by between 2–3 ppts annually in the next three years. Saskatchewan’s oil production is projected to be flat in 2024 and increase at an average of 1.8% per year over 2025 to 2028. Newfoundland and Labrador anticipate a rapid 12% boost in oil production from last year’s subdued levels as Terra Nova resumes full production.

RATE CUTS POWER A WIDESPREAD REBOUND LATER IN THE YEAR, MORE PRONOUNCED IN ONTARIO AND BC

Given the underlying resilience in the economy, we anticipate fewer and later rate cuts by the Bank of Canada, leading to a rebound led by residential and business investments in the second half of this year and into 2025. Anticipated reductions in borrowing costs are likely to release some pent-up demand across all housing markets, particularly in Ontario and British Columbia, where current sales rates sit well below fundamental levels. These provinces could expect the largest growth in the residential sector next year, accompanied by some erosion of housing affordability.

BRITISH COLUMBIA: GROWTH PERSEVERES AGAINST MOUNTING HEADWINDS

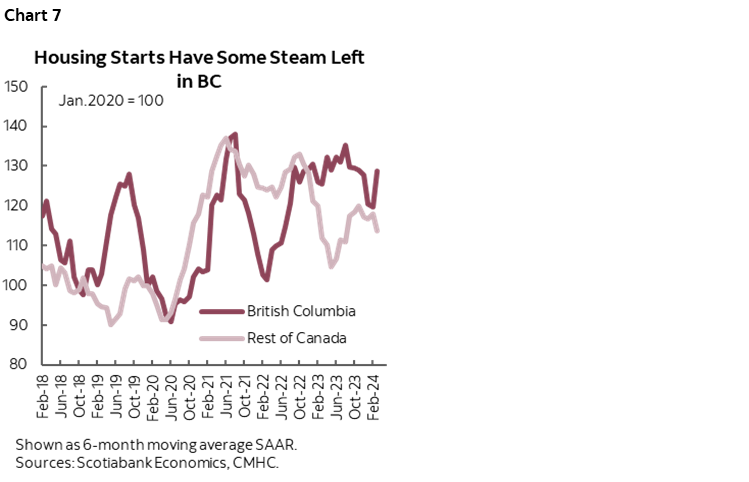

Last year, BC experienced a more pronounced slowdown than the rest of the country against a backdrop of high interest rates and softening export prices. While activities continue to be subdued in some sectors, particularly residential investment, the province anticipates positive developments this year with its well-positioned economy supported by a stimulative fiscal stance. The housing sector performed better than anticipated towards the end of last year, with the momentum carrying into this year, reflecting strong fundamentals and the province’s effort to increase supply. Hiring in BC initially experienced modest declines amid aggressive rate hikes but stabilized in the second half of last year with the province achieving impressive job gains. Exports are expected to rebound with a gradual rise in natural gas prices and an improved outlook in forest products, yet uncertainty and volatility persist in the sector.

Business investment—a driver of growth last year—should be neutral to growth this year. According to the 2024 capital spending intentions, private investment is set to ease following the completion of LNG Canada and Site C dam. Business investment in BC and at the national level should continue to slow as higher borrowing costs weigh on investment spending. There are undoubtedly positive developments as the province unveils significant investments in the EV battery supply chain. Public investment is set to pick up, offsetting some weaknesses in private investment. The government beefed up its capital spending program over the medium term with taxpayer-supported outlays expected to jump by 40% this year, then remain elevated in the next two years, totalling $43.3 bn over the three-year fiscal plan.

In BC’s 2024 Budget, the government announced $13 bn (around 1% of nominal GDP annually) of new spending over the next three years, directed towards addressing a wide array of priorities, including new funding unlocked to improve healthcare. The sizable increases in operating spending should provide BC with a near-term lift.

