BENEFITING FROM BROAD-BASED COMMODITY PRICE GAINS

- Saskatchewan’s oil production remained stubbornly weak in the first quarter of 2021, but we anticipate stronger gains as the year progresses.

- Other commodities and fiscal stimulus should bolster the recovery.

At the time of writing, Saskatchewan had the second-highest per-capita COVID-19 caseload of any province. We are encouraged by the downward trend in infection rates and rising pace of vaccination, though risks remain on this front.

Saskatchewan’s staple oil and gas industry has also gotten off to a somewhat soft start to the year. Crude production was down by 13.5% y/y ytd as of March 2021, though it did see a significant month-over-month improvement between February and March. While we expect output to rally as producers respond to stronger oil prices, the soft start should weigh on the annual growth rate—we assume a modest increase of about 3% this calendar year, in line with provincial government projections. Improving industry conditions to begin 2021 may have helped manufacturing and construction employment and hours, with robust homebuilding.

Yet the province’s other commodities still look set to contribute handsomely to the expansion this year. From January to April 2021, potash production was up over 11% versus the same period last year, and major producer Nutrien has revised H2-2021 potash output guidance by 500 kt, particularly at its Vanscoy mine. The Cigar Lake uranium mine restarted in April after two COVID-19-related work stoppages during the past year; output should ramp up more materially as we near 2022. Finally, prices for key crops wheat, canola, and soybeans are at multi-year highs—anchored by Chinese demand—and helped drive nominal Saskatchewan exports 15% higher than year-earlier levels as of April.

Eventual safe resumption of immigration flows is important for Saskatchewan just as in other provinces. For one, population outflows to other provinces had been steadily increasing before the pandemic, raising the need for an offset. As well, newcomers to Saskatchewan have historically had some of the highest employment rates among immigrants in Canada. Immigration to Saskatchewan has been helped by granting permanent resident status to workers already in the province, but overall admissions were still down 7% y/y ytd as of April 2021.

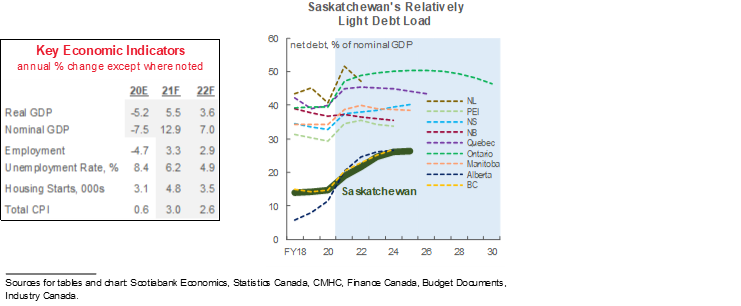

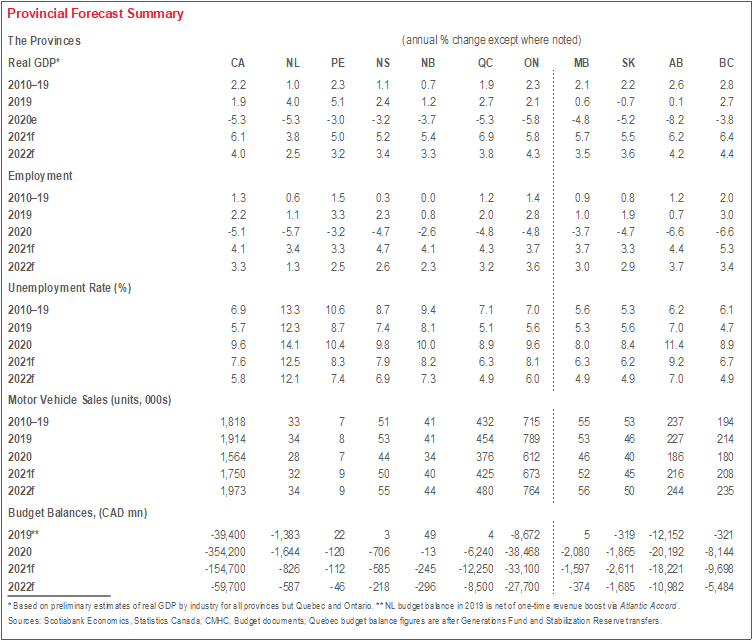

While Moody’s recently downgraded its rating of Saskatchewan’s debt from the vaunted AAA level, we still assess the province’s finances to be among the healthiest of any subnational jurisdiction in Canada. According to the latest government budget (read our take here), Saskatchewan’s net debt-to-GDP ratio is on track to be the lowest of any region through at least FY24. With low debt servicing costs relative to other provinces, this suggests debt levels are sustainable and leaves room for more fiscal policy intervention if needed. But more intervention may not be needed. Capital outlays across Crowns and government agencies are expected to rise by 12% and account for almost 4% of provincial output in FY22. Those figures are among the largest in Canada and should lend meaningful support to the recovery.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.