SUMMARY

- Russia’s invasion of Ukraine on Feb. 24, 2022 has dominated headlines around the world, rattled global markets, and thrown into question established geopolitical norms and agreements.

- From a commodity price perspective, oil has been the most obvious and immediate beneficiary of the conflict given Russia’s share of global production; we now expect higher crude values and volatility for at least the near term.

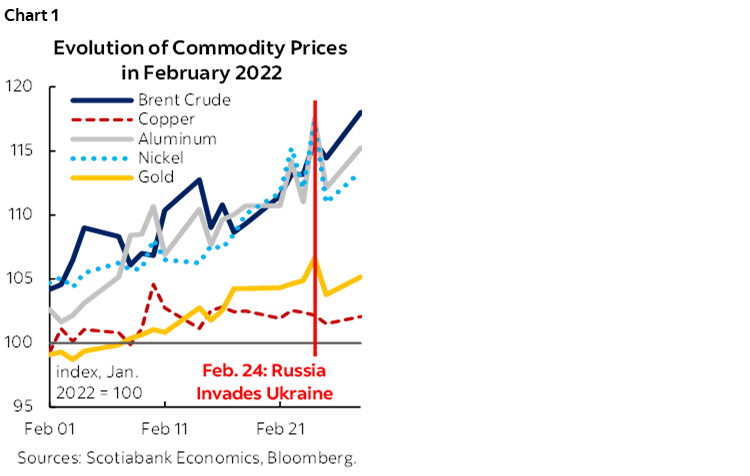

- Copper, nickel, and aluminum prices also received significant boosts in February (chart 1)—Russia is a major producer of all three metals—but iron ore’s increase was more muted because of mitigating developments in China.

- Daily closing values for gold prices ranged from 1,792 USD/oz to 1,936 USD/oz in February; the macroeconomic environment is now more supportive of the yellow metal.

- With no immediate end to the conflict in sight, most of the commodities in our coverage universe look likely to see material upward price pressures beyond those assumed our January 2022 forecast.

WAR SHAKES UP GLOBAL POLITICAL ECONOMY

Russia’s invasion of Ukraine on Feb. 24, 2022 has dominated headlines around the world, rattled global markets, and thrown into question the established geopolitical order. Accordingly, our expectation of a fairly synchronized path of economic recovery as the omicron variant is brought under control now looks likely to be bumpier than we previously thought.

The situation is highly uncertain; at this time, we see four key economic impacts from the conflict, all of which should persist to some degree. The first is surging commodity prices via supply disruptions—Russia is the third-largest oil producer and second-largest natural gas producer in the world; Ukraine is a major grain exporter. The second is economic uncertainty and equity market volatility following a breach of post-Cold War norms respecting the borders of sovereign states; policy and equity uncertainty indices and the safe haven US dollar have been bid up following the invasion. Third, snarled trade routes in Europe will likely add to existing supply chain and inflationary woes—US CPI rose by a nearly 40-year high of 7.5% y/y in January, before war broke out. Fourth, the airline industry and jet fuel demand could take hits with flights grounded around the world.

Despite the incursion’s myriad implications for the real economy, our core monetary policy assumptions are unchanged at this time. The Russian Federation’s financial linkages to the wider world are more limited since the Crimean invasion of 2014, and we expect the Bank of Canada and Federal Reserve to remain focused on fighting inflation and that both will raise policy rates by 175 bp in 2022. For Canada, the strength of Q4-2021 GDP growth—predicted by our nowcast model—all but assures a rate hike this week. Of course, global escalation of the current conflict could alter our outlook.