ALBERTA: PIONEERING GROWTH ON STRONG OIL OUTLOOK

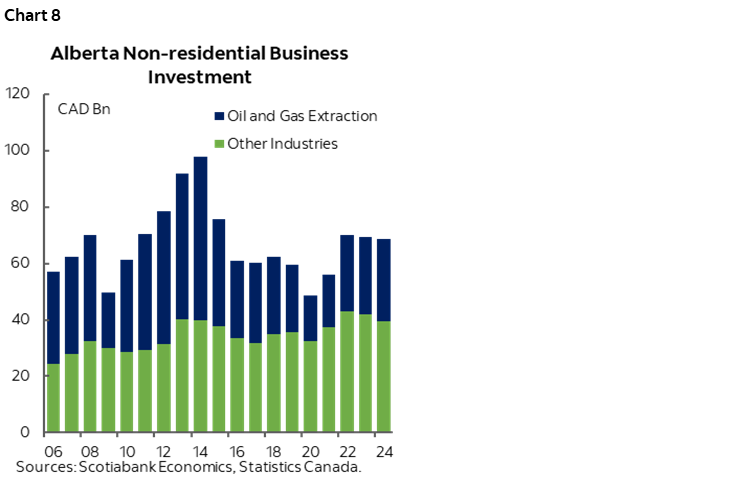

Leading provincial growth once again in 2024, Alberta’s growth outlook should brighten further with surging oil prices amid geopolitical tensions and a supply crunch. Anticipated supply deficits should support crude prices throughout the year, driving continued boosts in oil and gas investment in Alberta. The completion of the Trans Mountain pipeline expansion (TMX) project will boost the province’s takeaway capacity by 590,000 barrels per day and expand market access to Asia and the US West Coast. The WCS-WTI differential could drop from historical levels of US$17–$19/bbl to US$13–$15/bbl in the next two years, supporting sector profitability. Anticipated momentum in energy prices and expanded egress support continued strong activity in the oil and gas sector. Alberta’s Budget 2024 anticipates a 7.4% increase in oil and gas capital investment this year as oil production continues to expand by between 2–3 ppts annually in the next three years.

While capital expenditure intentions in sectors outside oil and gas extraction are down slightly in 2024, Alberta continues to diversify business investment. The province’s 2024 budget paints a rosier picture, projecting an 11% increase in nominal terms in spending outside the oil and gas sector, focusing on large-scale investments in emissions reductions across industries such as power generation, manufacturing and transportation. Further upside could be anticipated with the proposal of several carbon capture and storage (CCS) projects, and more are expected with the announcement of the Alberta Carbon Capture Incentive Program (ACCIP), offering grants of 12% for eligible capital project costs.

The impact of high interest rates and prices continues to weigh on consumer sentiment, yet the region remains relatively insulated compared to its peers, supported by its exceptional population gains. Although retail sales inevitably slowed after a year of impressive growth, underlying fundamentals remain supportive. Household debt in Alberta has seen significant deleveraging since 2019, with the average debt-to-disposable income ratio decreasing from over 200 to 165. The moderation in both mortgage and non-mortgage loans has positioned households well to withstand elevated interest rates and prices. Healthy job gains in the province continue to support future spending, and population growth remains an advantage, with Alberta remaining an attractive destination for both international and interprovincial migrants. The government doubled down on the “Alberta is Calling” campaign by offering a tax credit, targeting skilled labour crucial for diversifying the economy. Moreover, the province is less affected by the potentially reduced inflow of non-permanent residents.

SASKATCHEWAN: INVESTMENT BOOM POWERS GROWTH ACCELERATION

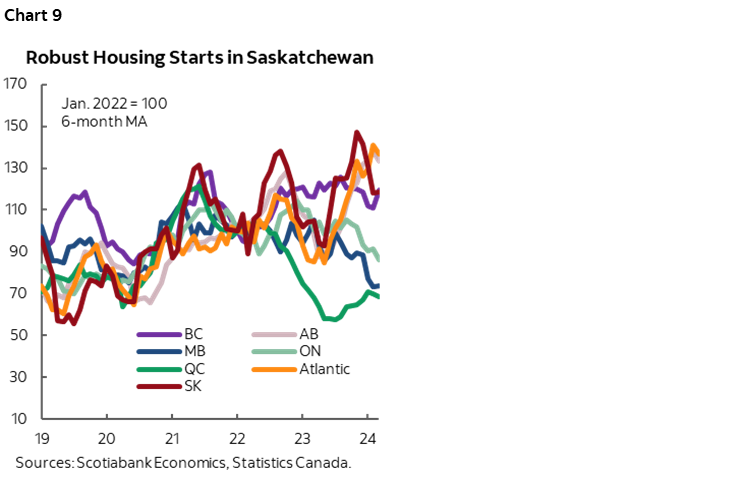

Despite setbacks from adverse weather conditions and weaker commodity prices last year, Saskatchewan’s solid growth path is bolstered by a strong investment outlook this year. Robust commercial and residential construction continued at elevated levels in 2024. Capital outlays are set to increase by $2.5 bn (14.4%) in 2024, with notable increases in mining, quarrying, and oil and gas extraction (+$1.7 bn +22.5%). Thirteen major projects are in the construction phase across key sectors including agriculture, manufacturing, mining, and oil and gas, and BHP’s approval of the $6.4 bn investment in the Jansen Stage 2 project should drive growth prospects over the next few years. Residential construction is also booming, with housing starts sitting at levels above the past two years while most provinces are experiencing a slowdown in building activities. Rapid growth in business investment supports job gains, and hiring has ramped up since late last year.

