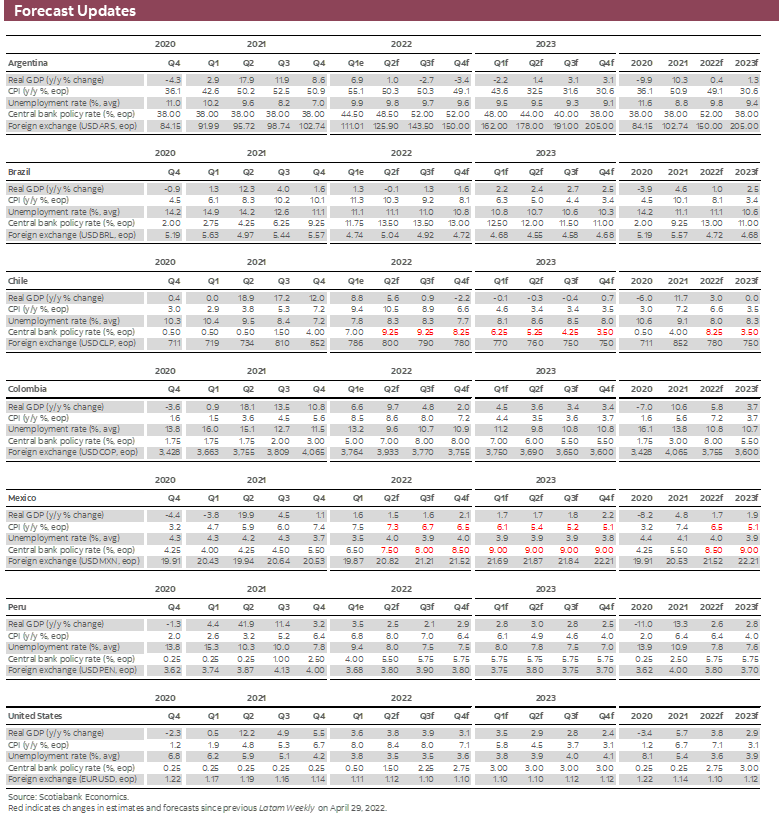

FORECAST UPDATES

- Increased financial market volatility in recent weeks, reflecting expectations of higher interest rates in advanced economies and the realization of geopolitical risk, adds uncertainty to the global economic outlook and poses new risks to Latam forecasts. Scotiabank teams in the region are assessing the implications and will be revising their projections in the week ahead. In the meantime, see their latest projections in the table below.

ECONOMIC OVERVIEW

- Russia’s invasion of Ukraine dominated global headlines in March and much of April. But with inflationary pressures showing few signs of abating—in part because of the commodity price shocks stemming from the invasion—inflation and the likely need for more aggressive policy rate increases in advanced economies once again dominate the headlines.

- Financial markets have not responded well to the prospect of higher rates. Meanwhile, the US dollar has appreciated against most currencies, including those of the Latam region.

- In the short-term, this conjuncture adds to the monetary policy challenges in the region, as currency depreciation could result in higher inflation being “imported” through exchange rate pass-through effects. Over the longer-term, the prospects for the Latam region may hinge on the resolution of the irresistible force-immovable object paradox represented by a potential inflationary wage-price spiral running headlong into central banks determined to return inflation to target.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period May 14–27 across the Pacific Alliance countries, plus their regional neighbours Argentina and Brazil.

Economic Overview: Immovable Objects and Irresistible Forces

James Haley, Special Advisor

416.607.0058

Scotiabank Economics

jim.haley@scotiabank.com

- Increases in inflation, and especially inflation expectations, are a source of considerable concern to central banks around the globe. A key worry is the possible wage-price spiral that higher expected inflation generates. Once embedded in wage bargaining, such a dynamic can resemble an irresistible force, one that is difficult to contain.

- But central banks with decades of inflation-targeting experience are loath to give up on their price stability commitments. Their determination to keep inflation well anchored at a “low, stable level” makes them implacable inflation fighters (even if they may have misjudged the persistence of price pressures). They could be immovable objects in the path to accelerating inflation.

- How this irresistible force-immovable object paradox plays out will determine global growth prospects over the months ahead. In the interim, the prospect of a clash between the two has led to increased financial market volatility and a marked appreciation of the US dollar. In the short-term, these effects add to the challenges faced by Latam central bankers.

