Next Week's Risk Dashboard

- FOMC minutes may inform a QT dialogue…

- …while the Committee’s soft confidence has probably gotten worse

- Canadian CPI—what matters and what doesn’t

- The BoC is very clear about its preferred inflation measures

- The BoC is messing up funding markets…

- …by weaving a complicated patchwork of QT defences

- The PBOC might be wise to remain on hold

- PMIs: EZ, UK, US, Japan, Australia, India

- BI expected to hold on rupiah concerns

- BoK to stand pat

- Turkey’s central bank soap opera

- Global macro

Chart of the Week

You know the kind of driver that speeds to the stop light only to slam on the brakes and wind up waiting in line like everyone else? That’s kind of what this week is going to feel like in the world of economics and markets.

FOMC minutes will tease us about potential QT and policy rate guidance but won’t do anything concrete and the dialogue may even be stale on arrival at least in some respects. Canadian inflation will be updated, but the BoC is in no rush to have to do anything other than glance at the figures and go back to checking the overnight sports highlights.

Decisions by the PBOC, BoK, BI and Turkey’s central bank plus modest data risk including PMIs will keep it lively. Just don’t expect a whole lot of earth shattering developments.

CANADIAN INFLATION—WHAT MATTERS AND WHAT DOESN’T

Canada starts off the week with markets on holiday for Family Day and then quickly gets down to business when January CPI lands on Tuesday morning. Key will be the BoC’s two preferred measures of underlying inflation, but only in a scorekeeping sense for now. There are no imminent decisions that are resting on the update.

The BoC Remains in Watch Mode

Why? Because the BoC has been clear that it’s in no hurry to adjust policy in either direction. Markets are pricing no change in the policy rate at the next decision on March 6th and this will be the last inflation reading before that meeting. There are, however, important updates on Q4 GDP growth and jobs before that decision, but the patient guidance also applies to those readings.

Governor Macklem has been clear in stating that the BoC is looking for evidence that underlying inflation is falling, that he wants to have confidence that it will stay on track toward durably achieving the 2% inflation target, and only then “we can begin discussing lowering our policy interest rate.” They do not sound like they feel they have even ticked the first box, namely that much more progress is required on underlying inflation.

Estimates

I’ve estimated a rise of 0.6% m/m NSA that would lift the year-over-year rate a tick to 3.5%. If so, then since January is a mild seasonal up-month for prices, seasonal adjustment factors would tamp down a little of that to a headline rise of about 0.4% m/m SA.

Traditional core CPI (ex-food and energy) is estimated to have risen by about ½% m/m NSA and by about 0.3% m/m SA.

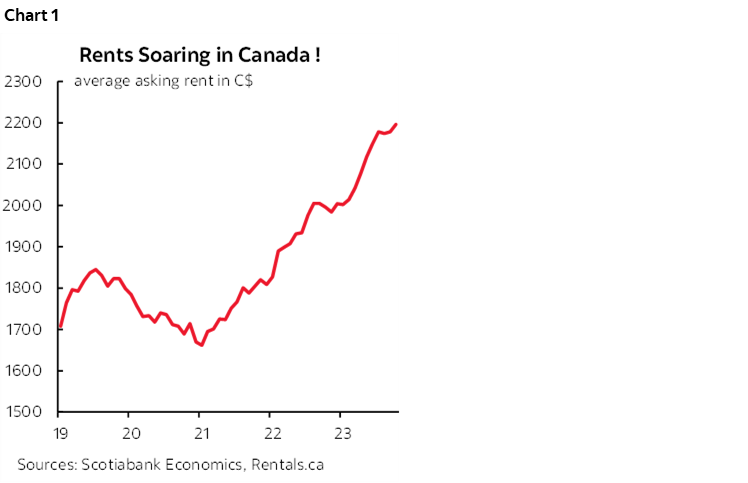

Year-ago base effects would lower the year-over-year headline CPI rate by half a point to 2.9%. Then we start to layer on bottom-up assumptions across components. For instance, average rent in the country is tracking a stronger than seasonally normal rise of 0.8% m/m NSA that could contribute about 0.1% m/m to traditional core inflation (chart 1). Gasoline prices fell a touch, but the small weight shouldn’t make it a meaningful contributor to headline inflation in m/m terms. Vehicle prices typically jump in January. The weakness during December in the recreation/education/reading category that carries about a 10% weight is expected to rebound.