SANCTIONS HEIGHTEN EXISTING OIL SUPPLY CONCERNS, SUPERCHARGE PRICES

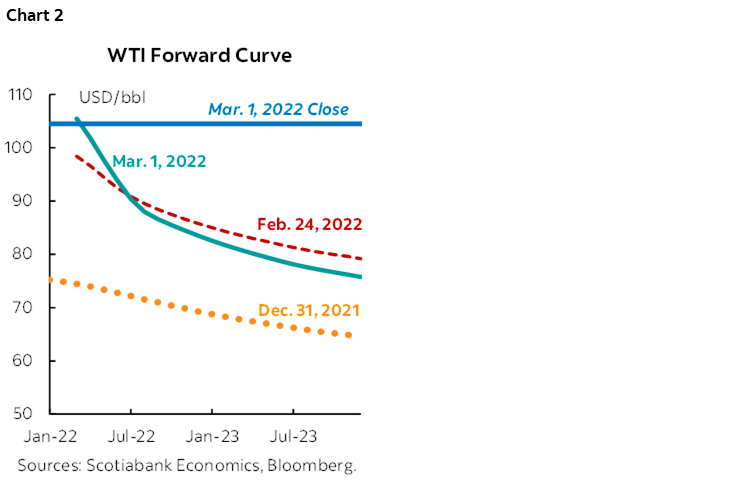

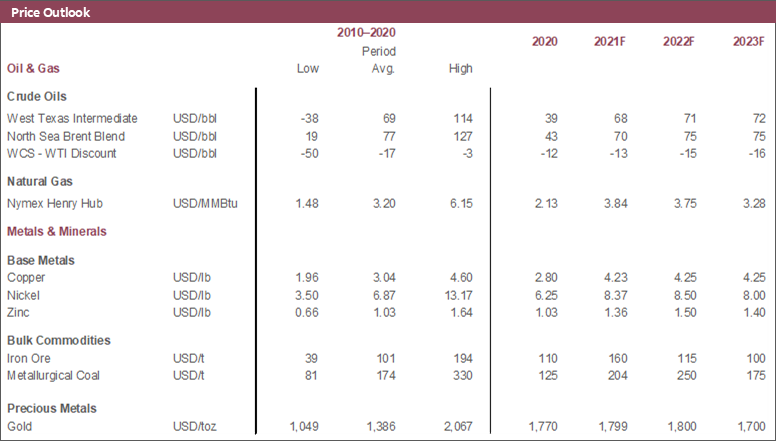

Oil has been the most obvious and immediate beneficiary of the Russia-Ukraine conflict, and we now expect much stronger crude values this year with heightened volatility in the near-term. Both the Brent and WTI benchmarks recently eclipsed the 100 USD/bbl threshold for the first time since 2014—the peak year of the last commodity super cycle—and continue to trade near that mark. With sanctions in place and no end to this conflict in sight, our January 2022 forecasts of 70 USD/bbl WTI and 73 USD/bbl Brent in H1-2022 are no longer feasible. Bloomberg median consensus forecasts assume 76 USD/bbl for WTI and 78.50 USD/bbl for Brent this year; forward curves—having shifted significantly higher since late 2021—suggest even higher values this year and next (chart 2, p.1).

Other bullish supply-side factors remain in place. Fears remain that OPEC+ will not be able to ramp production up to target rates and we still expect capital discipline in the US shale patch per company guidance. This latter effect naturally follows several years of commodity price volatility, though the sheer strength of the recent gains in crude values plus the increasing likelihood of persistence presents some upside potential on this front.

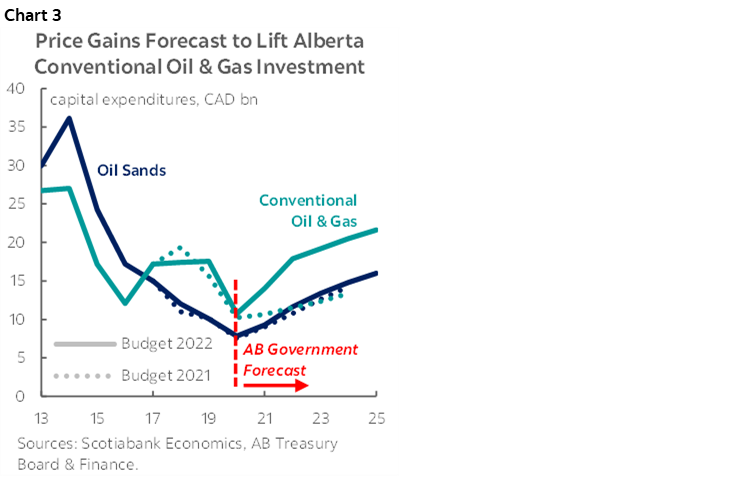

In Canada, oil price surges add to an already improving outlook in oil-producing provinces. WCS has generally tracked light crude benchmarks, last week rising above 80 USD/bbl for the first time since 2014; that surge in crude values comes as production, investment, and new egress capacity already looked to be ramping up. Canadian oil and gas capital outlays continued to climb in the fourth quarter of 2021 and Alberta crude output—despite a small decline in December 2021—remains near an all-time high. Early projections already looked good before supply concerns arose: last week’s Alberta budget (see our analysis here) revised conventional oil and gas investment—more sensitive to price movements—significantly higher through 2025 (chart 3), and Statistics Canada’s investment intentions survey for 2022 reported expectations of a hefty 22% increase in sectoral capital expenditures.