SOMETHING HAS TO GIVE

Since the start of 2022, two stories have dominated headlines around the world—inflation and Russia’s war in Ukraine. The two are not wholly unrelated, of course, with global commodity prices—particularly for fertilizers, cereals and foodstuffs (sunflower oil)—spiking higher in anticipation of disruptions to Ukraine’s export capacity and the effects of sanctions on Russia. These price shocks have compounded COVID-19-related shocks to global supply chains, propagating a steady increase in price pressures.

As a result, inflation that just six or more months ago could be attributed to “temporary” factors is today a persistent and pressing problem. No country has been immune to these shocks, including those in the Latam region. And for central banks across the globe, the critical question is whether higher inflation becomes embedded in expectations that fuel rising wage pressures, which in turn could unleash a wage-price spiral.

Russia’s invasion of Ukraine temporarily crowded out coverage of inflation. But with a desultory Russian advance, Ukrainian counterattacks, and the emerging prospect of a potential military stalemate, inflation—what it implies for monetary policy and the effects of that on asset prices—once again dominates the news. Over the past couple of weeks global asset prices have been whiplashed by the realization of higher interest rates in advanced economies and the expectation of more rate hikes to come. Bond markets have sold off, and equity markets have experienced high volatility as they have progressively trended down.

To some extent, and with the benefit of hindsight, none of this should have come as an unmitigated surprise: interest rates were, after all, at historically low levels (as they have been for a decade or more in the wake of the global financial crisis); moreover, the global economy has been emerging from a once-in-a-century pandemic. Even without the price shock resulting from the Russian invasion of Ukraine, which arguably—though, even here, there is room for debate—was less foreseeable, interest rates would have reasonably been expected to rise. That said, there is no denying that inflation now looks more like a persistent plague, one that calls for a recalibration of the path of policy rates.

To be fair, the news on the inflation front is not all bad. US inflation was down slightly in April, as price pressures moderated from March. However, the improvement turned out to be less than consensus was expecting and, as Scotiabank’s Derek Holt has pointed out, US Core Inflation is Still Running Hot. The market did not react well. Expectations of higher interest rates have taken a toll on financial markets in recent weeks as the realization that the Fed can, in fact, raise rates, as well as lower them, sunk in. It remains to be seen how much of the market reaction is a by-product of spillover from the more esoteric assets. In such an environment, after all, valuations on a range of speculative assets—and the modern equivalent of tulip bulbs—would likely come under stress.