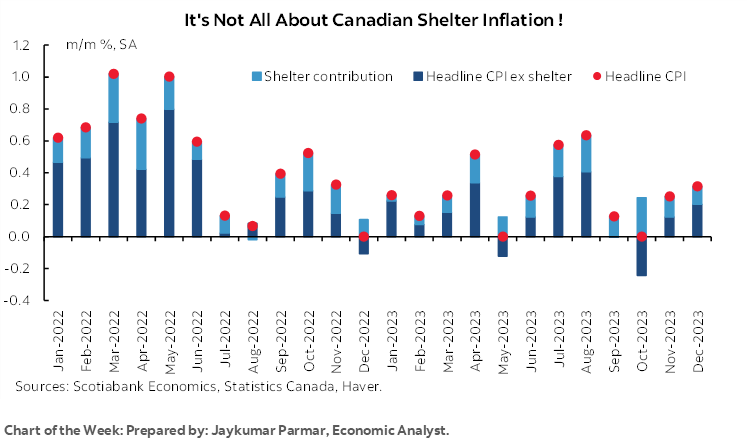

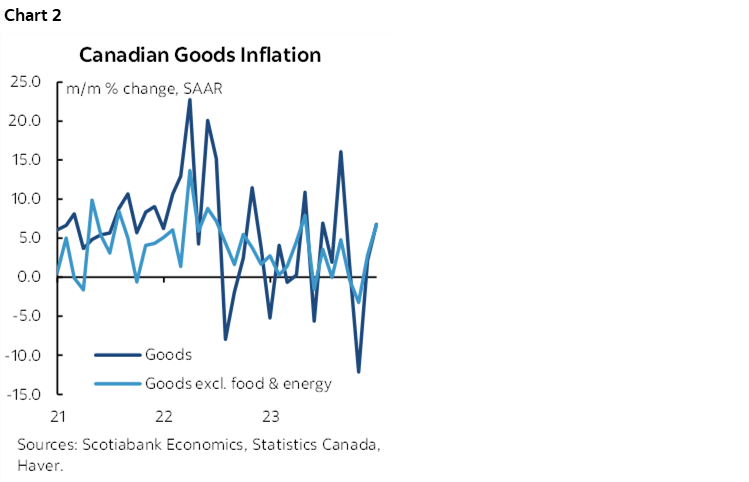

Key, however, may be an expected rebound in overall service prices given the 53% weight and following greater than normal seasonal softness in December (chart 2). Also note that it’s a fallacy that the only sources of pressure on Canadian inflation are coming from shelter costs. That same chart shows core goods inflation (excluding groceries and energy) that was hotter than seasonally normal as it accelerated to 6.8% m/m SAAR in December.

The BoC is Very Clear on the Two Measures that it Prefers

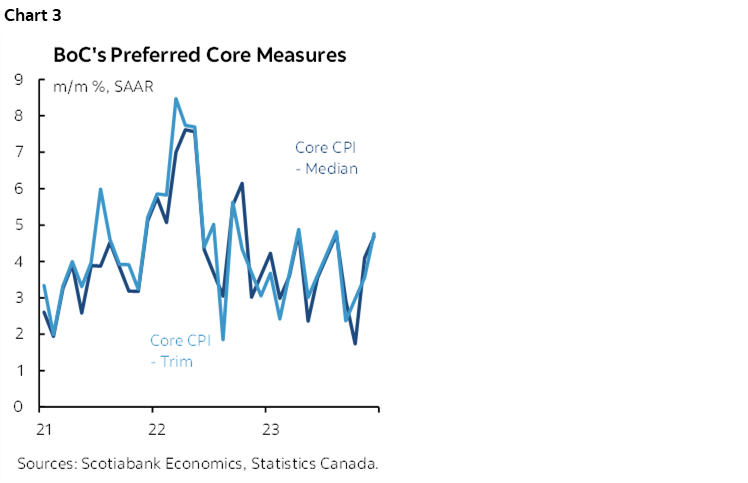

What happens to the Bank of Canada’s preferred gauges for underlying inflation will nevertheless determine the consequences for markets in the short run while the smoothed trend will inform the outlook for the BoC’s policy rate over time given the ongoing hot readings (chart 3). Canada has not yet entered a soft patch on underlying inflation. Trimmed mean CPI was 3% m/m SAAR in October, 3.6% in November and then 4.8% in December. Weighted median CPI was 1.7% in October, and then 4.1% in November and 4.7% in December.

