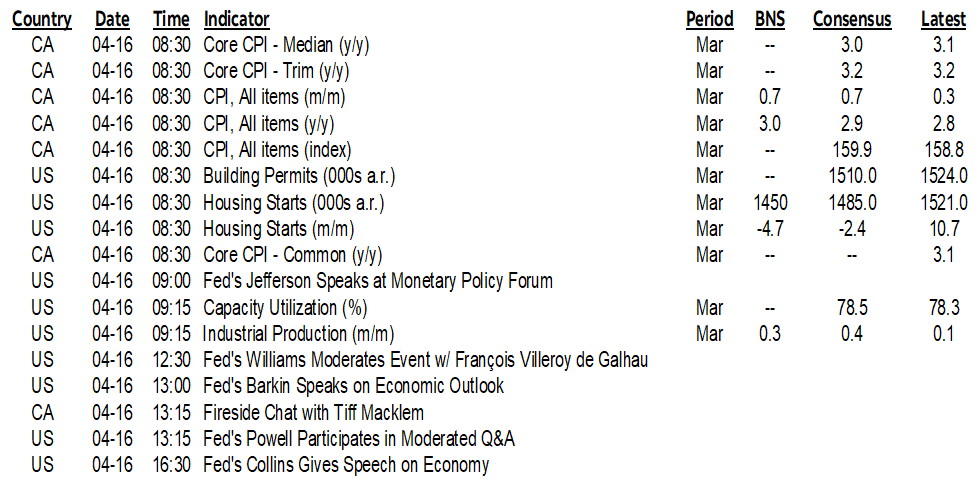

| ON DECK FOR TUESDAY, APRIL 16 |

KEY POINTS:

- Bonds, stocks continue to sell off

- Canadian core CPI: will the soft patch fade or extend?

- BoC’s Macklem to speak post-CPI

- Canada’s Federal Budget: Big Spending, Tax Hikes, Deficits forever...

- ...as Trudeau/Singh/Freeland fight for their political lives with an election ahead

- Canada to raise taxes on upper income earners and corporations

- Who are the ‘under 1%’ of earners being targeted for tax hikes in Canada?

- Fed’s Powell to speak after recently strong data

- Gilts sell off after strong wages despite job losses

- China’s economy beat expectations

- US earnings: BofA, MS in focus

Sovereign bonds and stocks are under selling pressure this morning. Some of that is the ongoing spillover effect from US retail sales that beat expectations yesterday. Gilts and sterling are outperforming after strong wage gains were recorded this morning despite job losses. China’s economy also beat expectations. But the main focus today will be upon Canada from start to finish, anything that Fed Chair Powell says, and the continuation of US earnings season.

Let’s get the overnight stuff out of the way before the main focal points.

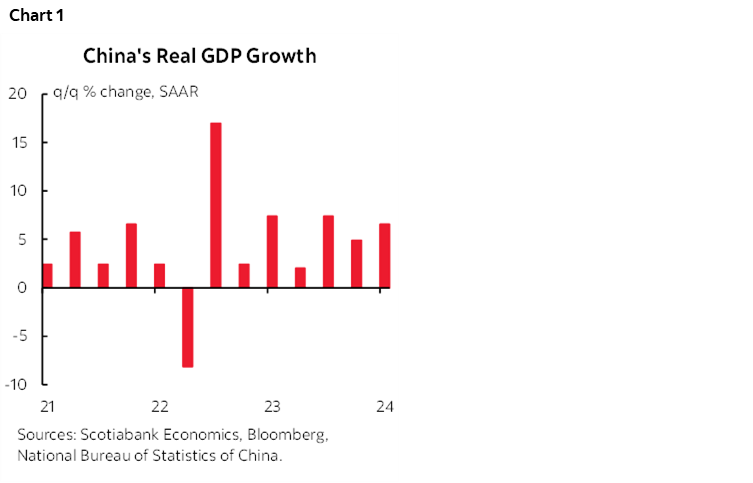

China’s economy beat expectations with Q1 growth landing at 1.6% q/q SA nonannualized (6.6% q/q SAAR) after an upwardly revised 1.2% in Q4 (from 1% initially). That’s the fastest growth since Q1 of last year (chart 1). This further validates the PBOC’s decision to hold the previous day and in addition to yuan considerations.