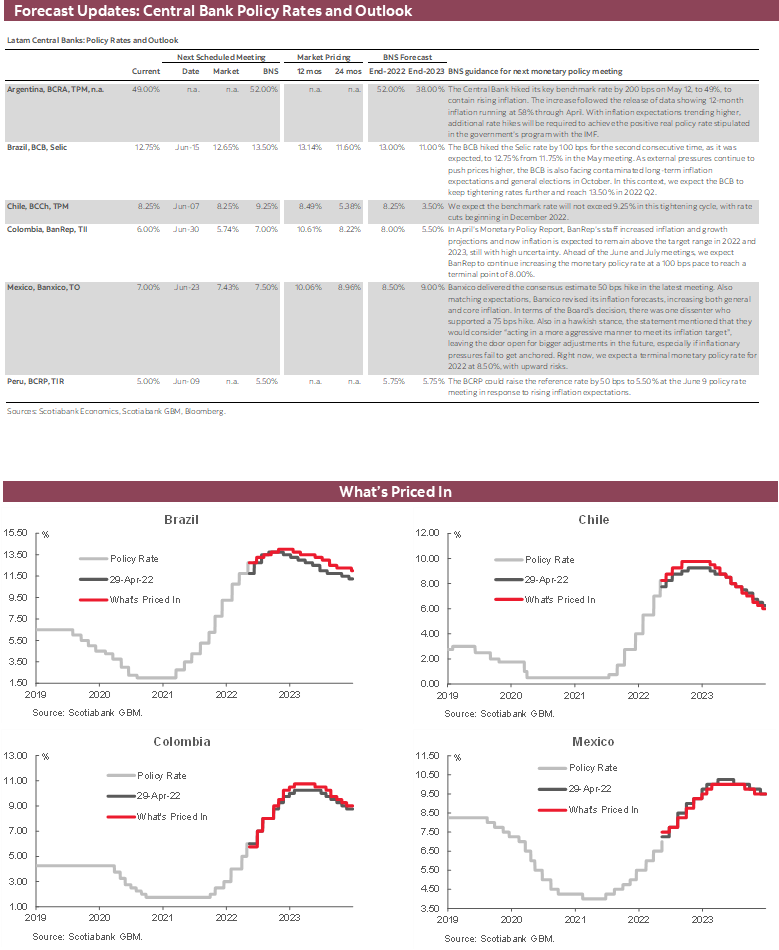

The inflation outlook is little better in the Latam region. In Mexico, inflation continued to trend higher April, rising from 7.45% y/y to 7.68%. While this was slightly below consensus, core inflation jumped from 6.78% y/y in March to 7.22% in April. Those developments undoubtedly weighed heavily in Banxico’s decision to raise its policy rate by 50 bps on May 12, with what our economists in Mexico view as hawkish guidance. The central bank in Peru likewise hiked its policy rate 50 bps on May 12, in response to inflation that rose to almost 8% y/y in April and an increase in 12-month ahead inflation expectations to 4.62%, up from 4.39% in March, and well above the BCRP’s inflation target. Similarly, in Chile, the BCCh raised its policy rate 125 bps to 8.25%, surprising the expectations of both the market and Scotiabank’s team in Santiago. As our experts there have pointed out, two factors likely influenced the central bank’s decision: the depreciation of the Chilean peso against the dollar, which could lead to higher inflation through exchange rate pass-through effects, and inflation itself. In Colombia, meanwhile, inflation soared in April rising by a whopping 1.25% m/m, as annual inflation increased to 9.23%. Core inflation also increased—from 5.31% y/y in March to 5.95% in April—to the highest level since September 2016.

These inflation trends could prove problematic in the months ahead. This is because, to the extent that high core inflation becomes incorporated into wage bargaining, increases in expected inflation will lead to higher wage demands. And since higher wages feed through to product and services prices, this process could generate higher inflation that eventually leads to still-higher wage demands, resulting in yet higher wage increases, and so on. Note the use of the conditional tense in the preceding sentence. It is key.

Higher inflation that leads to rising wage demands can trigger a wage-price spiral reminiscent of past decades. However, such dynamics do not necessarily lead to a replay of the 1970s, even if they may appear at times to be irresistible forces. The difference between then and now is that central banks both in the Latam region and the advanced countries have well-defined inflation-targeting frameworks that anchor policy targets and guide decision-making. To the extent that these central banks remain steadfastly loyal to their low, stable inflation commitments, there is no reason to believe that we are on the cusp of ever-accelerating inflation. That, in a nutshell, is the wholly reasonable basis of Scotiabank’s (and other) projections showing inflation returning to target over the medium-term, even if the timing of that return has been pushed out owing to supply and commodity price shocks.

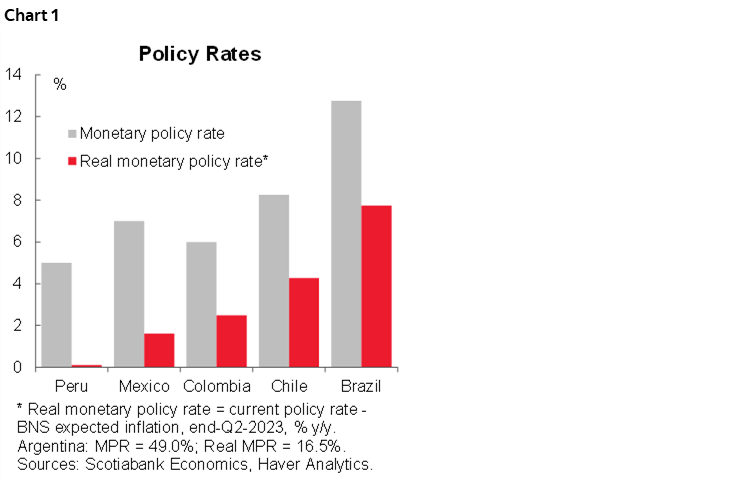

But if central banks in the Latam region and elsewhere remain immovable objects in the path of an irresistible force pushing higher inflation, we have a problem. The paradox is only resolved through one of two possible outcomes: either inflation expectations and wage demands are ratcheted down, in which case inflation returns to target, or higher wage demands and product pricing that are inconsistent with the monetary anchor ultimately lead to lower growth and increasingly high unemployment, which eventually elicits a moderation in wage demands and narrower pricing margins as stores see inventories of unsold goods rise. The first resolution entails a relatively painless process of adjustment. The second is far more disruptive; it is why central banks around the globe have sought to anchor inflation expectations. And as noted in the last edition of the Latam Charts, Latam central banks have been proactive in this regard (chart 1); advanced country central banks somewhat less so.