There is, however, some unjustified confusion around what the BoC follows as its preferred core measures. There shouldn’t be. The BoC’s communications are very clear in terms of what measures are preferred. The MPRs explicitly state the following at the beginning:

“The Bank’s two preferred measures of core inflation are CPI-trim, which excludes CPI components whose rates of change in a given month are the most extreme, and CPI-median, which corresponds to the price change located at the 50th percentile (in terms of basket weight) of the distribution of price changes.”

There was a time about three years ago that the BoC confused folks with respect to which measures of underlying inflation it was relying upon. I think that time has long passed as the BoC really only talks about trimmed mean and weighted median CPI as preferred core CPI measures these days. Box 5 back in the April 2021 MPR (here) splashed no fewer than seven such measures including trimmed mean CPI, weighted median CPI, common component CPI, CPIX that excludes the eight most volatile items and indirect taxes, traditional core CPI that excludes food and energy and indirect taxes, CPIW that includes everything but with lower weights on more volatile components, and MEANSTD that does not use fixed weights but filters out large y/y changes thereby making it less susceptible to base-year effects.

That’s not to say that they also don’t consider breadth and many other perspectives on forward-looking inflation risk.

Of Course the BoC Can’t Just Ignore Shelter!

On that note, while Governor Macklem didn’t say this, should monetary policy look through shelter cost inflation in Canadian CPI? Macklem’s recent messaging on this topic got misinterpreted by some.

What I heard him say is that they target total inflation over the medium-term but can’t ignore shelter given it is a big component, but they also can’t fix affordability issues. Here are some reasons why shelter cannot be omitted from CPI when doing so could lead to misleading interpretations about how the BoC is about to ease because the rest of the basket ex-shelter is looking like it’s better behaved.

Upside risk to shelter costs may well intensify into the Spring housing market.

Multiplier effects of housing market activity on other categories could become material. Therefore, it’s not clear that shelter crowds out pricing power in the rest of the economy as opposed to buoying more widespread pressures.

In today’s environment, households don’t differentiate between sources of inflation in forming expectations and changing behaviour. They just think the cost of living is going up and so they demand bigger wage gains which feeds further inflation. Therefore, it’s a mistake to dismiss shelter cost as a relative price effect on CPI in the context of today’s realities as opposed to in the past when such evidence of changing behaviour was not apparent.

There are multiple other sources of inflation risk, like very strong wage growth, previously flagged evidence from the S&P PMI for Canada that service sectors plan on passing on higher wages and other costs through prices, moribund labour productivity, excessive immigration, a very slow movement toward excess supply that may be interrupted into 2024H1, excessively stimulative fiscal policy that may become more so including through the pharmacare program that is likely to be introduced in the Federal budget and targeted initiatives.

One thing that is clear is that the BoC’s preferred measures of underlying inflation are unaffected by mortgage interest costs within shelter CPI. Mortgage interest has not been included in either the trimmed mean or weighted median measures of underlying inflation throughout the entire rate hike cycle and even well before then.

FOMC MINUTES—HEY THERE QT

Minutes to the FOMC’s meeting on January 30th – 31st will be released at 2pmET on Wednesday. A recap of that meeting’s communications is available here. The key focus will be upon balance sheet policy guidance. A secondary focus will be upon anything that is offered on policy rate guidance after Chair Powell all but ruled out a near-term cut.

Expect Light Balance Sheet Guidance

During his press conference on January 31st, Chair Powell was asked whether the Committee had discussed slowing the pace of balance sheet run-off in the months ahead. He said that the run-off has gone well so far, and that:

“We did have some discussion on the balance sheet. We’re planning to have more in-depth discussion in March.”

That translated into a need to watch this round of meeting minutes for limited guidance, but that more of the meat will focus upon the discussion to be held at the March 19th–20th meeting. The gap in between may be filled in by communications over the inter-meeting period since the March meeting is the earliest point at which to possibly expect a policy decision to begin reducing roll-off from the current pace of US$95B/month through Treasuries (US$60B/month) and maturing MBS (US$35B/month but typically less).

Powell may have guided that the Committee is not inclined to abruptly end QT when he said “We’ll be looking at a variety of things over the next year or so” in reference to the criteria for tapering QT. The implication may lend itself to our belief that QT may be gradually wound down over a roughly one-year period.

