READY FOR LIFTOFF

- We still anticipate that Quebec’s economic growth will be among the strongest of any province this year.

- We expect the province to benefit from very strong US growth, a relatively modest third wave, and its own elevated level of fiscal stimulus.

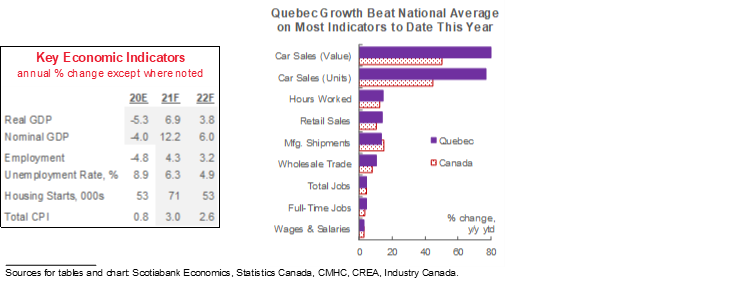

After carrying the largest absolute and per-capita COVID-19 caseloads in Canada throughout 2020 and in early 2021, Quebec’s third wave was modest relative to those in other provinces as well as its own prior rounds. At the time of writing, the province’s infection rate was the lowest outside of Atlantic Canada. That enabled relatively modest restrictions and earlier reopening than many other provinces, which already appear to have translated into stronger economic activity in Quebec than most elsewhere. Gains to date in full-time employment, hours worked, and wages and salaries in La Belle Province have outpaced those at the national level, as did real GDP growth in the first two months of the year.

Alongside the momentum that the province brought into 2021, we believe that Quebec is now poised for the strongest growth of any Canadian province this year. We now anticipate that Quebec’s growth will exceed that national average in both the first and second quarter of this year, with Canada likely to witness a slowdown in the latter period under the weight of third wave restrictions. With the strong gains we expect in the first quarter and the astronomical 60% (q/q ann.) in Q3 last year, that would be three out of the last four quarters in which Quebec’s growth outpaced the national average.

Upward revisions to our US forecast also contribute positively to our projection for Quebec exports; in our view, these broad demand impacts should outweigh potential downsides from “Buy American” policies. More specifically, Quebec’s export profile is oriented towards production of metals—notably aluminum and iron ore—and forest products, both of which appear to be benefiting from exceptionally strong prices and industrial sector demand and homebuilding. Aerospace—the province’s number one export product—took a significant hit last year as global air traffic plunged, but jumped higher in April .

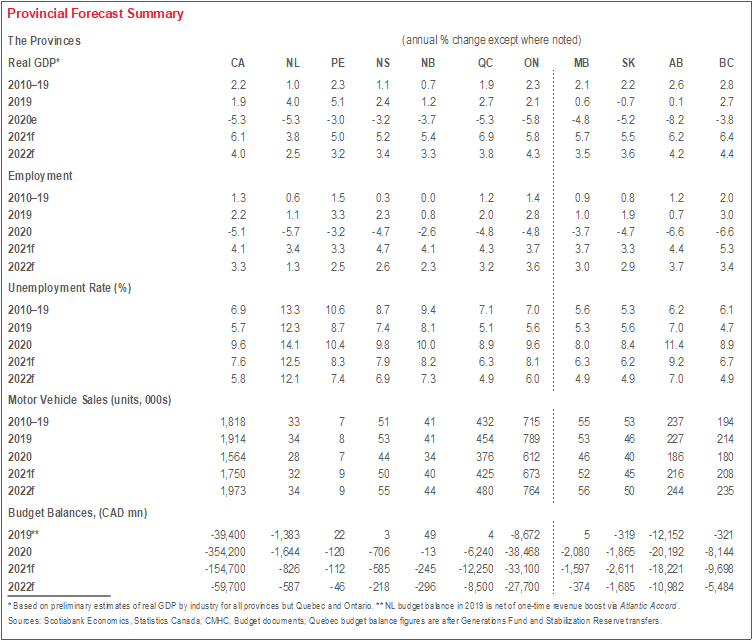

Quebec’s 2021 budget highlighted the impact of COVID-19 on the province’s fiscal position and the significant potential growth impact from provincial fiscal policy over the forecast period. Read our full analysis here. As a share of output, Quebec’s projected budget balances and net debt loads are towards the high end of the provincial spectrum. However, the government prudently targets a declining debt-to-GDP ratio beyond this fiscal year. The province also aims to increase capital outlays under the Quebec Infrastructure Plan through FY24; that includes projected boosts of 10% this fiscal year and 19% in FY23 that amount to total spending of over 3% of GDP over the two years.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.