BASE METALS GAINS MORE MODEST, POTENTIAL FOR FURTHER SPIKES REMAINS

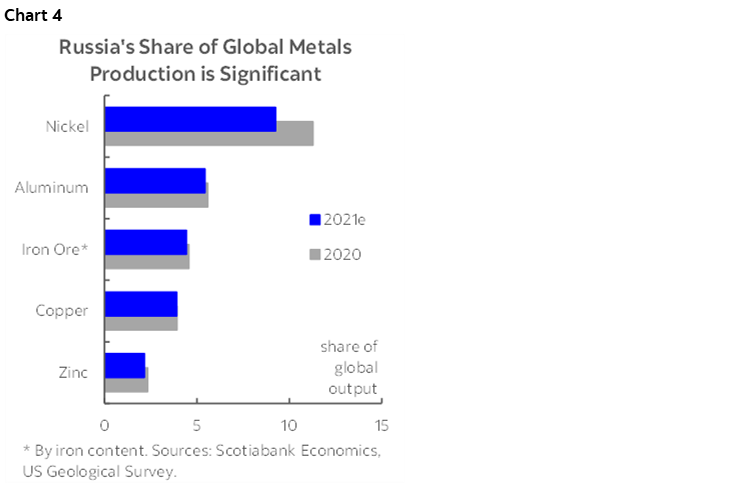

Copper, nickel, and aluminum prices received significant boosts in February—again an understandable result given that Russia is a major producer of all three metals (chart 4). Nickel hit its highest level since 2011, while aluminum reached an all-time high. Zinc and copper, for which Russia accounts for a smaller share of global output, increased more modestly in value than the other base metals. Prices for the red metal also gained following the publication of weak production data from Chile—the world’s largest producer of copper—which may have been linked to mine maintenance work and inclement weather—to average more than 4.50 USD/lb for the first time since May 2021 when they set an all-time record. Needless to say, so long as Russian supply concerns remain, there is upside risk to the price forecasts we laid out for these metals in January 2022.

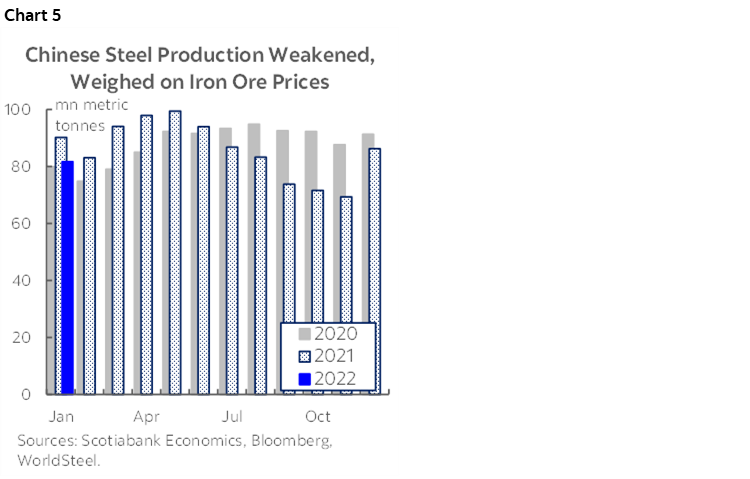

Though iron ore values saw upward movement related to supply disruption fears in late February, their increase was more muted because of other factors. Earlier in the month, a Chinese government announcement of investigations into iron ore inventories and trading activity was followed by transactions fees for some futures contracts and a plunge of about 15 USD/t. Chinese steel production—into which iron ore is an important input—also weakened in January amid ongoing emissions curbs related to the Beijing Winter Olympics (chart 5). There had been hopes of better results after data from late 2021 indicated some success reining in output and pollution levels. More positively, China appears ready to further boost infrastructure spending—with funding from special-purpose bonds that do not impact headline government debt numbers—to sustain economic momentum amid a slowing real estate sector. More details will be announced during the March 5 National People’s Congress; this presents upside potential for steel demand and iron ore consumption going forward.

UNCERTAINTY BIDS UP SAFE HAVEN GOLD

Daily closing values for gold prices ranged from 1,792 USD/oz to 1,936 USD/oz in February; the macroeconomic environment now appears more supportive of the yellow metal. Bullion values began to drift higher after US inflation—against which it is used as a hedge—was reported to have reached a nearly 40-year high in January. It then surged on February 24 as investors sought safety when Russia invaded Ukraine and speculation rose that the former country might liquidate its bullion reserves to cover the costs associated with global sanctions. Gold should remain well-supported in this environment of greater-than-predicted uncertainty created by the geopolitical conflict as well as potentially stronger-than-forecast price appreciation.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.