- Peru: April inflation should fall comfortably within the BCRP target range

French, and then Eurozone, inflation and GDP beats have global rates markets on offer, with yields gradually rising and undoing a good portion of yesterday’s declines. The risk mood looks a bit negative today as the USD strengthens against most major currencies—the MXN stands out with a small gain to trade below 17—and US equity futures trade slightly weaker, while metals are on the backfoot against crude oil unwinding a very small part of its Monday decline on ceasefire optimism. G10 markets await Canadian Feb/Mar GDP and US Q1 employment cost index data, both at 8.30ET.

Today’s Latam calendar is packed with key data and events before local markets close for Labour Day tomorrow—though that doesn’t stop Peru’s INEI from releasing April CPI data (see below). At 14ET, BanRep will deliver its policy decision where a 50bps cut is universally expected in a split vote (Fin Min Bonilla will probably vote for 100bps). We refer our readers to our Colombia team’s preview in yesterday’s Latam Daily, highlighting that the bank’s board remains cautious about “the convergence to the [inflation] target rate being slow, and, in the communique and in [the March meeting] minutes, they emphasized their compromise to take inflation within the target range by mid-2025, which shows that they are very concerned about credibility.”

At 8ET, Mexico’s INEGI publishes Q1 GDP figures that are expected to show the q/q pace holding at an underwhelming 0.1% rise with not much doing in the y/y rate at 2.3% y/y from 2.5% in Q4-23. Assuming no change in output in March, then the IGAE monthly data would point to about 2% y/y growth for Q1 but also a small negative quarter-on-quarter due to weakness in construction and manufacturing wile services remain in decent shape. Regardless, the Q1 expansion will undershoot Banxico’s forecast of 2.8% but this is no reason to favour a May cut. This is especially true after last week’s strong H1-Apr CPI print. Despite the beat generally coming from non-core categories, Banxico is worried about unanchored expectations and elevated headline inflation readings don’t help here.

At 9ET, Chile releases a collection of March macro data: retail sales, commercial activity, unemployment rate, industrial/manufacturing production, and copper output. Combined, the data will greatly impact expectations for Thursday’s monthly economic activity release, where we expect a below-consensus 0.5% y/y rise (see our team’s preview here). We got some relatively hawkish comments from BCCh Pres Costa yesterday, who noted that officials need to be cautious about the speed of rate cuts but also that inflation expectations remain well anchored.

—Juan Manuel Herrera

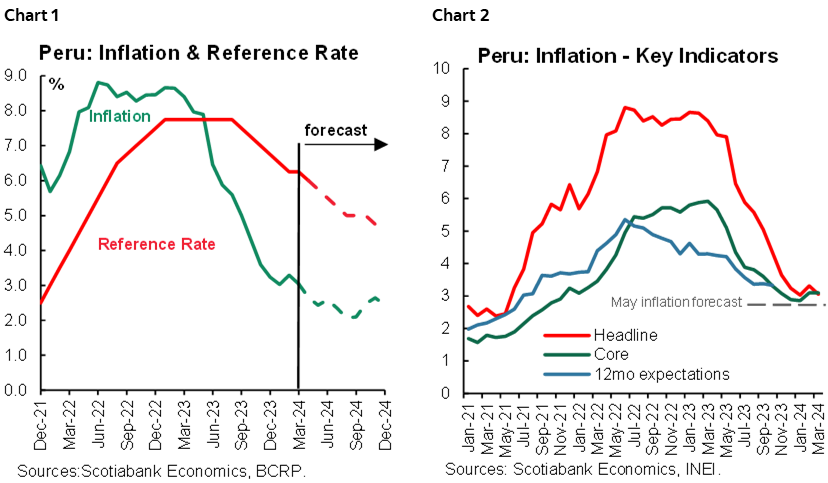

PERU: APRIL INFLATION SHOULD FALL COMFORTABLY WITHIN THE BCRP TARGET RANGE

The main economic figure that will be released this week is inflation for April on May 1st. The key prices that we track point to a monthly inflation of just under 0.2%. If so, yearly inflation for April should fall decisively within the BCRP target range (1% to 3%), to around 2.7%, from 3.0% in March. This would give the BCRP plenty of room to reduce its reference rate on May 9th, which is what we expect, from 6.00% currently, to 5.75%.

The BCRP has been giving mixed signals lately regarding their intentions. We view the BCRP as mostly concentrated on inflation and how it is performing with regards to its target inflation range. It has also signaled its concern over interest rate differentials between the BCRP and Fed policy rates that could eventually motivate an outflow of offshore short-term capital from PEN assets. Of the two concerns, the first appears to be much more important. The BCRP paused in reducing rates in March, after February inflation rose to 3.3%, moving away from its target range. In April inflation declined to 3.0%, on the cusp of the target range, and the BCRP lowered its rate. If inflation falls below the 3.0% range ceiling tomorrow, as we foresee that it will, then we would expect the BCRP to lower its rate despite uncertainty regarding the Fed rate.

On May 1st, March GDP growth figures for mining and for fishing are also on tap. Fishing is immaterial, as March was between fishing seasons. Fishing growth in April, however, could be quite impressive. Apparently, there are plenty of fish in the sea. Last year’s lacklustre catch, due to El Niño, has allowed the supply to be replenished, and the current cold ocean water is making the fish readily available. As a result, the government has determined a higher-than- usual quota for anchovy (fishmeal) fishing. The fishing season began recently in the latter half of April, and it’s our understanding that it is going extremely well.

Mining output has been quite robust, up 10.7% y/y in January–February. Daily production in March should maintain this rhythm. However, March this year has two working days less due to Easter (which was in April in 2023), and this should weaken the monthly figure somewhat. No worries, though, as March’s Easter losses will be April’s gains.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.