Recent rate hikes by the Bank of England, the Bank of Canada, and the Fed, together with the intimations of a likely rate increase by the ECB, and the articulation of a resolve to do more—to do “whatever it takes,” to borrow a phrase—to preserve price stability could keep inflation expectations firmly anchored. That would, of course, be the best outcome. But in a world of repeated supply shocks and global commodity price spikes, the expectation of that outcome may well be Panglossian.

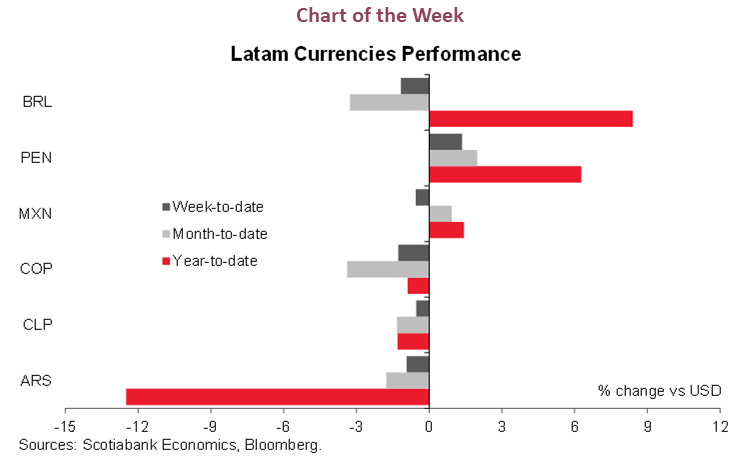

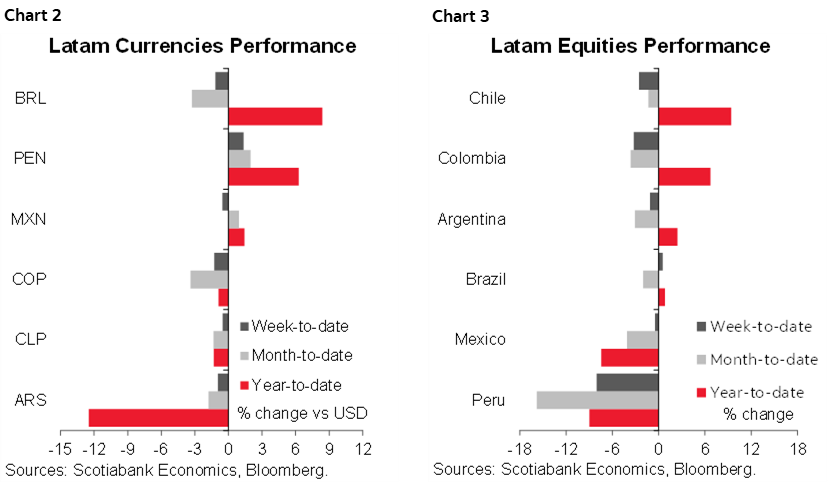

How the irresistible force-immovable object paradox will be resolved is, for now, uncertain. That will be decided in the coming months. A more immediate concern for the region’s central bankers is the US dollar, which has appreciated against most currencies around the globe, including those of Latam countries. Through much of 2022, their currencies had held their own (and even appreciated) against the dollar, as proactive policy rate increases provided a favourable interest rate spread. That stability has looked far less certain in the last few weeks in the wake of the Fed’s more hawkish messaging on interest rates. As expectations of US rates have risen, and geopolitical risks materialized —shifting global investor risk appetite—regional currencies have depreciated (chart 2). In the past week, all but Peru’s PEN has depreciated against the dollar. Local equities markets have likewise sold off, as these factors have been priced in (chart 3). At the same time, the region’s electoral schedule and idiosyncratic political uncertainties have probably played a role in the re-pricing of assets.

For Latam central bankers, a sustained period of currency depreciation would greatly complicate the return to inflation targets. This is because currency weakening would add to inflation through the pass-through effects noted above. In such a scenario, central bankers would have to weigh the potential output losses of an earlier return to target against the longer-term costs of weakened credibility associated with a longer path back. This output-inflation tradeoff is not entirely under their control, however.