Whatever may be guided at this time, expect the Committee to continue to say that QT and the policy rate are treated as separate tools that don’t necessarily have to be aligned. In plain English, stepping back from QT in the nearer term does not necessarily have to be viewed as a step toward cutting the policy rate.

Policy Rate Guidance—The Fed’s Confidence Problem Hasn’t Gotten Any Better

The Committee’s discussion on the criteria that would inform if and when to begin cutting the policy rate is likely to be stale on arrival. The meeting was held before strong jobs and wages including the effects of revisions (here) and stronger than expected core CPI (here). Those two reports struck to the heart of the dual mandate by reminding the Committee to be careful about prematurely declaring victory.

In other words, the limited confidence that Chair Powell described at the January press conference is probably even more limited now. Recall he said the following:

“We have confidence. We’re looking for greater confidence. Implicitly our confidence has been gaining. We want to see more data, a continuation of the good inflation data. Is the 6 months of good inflation data a signal we’re on a sustainable path toward achieving 2% sustainably? The data is low enough. But can we take it as sustainable, that’s what we’re talking about. We’re looking for inflation to continue coming down as it has for the past six months.”

And don’t forget his warning:

“The greater risk is that inflation stabilizes at a level above 2% rather than accelerates. We would have to respond if inflation moves back up again and both of those scenarios are risks.”

Reasons to Taper QT

So if it’s not about the fundamentals that appear to be strong, then why all the chatter about curtailing balance sheet run-off?

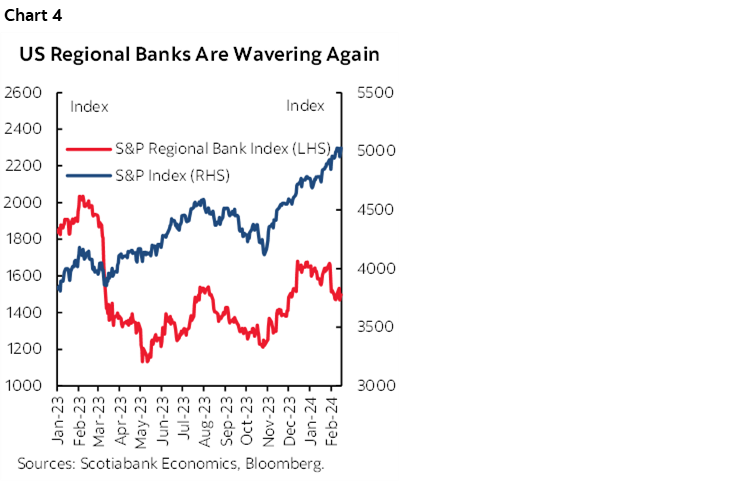

For years now, there has been the widespread feeling that the day would come when underestimated frailties would be exposed across a disparate array of funding franchises across the US financial system. The regional banking crisis last Spring was a good example of this, aided by widespread ineptness among the affected regional banks. Those frailties would force the Fed’s hand toward pulling back on QT plans by this year. Recent challenges have resurfaced across a select few regional banks and that has hurt the KBW regional banks stock subindex that is about 14% below the recent peak toward the end of last year even as the S&P500 has risen over this period (chart 4).

As a reminder, the driving issue is the depletion of bank reserves and liquidity at money market funds and the vulnerabilities to the financial system that could arise. When the Fed was engaged in Quantitative Easing and liquidity management, the aim was to buy reasonably safe assets—primarily Treasuries and Mortgage-Backed Securities—and inject cash into the market on reasonably favourable terms. The result drove higher bank reserves held at the Fed and higher repo facility balances held by money market funds. The hope was that injecting this liquidity would give these groups more cash to buy other securities and to lend, and therefore add to the effects of rate cuts in lowering borrowing costs while stoking economic growth and countering disinflationary pressures.

As the economy strengthened and inflation rose, Quantitative Tightening sought to reverse this chain of effects as a complementary form of policy tightening to the primary tool of raising the fed funds target range. It entailed allowing the Fed’s holdings of securities to drop off the balance sheet as the amounts matured at a controlled pace of US$60 billion per month for Treasuries and $35 billion per month for MBS, although they tend not to be able to run off MBS holdings at this pace. As issuance replaces the retired securities, banks have to deplete their reserves to fund their securities holdings and money market funds have to run down RRP balances. The effects are to provide less money to lend, less money to invest in securities holdings, and hence less stimulus to growth and inflation.