A handful of indicators suggest that the quarter didn’t end very well for China, however, which may set up a soft entry into Q2 (charts 2, 3). Nominal retail sales were up by 0.3% m/m SA in October which was the strongest gain since last October but still fairly soft. Industrial production, however, slipped by -0.1% m/m for the weakest reading since last April.

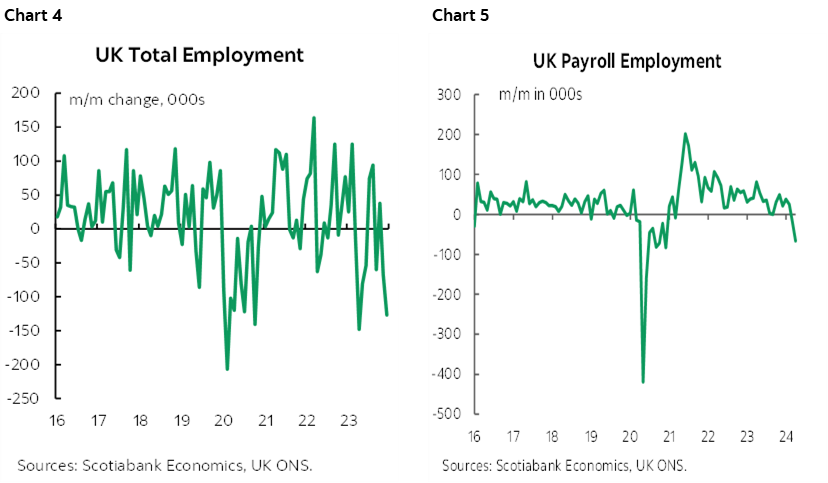

The UK job market weakened in February and March. Total employment fell by 127,000 m/m SA in February after a 67k drop the prior month with declines in three of the past four months (chart 4). Payroll employment—a fresher subset of total employment—fell by about 67k m/m SA in March following a drop of 18k the prior month (chart 5). The unemployment rate moved up to 4.2% from an upwardly revised 4% the prior month.

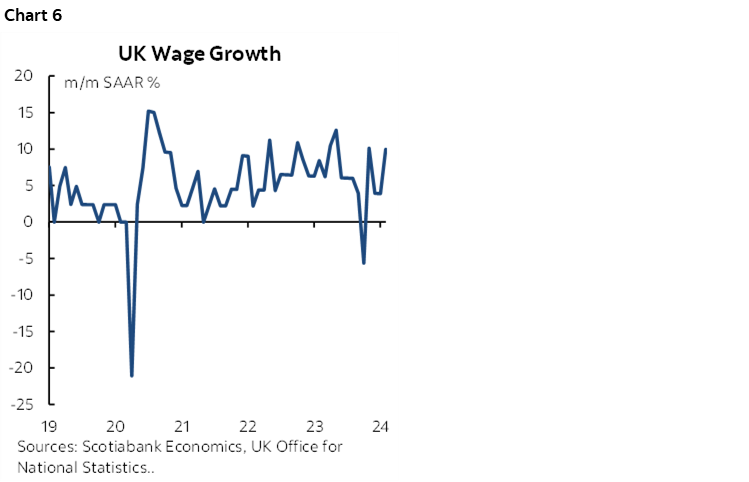

The rub likes in the fact that UK wage growth accelerated which is not welcome from an inflation risk standpoint. Wages ex-bonuses were up by 10% m/m SAAR for the biggest gain in three months (chart 6).

CANADA — INFLATION, MACKLEM AND THE BUDGET

It’s mostly about Canada into the North American session with a hat trick of key developments to look forward to:

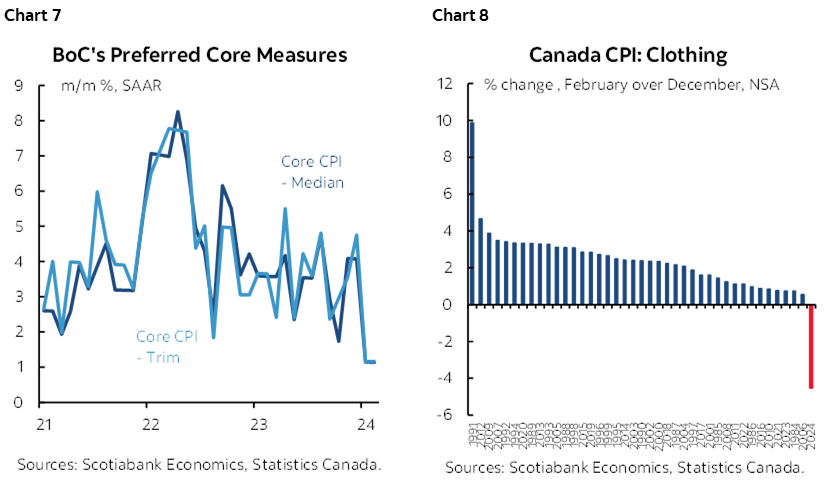

1. CPI (8:30amET): 0.7% m/m NSA and 3% y/y is expected. Key will be trimmed mean and weighted median in m/m SAAR terms after just a two-month soft patch (chart 7). See the Global Week Ahead here that laid out expectations and risks including emphasis upon a panoply of probably temporary idiosyncratic factors that dampened inflation in January and February and that have nothing to do with the effects of tighter monetary policy. The folks saying that inflation is just driven by shelter and everything else has weakened are ignoring the unusual array of factors that may be temporarily depressing multiple categories. One example of how unusual the movements have been is clothing that saw the biggest declines to start the year on record and that may have been driven by a milder and drier than normal winter (chart 8).

2. Governor Macklem (1:15pmET): He’s on a panel with Chair Powell at 1:15pmET at the IMF/World Bank Spring meetings. It will last for an hour and is going to be moderated by former Canadian Finance Minister Bill Morneau.

3. Federal Budget (>4pmET): It lands when Minister Freeland rises to speak just after 4pmET. Instant headlines will roll as soon as the media embargo lifts. Big spending, tax hikes, and deficits as far as the eye can see will be the focal points. It’s being confirmed in the local press that Minister Freeland will hike taxes on relatively upper income earners and corporations in some sectors. Among this government’s favourite targets have been grocers, telecoms, banks, and energy companies. Don’t hold your breath while hoping to see anything about productivity, investment and saving. This government’s focus remains squarely upon current spending on social programs.

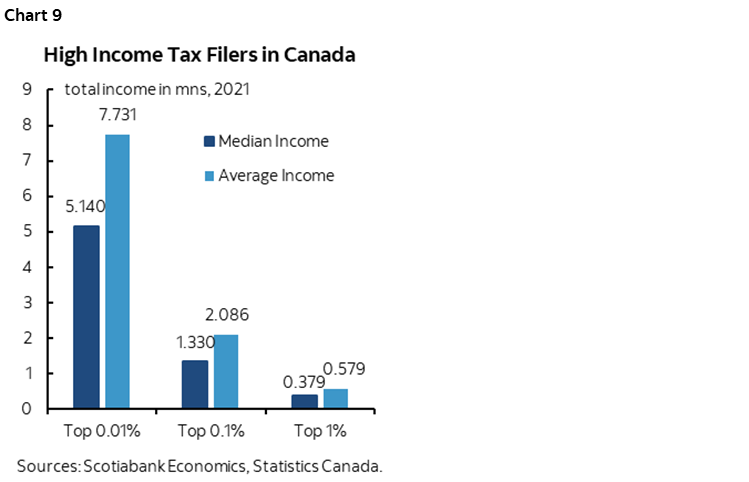

Anonymous sources are being quoted saying that the Budget will raise taxes on less than the top 1%. What that means is pretty vague in terms of income cut-offs and also in terms of what types of tax hikes are likely. The top 1% of earners in Canada had median income of C$378,900 and average income of $579,100 in 2021 using the latest figures from StatCan that were released late last year. The top 0.1% had median income of $1,329,600 and average income of $2,086,100. The top 0.01% of earners had median income of $5.14 million and average income of $7.73 million. Chart 9.

Canada also updates housing starts for March just ahead of CPI (8:15amET).

US — Fed, IP and Earnings

Fed watchers will have an eye on the same session at 1:15pmET when Chair Powell joins Macklem. US industrial production is also on tap (9:15amET).

US earnings will include 10 S&P-listed companies such as Morgan Stanley and BofA. BofA already beat this morning with Morgan Stanley ahead at 7:30amET.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.