In this respect, the tradeoffs that Latam central banks confront in the weeks ahead will be greatly influenced by the decisions made by the Fed and other advanced country central banks in the resolution of the irresistible force-immovable object paradox.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Central Bank Speeds Up Stimulus Withdrawal amid Rising Inflation

Jorge Selaive, Head Economist, Chile

+56.2.2619.5435 (Chile)

jorge.selaive@scotiabank.cl

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

Waldo Riveras, Senior Economist

+56.2.2619.5465 (Chile)

waldo.riveras@scotiabank.cl

The daily number of confirmed COVID-19 cases has started to increase in recent days. The test positivity rate rose to 6%. For now, however, occupancy rates of ICU beds and COVID-19-related death rates are decreasing. Meanwhile, the vaccination campaign has reached 94.4% of the eligible population. The rollout of booster (third) doses continues—reaching 14.1 million people—and the new booster dose (fourth) is in progress—with 4.8 million people covered. Overall, mobility has continued to increase in May, which will support the economic activity, mainly services.

In light of the increase in COVID-19-related cases, the government announced that the Metropolitan Region (52 communes) will go back to the medium health impact stage, starting Thursday, May 12. In total, 95 communes in the country will change from low to medium impact.

ECONOMIC RECOVERY LED BY STABILIZATION OF GOODS PRODUCTION, WHILE ANNUAL INFLATION INCREASES

On Monday, May 2, the central bank (BCCh) released data on monthly GDP for March, which expanded 7.2% y/y, above market expectations (Bloomberg: 6.2%) and in line with Scotiabank’s estimate (7.0%). Imacec grew 1.6% m/m (seasonally adjusted), recouping part of the contraction in economic activity observed since December, largely owing to faster growth of services and a stabilization in goods production.

With these figures, GDP nevertheless fell 0.4% q/q in Q1-2022, reflecting convergence to trend levels of GDP. However, the decline in quarterly growth raises the risk of a moderate technical recession should Q2-2022 also turn out to be negative. A technical recession would be consistent with our base case scenario, in which the second half of the year is crucial to our higher-than-consensus estimate of annual GDP growth in 2022 of 3% (chart 1). Risks to our projection include external factors linked to the global slowdown as well as local factors coming from heightened political uncertainty.

On Friday, May 6, the statistical agency (INE) released the April CPI inflation, which rose 1.4% m/m (10.5% y/y), above both market and our expectations. These levels of inflation generate significant second-round effects that give rise to inflationary persistence that is not easy to contain. In this context, after two consecutive monthly inflationary surprises, we have revised our inflation scenario for 2022 and 2023, projecting annual inflation in 2022 at 8.4% and in 2023 at 3.7% (previously 6.6% and 3.5%, respectively).

GOVERNMENT REVISES ITS FORECAST OF 2022 GDP GROWTH, AND INCREASED ITS PROJECTION FOR INFLATION

In this context, on Tuesday, May 3, the Ministry of Finance (MoF) published its quarterly Public Finance report for the first quarter of 2022. A key change from the last report was the downward revision in the GDP projection for 2022, which decreased from 3.5% in December to 1.5%. According to the MoF, the projection is consistent with a -1.0% contraction in domestic demand in 2022 (from +2.6%). The MoF also revised its CPI inflation forecast upwards, from 6.5% to 8.9% on average for 2022.

A ROLLER-COASTER MONETARY POLICY RATE BECOMES MORE LIKELY

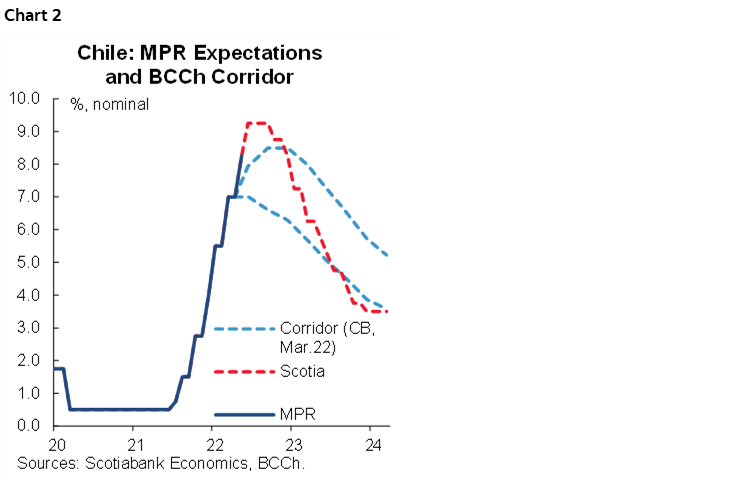

On Thursday, May 5, the BCCh hiked the monetary policy rate (MPR) by 125 basis points (bps), to 8.25%, surprising both market and our expectations. The BCCh statement makes for a hawkish read, particularly in pointing out that all the recent international and national data are inflationary and the discussion of the Board’s decision to place the policy rate in the upper part of the rate corridor revealed a few weeks ago in the March Monetary Policy Report. The statement also reveals concern with respect to the recent nominal depreciation of the Chilean peso (CLP), which contrasts with the fall in the real exchange rate and the limited multilateral depreciation of the CLP.