In the resource sector, a strong oil price outlook and stabilized potash prices indicate a promising year ahead. Favourable oil prices are expected to boost income in the province despite largely flat production levels. The normalization of potash prices from record highs in 2022 following Russia’s invasion of Ukraine seems to have stabilized and remains above historical levels. Although the lingering effect from the substantial price decline still weighs on growth in the sector relative to last year, potash sales should continue to expand steadily given robust global demand.

MANITOBA: STEADY IT GOES

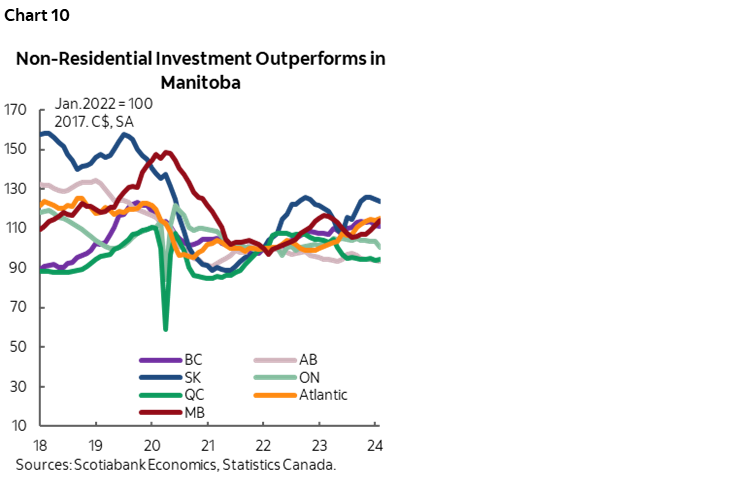

Manitoba’s growth slowed last year in tandem with the national average as restrictive interest rates keep a lid on consumer spending and housing activities. The province continues to weather the ongoing slowdown well, thanks to its resilient economy and well-diversified industries, and we anticipate a middle-of-the-pack performance this year. Drought conditions weighed on several key sectors, which could expect moderate recovery this year assuming normal weather conditions during the growing season. However, prices for key crops remain subdued, pressured by improved global supply, constraining potential upside in the agriculture sector. Hiring remained strong in the province with an impressive 2.6% y/y growth in the first quarter. The province also boasts the lowest price inflation, which should contribute to continued growth in household spending, supported by fiscal measures such as the extension of fuel tax holidays. Nonresidential investment should continue to outperform most provinces, offsetting some weaknesses in the residential sector, and giving Manitoba’s growth prospects some edge.

ONTARIO: GROWTH SUPPORTED BY CAPITAL INVESTMENT WHILE FACING STRONGER HEADWINDS AHEAD

According to quarterly economic account data, Ontario’s economy posted a gain of 1.2% last year, slightly outpacing the national average. Underlying resilience should support continued expansion in the province this year, particularly in business investments, yet growth will likely lag the rest of the country as the province experiences stronger headwinds.