The problem is that nobody wants this process to go too far. If banks’ reserves and money market funds’ RRP balances are depleted too rapidly and sink too low, then it could trigger problems in funding markets. It could result in forced selling of securities holdings and excessive damage to lending channels while scarce liquidity puts upward pressure upon repo rates and broader funding costs. This is what happened in late 2019 and the Fed has since adopted a more liberal ‘ample’ reserves framework.

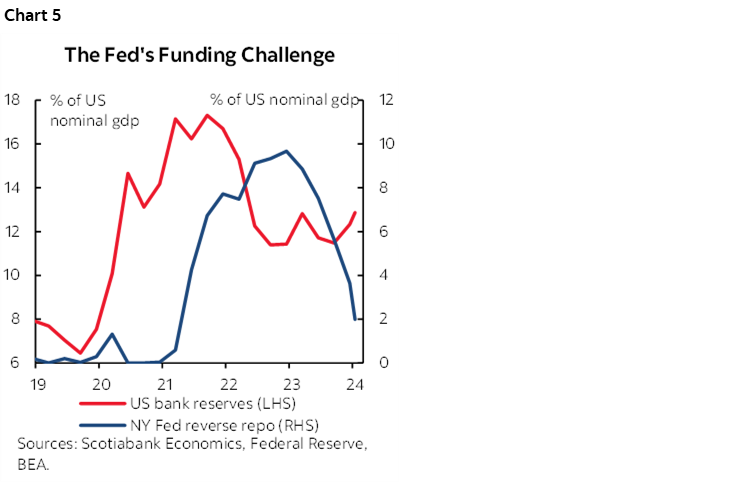

The ample reserves framework is now being tested (chart 5). Reserves are at just over 12% of NGDP when the Fed has indicated 10–12% is their target range. That indicates reserves are still ample, but getting closer to the target range that would require slowing the pace of QT runoff notwithstanding the fact that policies applied over the past year have taken reserves up from the depths that were being reached in early 2023. RRP balances, however, continues to fall at a rapid pace; from a peak of over US$2.5T at the end of 2022, they have fallen back to about half a trillion now and hence only half a trillion above pre-pandemic levels. Most forecasters expect that reserves and RRP balances could become too tight by Spring and so the Fed would want to head off a funding market challenge beforehand. The tighter RRP balances become, the greater the risk that renewed downward pressure upon bank reserves will arise.

INFLATION VERSUS ENDING THE BoC’S QT EARLY

The discussion on Canadian CPI and FOMC minutes can serve as a segue into a reminder about what I expect by way of BoC balance sheet policies.

If the decision was solely based upon the inflation mandate, then the BoC would probably not be in a rush to end policy tightening through QT that is designed to drain reserves from the banking system. It would probably wish to keep tightening policy through that tool and perhaps stay on course toward its initial plan to end QT toward the end of 2024 or early 2025.

This is the logic that is guiding our thinking behind why the BoC is unlikely to be cutting until September, and that an awful lot has to go right in order to cut by then amid ongoing hike risk. How far in advance that the BoC would wish to end QT before cutting or whether they would wish to time the two policies is unclear. But balance sheet policy doesn’t necessarily have to be driven by the same factors that drive the policy rate as the dominant policy tool.

I first wrote about the likelihood that the BoC would be ending QT by about six months earlier than initially guided in daily notes last Fall and in this Global Week Ahead on December 1st that said “It could be 6+ months earlier than initially thought.”

The main reason for the recent and sudden elevated interest was the announcement by the Toronto CFA Society (here) back on February 9th—flagged for clients at the time—that BoC Deputy Governor Gravelle would be delivering a speech titled “Normalization of the Balance Sheet” on March 21st. That jumped the gun on the BoC’s speech announcement.