We discern a central bank concerned about local inflation and inflation expectations, and we reassess the terminal rate of this policy cycle towards 9.25% (chart 2). After being one of the most aggressive central banks in the recent tightening cycle, the BCCh will be forced to unwind the withdrawal of monetary stimulus quickly and aggressively after the first signs of disinflation. Special attention should be paid to the CLP and monthly CPI as monetary policy will no longer have credible forward guidance. The BCCh has turned to reacting to short-run data, minimizing its usual forward-looking behaviour.

A LOOK AHEAD

Lastly, in the fortnight ahead, the central bank will release the Q1-2022 GDP growth, on Wednesday, May 18, and will publish the minutes of the last monetary policy meeting on Friday, May 20.

Colombia—Economic Policy Priorities for the Next President Range from the Urgent to the Important

Sergio Olarte, Head Economist, Colombia

+57.1.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Maria (Tatiana) Mejía, Economist

+57.1.745.6300 (Colombia)

maria1.mejia@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.1.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

In a couple of weeks, Colombia will hold elections to choose the next president for a four-year term. Recent voter intention surveys point to the leftist candidate, Gustavo Petro, and the centre-right candidate, Federico Gutierrez, as the two potential contenders in the runoff election. However, polls also revealed that the undecided share of the population remains high, and it is difficult to predict who the new president at the Casa de Nariño will be. A first milestone on the election schedule was passed with the recent Congressional election, which proceeded smoothly. In fact, the main credit rating agencies highlighted that Colombia has well-established institutions that will be preserved, which reduces the probability of sudden changes in economic policy. This stability is an important feature given that the next president will have to deal with a range of important challenges requiring structural changes to economic policies, in addition to the most urgent issue—increasingly high inflation.

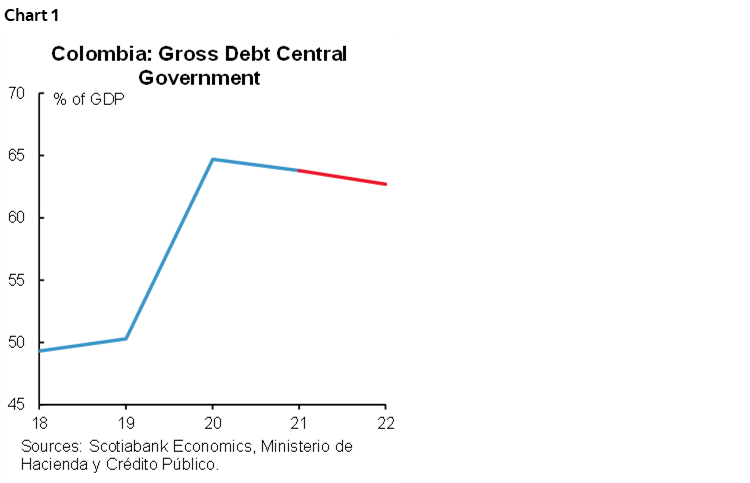

There is a common factor in the political agenda for all the candidates and it is fiscal sustainability. Prior to the pandemic, economic analyses of Colombia typically found a weak and rigid fiscal structure with low income taxes as percentage of GDP (17% of GDP, compared to the OECD average of around 35%), and a highly inflexible budget, with about 80% of budget spending non-discretionary. During the pandemic shock, the fiscal rule was suspended and the debt-to-GDP ratio increased from 50% of GDP to 65% (chart 1). In 2021, a fiscal reform package was approved, reversing some tax reductions to the corporate sector, but this reform was far from being the structural reform that is needed. As a result, the next president will not only have less fiscal space in which to operate, but also a new fiscal rule, introduced in 2022, which targets a reduction in the net structural primary balance to 1.4% of GDP in 2023, from the current estimate of 2.6% of GDP.