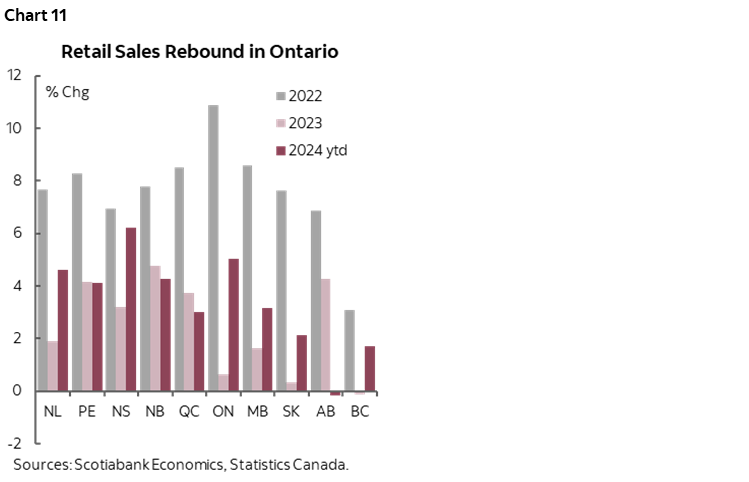

Household consumption held up stronger than expected, contributing to the province’s outperformance last year, yet the outlook remains a mixed bag. Growth in retail sales—which does not capture consumption in services—stalled last year in Ontario as rate hikes disproportionally affected the provinces’ highly indebted households. While the rebound in retail sales so far in 2024 signals a stabilization, consumer spending could nevertheless slow further this year in Ontario as more mortgages come up for renewal and population inflow normalizes. Population growth should low sharply from the 3.4% recorded in 2023 as the province faces the largest reduction in temporary resident intake in the country. Resilience in consumer spending could dissipate rapidly due to an evident cooling in the province’s labour market.

Non-residential investment should weather the slowdown better in Ontario than the rest of the country, offsetting continued weaknesses in the residential sector. The province achieved a 4.7% gain in real non-residential structures investment last year as Stellantis-LG and Volkswagen EV battery plants broke ground. Investment in the manufacturing sector is expected to boost growth in Ontario this year, according to the 2024 capital expenditure intentions, and the province continues to attract EV investment with a $15 bn new deal announced with Honda. Sustained growth in the public sector adds to the strength with the government announcing the most ambitious capital plan in history to address the long-standing infrastructure underinvestment. The upgraded Capital Plan totals $190.2 bn over the next decade—$5.2 bn higher than the previous plan. That includes $26.2 bn in FY2024–25—a 25% jump from last year.

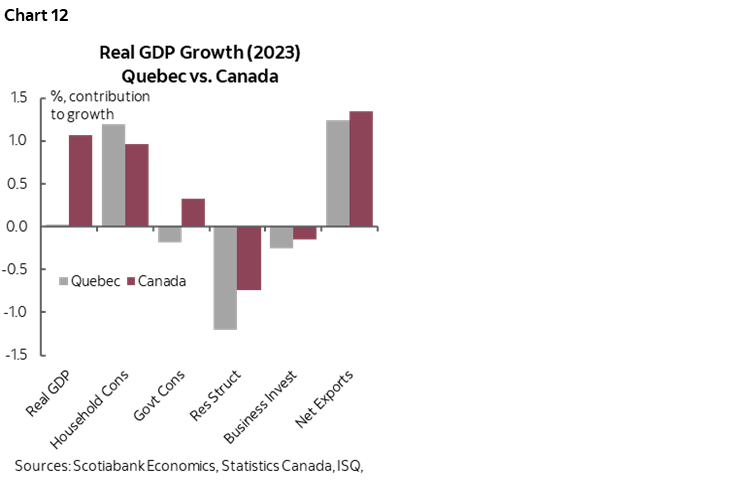

QUEBEC: WEAKNESS RUNNING ITS COURSE, UNDERLYING STRENGTH TAKES OVER

Quebec experienced a deeper slowdown last year with its economy contracting in the second half of 2023, driven by continued softness in residential investment and other disruptions such as droughts and public-sector strikes. We expect current weaknesses to run their courses and the economy to return to expansion this year on the back of underlying strength. Real residential investments bottomed to -17% below pre-pandemic levels in the second quarter—a larger decline than the rest of Canada—and remained subdued for the rest of the year. The slump in residential investment could be due to a normalization of strong activities in 2021–2022 that surpassed the rest of Canada, and housing starts should improve this year. Exports turned into a headwind for growth in Quebec, hampered by forest fires and production disruptions and weighed by the continued decline in forest products. Other than these transitory shocks, demand for Quebec exports remained solid.

Business investment is faring better starting the second half of last year and has room to improve. The province anticipates robust private investment in 2024 according to the capital spending intentions, layering on top major public investments in infrastructure. Construction of Northvolt’s $7 bn EV battery plant should support capital formation this year and next, and Hydro Quebec’s $90–$110 bn expansion plan ($7–9 bn per year) is another substantial one, as it is equivalent to around 10% of non-residential investments in the province.

Quebec led the country in household spending last year despite lower population growth than other jurisdictions. As fiscal stimulus waned, consumer spending started to taper off towards the end of last year. However, the province’s high household savings and relatively low debt burden serve as effective buffers in the ongoing consumption slowdown.

MARITIME PROVINCES: ROBUST MOMENTUM PREVAILS

Benefiting from record-level population influx from both international and inter-provincial migration, strong momentum continues to support above-trend growth in the Maritime provinces. Prince Edward Island (PEI) is set to rank among the top provinces in growth, while Nova Scotia continues to outpace the national average. New Brunswick may lag behind its maritime peers slightly due to softening exports and capital investments.