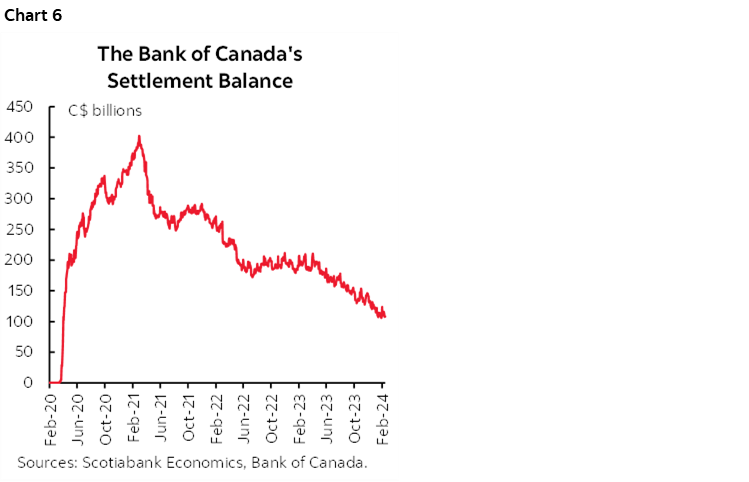

The underlying logic behind guiding a potentially earlier end to QT remains generally intact but with an added complication. Settlement balances are rapidly falling to C$108B (<5% of NGDP), or about one-quarter of the pandemic-era’s peak (chart 6). That is rapidly getting closer to the target of C$20–$60B of balances toward the end of 2024 or early 2025, or 1–2% of nominal GDP. By April, another C$30 billion of the BoC’s GoC bond holdings will mature and drop off the balance sheet, potentially bringing settlement balances that much closer to the upper end of the BoC’s target range. The BoC has nevertheless indicated that they intend to issue a cash management bill in order to refinance that.

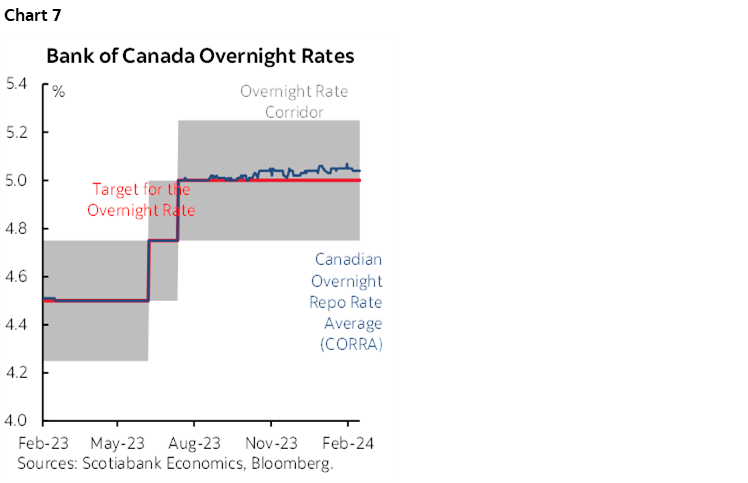

In addition to cash management bills, the added complication is that the BoC is embracing alternative tools in an effort to control pressures in funding markets. To date they are not working, and they may not work unless dramatically raised. The Canadian Overnight Repo Rate Average (CORRA) continues to trade several basis points above the overnight rate (chart 7) despite constant injections of liquidity through repo and despite the recent announcement that receiver general auctions would be introduced, although they have yet to be applied.

The BoC announced here that the receiver general auctions will commence on February 21st and will be conducted daily at an initial size of C$5 billion across overnight through 3-day tranches. They made it clear that any changes to the amounts will be based on government cash management needs which strengthens our understanding that the purpose is to generate a better return for government cash balances.

The key here is the degree to which the BoC is comfortable relying upon alternative tools to prop up liquidity in funding markets versus tackling the root cause of the challenges. As previously written, I still view ending QT earlier than guided as the cleaner solution versus relying upon a complex patchwork of funding tools like cash management bills, repo injections, and receiver general auctions. If the BoC is not of the same opinion and doubles down on QT while supporting funding markets through other means, then it could be a sign they are nowhere close to easing—if not open to further tightening—but that decision would have to be supported by an assessment that they have not done enough to durably bring inflation toward the 2% target within a reasonable period of time.

Another possibility is that such funding tools are being ramped up in anticipation of loan demand into the Spring housing market that could worsen funding market pressures. Those signs are intensifying in my opinion.