In this regard, tax reform is likely to be the first task of the next government. The leftist candidate, Gustavo Petro, proposes dropping all tax exemptions and maintaining the consumer staple basket without VAT. He also wants to increase the personal tax base. According to his calculations, these changes would increase tax collections by around 5.5% of GDP, which would constitute an unprecedented amount compared with traditional tax reforms in Colombia (0.5% of GDP). Uncertainty remains whether fiscal reforms would be the first priority of Federico Gutierrez, though some proposals that we have heard include reducing corporate taxes, increasing taxes to wealthy people, further implementing electronic bills, reducing some tax exceptions (no clarity here regarding which sectors), and raising regional tax collection. A similar approach is proposed by Sergio Fajardo, with emphasis on green taxes. The only candidate who, for now, downplays fiscal reform is Rodolfo Hernandez, whose main priority is fighting corruption; he is considering reducing bureaucratic burdens to limit the scope for corruption. He is considering lowering the VAT to 10% and eliminating the tax on financial transactions.

Regardless of the election outcome, the market will find that the next president is committed to fiscal responsibility, aiming to achieve lower debt as a percentage of GDP. All of that should send a positive message with respect to the public debt market pricing. In any case, it is important to recall that the eventual fiscal reform package must be approved by Congress, which make us think that a candidate with stronger negotiation skills and a pragmatic approach will end up achieving more positive outcomes.

The second main issue on the economic policy agenda is Pension Reform. Currently, Colombia not only has a highly regressive system, but also a very inefficient system. In fact, only about 25% of the elderly population has a pension. In this respect, any pension reform would impact financial markets if the transition were carried out suddenly. It is noteworthy, therefore, that none of the candidates are looking to change special regimes, which usually imply higher pension subsidies to politicians, teachers, and the military. Moreover, none expect to change pension parameters, such as the eligibility age, nor propose significant reductions on regressive subsidies to wealthy people.

The most ambitious pension reform proposals come, again, from Gustavo Petro, who advocates a mandatory contribution to the public system (which usually only has liabilities) for people of up to 4 monthly minimum salaries (more than the 80% of pensioners). This proposal would reduce flows of private pension funds, which eventually will affect their Assets Under Management, whose principal investment is in public debt (since they have 28% of total local debt outstanding). Given the potential impact on asset markets, this possible reform should be monitored closely. Another proposal from Petro is to guarantee a universal pension of at least half the minimum salary, which would have a future fiscal cost (which bowing to the lack of specifics cannot be calculated).

The other candidates have somewhat less ambitious pension reform plans. Federico Gutierrez is not looking to change the current pension system. Instead, he would concentrate his efforts in subsidizing vulnerable people (a third of the minimum salary) and promote some skill programs for the aged population. Sergio Fajardo’s proposal mirrors Gustavo Petro’s, but with a lower mandatory contribution to the public system (up to two monthly minimum wages), which could represent a liquidity shock to private pension funds. Fajardo’s proposal also includes some solidarity pillars for vulnerable populations (payment of a half monthly minimum salary). Rodolfo Hernández’s plan includes a competing system putting the public and the private pension funds on the same playing field, which would likely increase the fiscal burden to cover current pensions but could also stimulate capital markets.

All in all, while pension reform will feature prominently on the policy agenda, its path forward is difficult since it must pass through congress and in Colombia’s history it is a fraught topic for politicians. In part, this is because, depending on the reform, it would have an impact on the capital market liquidity, but also would imply a potential fiscal burden if current regressive subsidies to wealthy people are not moderated.

The picture for the next president is far from rosy. The post-pandemic recovery has seen increased social demands as monetary poverty has risen, and current inflation is adding additional pressure. We expect fiscal issues to be at the top of the new president’s “to do” list. All in all, if the eventual fiscal reforms contribute to fiscal sustainability in the medium term, it would be credit positive. But it will also be important to see how the next president deals with current social demands.

Mexico—The (Public Finance) Costs of Fighting Inflation

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

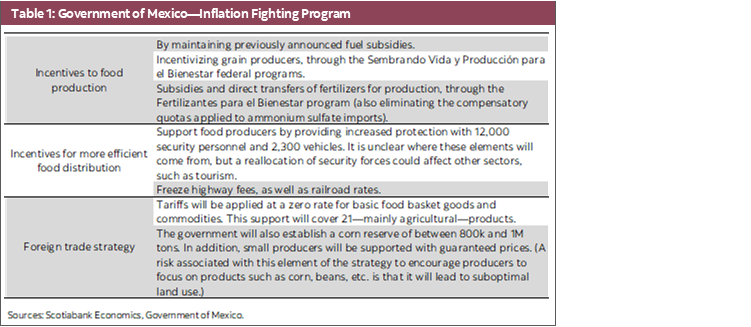

On May 4, the government announced a package of measures to reduce inflationary pressures in key items of the consumption basket. Some details of the package are not entirely clear, making it difficult to estimate the impact of the program accurately. However, most of the measures to reduce prices, or at least curb price increases, are likely to have a cost either to public finances or the private sector. The government estimates that the program, which is scheduled to last for six months, will help contain pressures on goods that contributed to 190 basis points of inflation in March, with a cost of 1.4 percentage points of GDP to the government.