Household consumption remains well supported by job growth and low debt burden. Retail sales continue to thrive in the region, mirroring strong hiring, particularly in Nova Scotia and PEI. Households in the region carry the lowest debt burden relative to income and have experienced a notable decrease in debt burden since 2019, positioning them well against higher borrowing costs. Fiscal policy, especially in Nova Scotia, has become increasingly accommodative, with the government announcing big spending increases focusing on healthcare and housing while delivering tax relief to households.

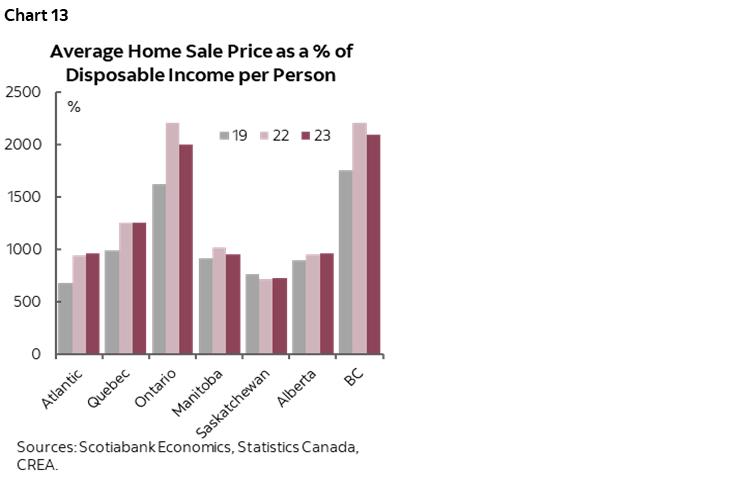

However, eroding housing affordability could dampen growth. Although home sales remained subdued, resale prices continue to climb, defying the national trend—a reflection of robust demand in the region. With price increases outpacing gains in disposable income, the Maritime region is losing its affordability advantage. Rising prices and tight demand-supply conditions spurred robust residential investment in the region despite high interest rates.

Private investment is expected to boost growth in Nova Scotia and PEI while posing headwinds for New Brunswick. Nova Scotia also anticipates strong public investment this year with a $1.6 bn capital plan.

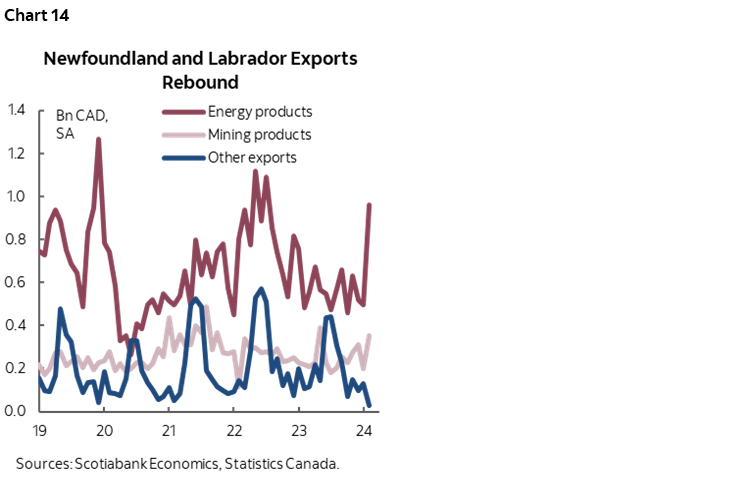

NEWFOUNDLAND AND LABRADOR: A LONG-AWAITED TURNAROUND ON THE HORIZON

After two years of negative growth, Newfoundland and Labrador anticipate a rapid rebound in oil production and investment in major projects to buck the trend of a global slowdown and sustain medium-term growth. Capital investment is expected to grow in 2024 as construction work ramps up on the West White Rose offshore oil project, combined with continued government investment in infrastructure projects. The wind-hydrogen sector brings significant upside to growth, with four companies granted rights to develop projects on crown lands, and a fifth expected on private land, projecting significant spending down the line and contributing to capital investment and GDP growth in the years to come. The province’s key exports are set to support growth in 2024, with the government projecting a rapid 12% boost in oil production from last year’s subdued levels as Terra Nova resumes full production to 29,000 bbl/d. Mining sector activities continue to pick up, driven mainly by the completion of the Voisey’s Bay Mine Expansion and higher production at the Iron Ore Company of Canada.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.