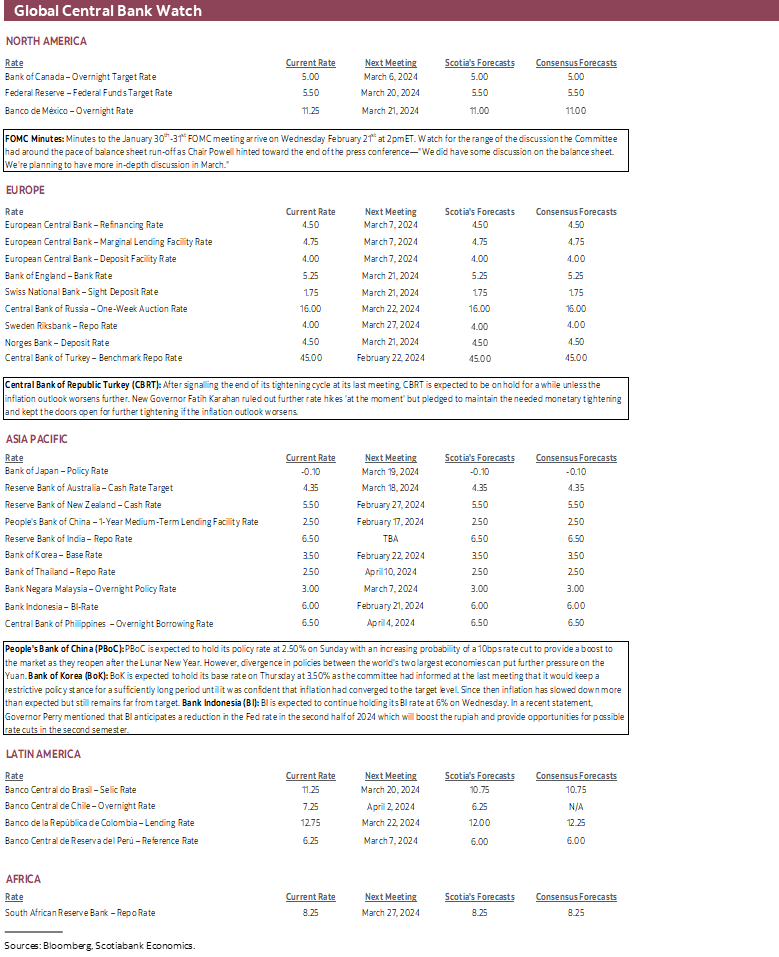

CENTRAL BANKS—WILL THE PBoC CUT THIS TIME?

FOMC minutes will dominate global central bank risks along with the risk of easier monetary policy in China, but a few regional central banks will also weigh in during the week.

The PBOC and Chinese Banks Might Cut

A minority within consensus once again thinks that the People’s Bank of China may cut its key 1-year Medium-Term Lending Facility Rate over the weekend. Such expectations did not pan out well into the last decision in January when the PBOC held. A cut would be the first since last August as Chinese policy makers have relied upon other measures such as reduced the required reserve ratio, expediting loan growth, somewhat easier regulations and targeted fiscal relief.

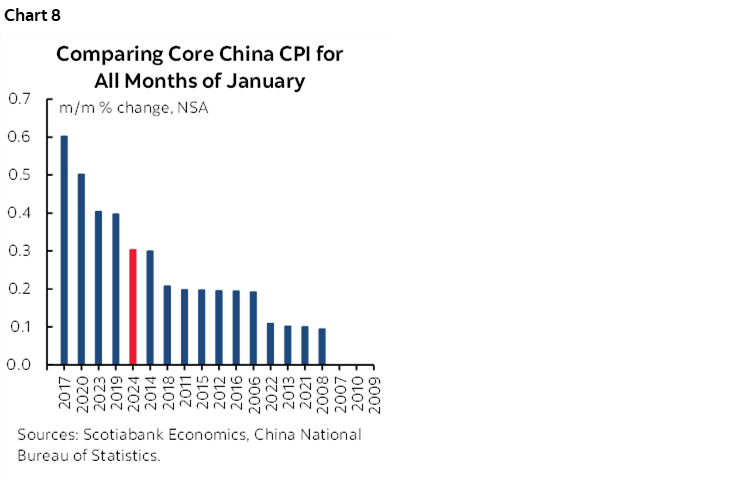

What may play against a cut narrative is that core CPI has been tentatively rising of late with stronger than usual m/m increases in back-to-back fashion (chart 8). This year’s slight softening in the yuan as expectations for Fed easing get pushed out may also restrain the PBOC’s flexibility given the stability risks.

Partly depending upon what the PBOC decides, Chinese banks may lower their 1- and 5-year Loan Prime Rates on Monday night (ET). Consensus is divided between expecting no change versus cutting the 1-year LPR by between 5–15bps. Consensus is also divided between no change and up to a 15bps cut to the 5-year LPR that matters more to the housing market.

Bank Indonesia—Waiting for the Currency

The policy rate is expected to stay on hold at 6% on Wednesday. Currency weakness is holding the central bank back from easing.

Earlier this month, Governor Perry Warjiyo made this clear when he said:

“If we rush while the global condition is in disequilibrium, the rupiah could weaken and inflation goes out of control.”

Inflation is running at about 2½% which is very close to the inflation target within a range of 1½% to 3½%, but the rupiah has been on a weakening trend so far this year.

Bank of Korea—An Extended Holding Period

Thursday’s decision is likely to keep the base rate unchanged at 3½%. The prior decision in January dropped reference to how it would “judge the need to raise base rate further” but then doused any inferences that it was moving toward easing. Governor Rhee Chang-yong said “My personal view is that I see little changes for the next six months” in reference to easing. He went on to note:

“Any premature rate cut could reignite inflation expectations which could adversely affect the economy by triggering expectations about a property market boom, rather than work to support growth.”

Central Bank of Turkey—The Soap Opera Continues

Think your rates are high? Try 45%. Turkey’s central bank is widely expected to keep its policy rate there on Thursday. That’s the cost to years of mismanagement and political interference. The central bank said in January under the previous Governor that “the monetary tightness required to establish the disinflation course is achieved” which strongly indicated that a prolonged pause for “as long as needed” would follow.

Since then, further turmoil has been unleashed in about as close to a soap opera as central banking gets. Governor Hafize Gaye Erkan resigned and new Governor Fatih Karahan was appointed. The turmoil drove further lira depreciation. Expect him to caution that while the policy rate is likely to be maintained, the risk of further tightening remains material.

OTHER GLOBAL MACRO

The rest of the global macro line-up will be fairly light and largely devoid of measures that could offer any shock effects on markets.

Purchasing managers’ indices covering the month of February will be the main set of global releases over the coming week. Australia and Japan kick it off (Wednesday), followed by the Eurozone, US, UK and India (Thursday).

Canada also updates retail sales estimates on Thursday for both December and January. Statcan’s advance guidance on January 19th said December was tracking a rise of 0.8% m/m in nominal terms based on a 49.4% response rate. Take that with high caution, however, given the high revision risk. Key, however, is more likely to be advance guidance for January as the new information.

The US faces a light week that starts with markets shut on Monday for Presidents Day. Only the S&P global PMIs for February (Thursday) and existing home sales for January (Thursday) are due out.

Eurozone CPI revisions for January (Thursday) and the ECB’s survey of 1- and 3-year CPI expectations (Friday) are also due.

Australia updates Q4 wage growth comes on the heels of the prior quarter’s acceleration to the fastest rate of increase on record for the series and set against an accelerating trend (chart 9). Australia’s job market has softened of late as prior strength may have pulled forward job gains from December’s loss of 63k jobs and then January’s flat reading.

Light inflation updates will come from Sweden (Monday), Malaysia (Thursday) and Singapore (Friday).

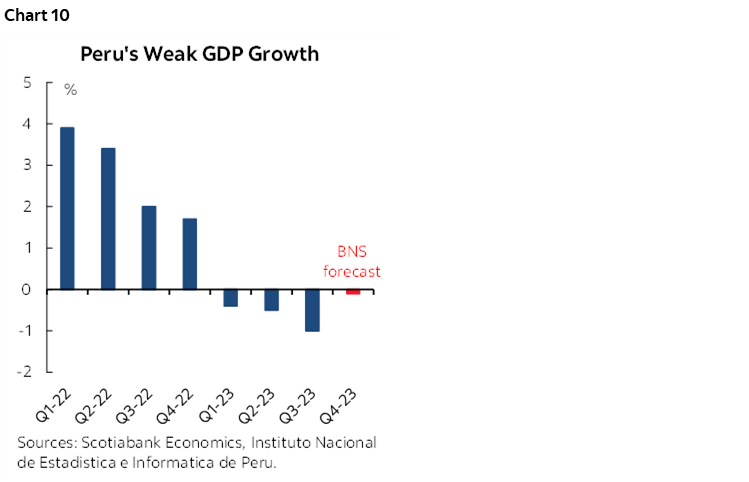

LatAm markets face Peru’s Q4 GDP report (Friday). Growth has been rebounding in quarter-over-quarter terms and the year-over-year rate might finally stop contracting or come very close to doing so (chart 10). Mexico updates retail sales for December (Wednesday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.