The aim is to contribute to reducing inflation through three main channels (table 1).

In addition, an agreement was reached with Telmex and América Móvil, which decided to maintain their prices during 2022.

While the measures aimed at containing price pressures could temporarily reduce inflation, we believe global price shocks will be long-lasting as supply chain disruptions are estimated to potentially extend into 2024. The time-bound nature of the program could mean that it provides only an ephemeral break in inflationary pressures. Furthermore, there is a risk that the Ukraine conflict will further escalate, leading to a range of impacts across a broader set of industries. With this, and considering the impact that these measures could have on public finances (higher spending and lower revenues) above the estimates already included in the 2022 Economic Package, such as the 4% growth assumption, and the average cetes/repo rate of 5%, we consider a steepening of the curve as a possible impact of the package. In this respect, a temporary respite from inflation could come at a longer-term cost in terms of an adverse impact on public finances. And while it is difficult to discern the impact of the package and the movements in global markets, over the last few days we have observed a widening of Mexico’s CDS, and a steepening of the curve, which is consistent with our reading that this package could lead to a temporary reduction in the short-term inflation premium, but an increase in the credit premium of Mexican debt, owing to the fiscal cost of these measures.

Peru—Finding Growth amidst Inflation and Political Noise

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

Mario Guerrero, Deputy Head Economist

+51.1.211.6000 Ext. 16557 (Peru)

mario.guerrero@scotiabank.com.pe

Inflation continues to rage, rising to 8.0% for the 12-month period to April. Price pressures were broad-based in April, with increases to over 77% of the 586 products that make up the consumer index. Furthermore, wholesale inflation, linked to production costs, jumped from 11.6% in March to 13.1% in April, suggesting that still-higher inflation is likely before it begins to correct. For May, we expect yearly inflation to be in the vicinity of 8.5%. Although the government announced tax benefits for staples including chicken, eggs, milk, meat, wheat and sugar starting in May, we doubt their effectiveness. Given the increase in inflation, it came as no surprise that the BCRP raised its reference rate by 50 bps to 5.0% on Thursday, May 12. We expect another 50 bps increase in June.

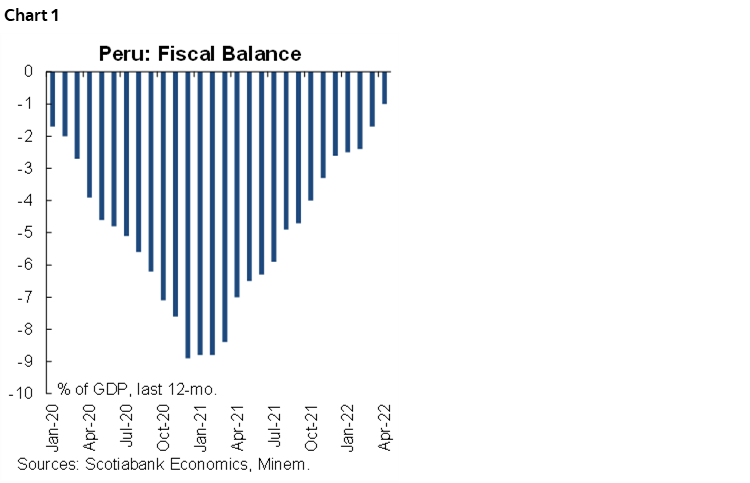

According to figures released by the BCRP, Peru’s 12-month deficit fell to an astonishingly low 1.0% of GDP in April (chart 1). Peru has thus already returned to the fiscal rule. The results reflect a very strong income tax season in the March–April income tax season. In April, tax revenue rose 30% y/y, led by income tax, up 66%. April could, however, represent the trough for the year, as the deficit begins to slowly creep back up now that the main tax season is over. Even so, Peru’s fiscal situation is extremely comfortable and helps reduce the need for debt financing at a time when interest rates are rising.

First-quarter GDP growth figures are scheduled to be released on May 15. We expect 3.5% y/y aggregate GDP growth, based on January–February monthly figures. Growth has held up well in the quarter, led by hospitality, restaurant, school supplies, and transportation expenditure, as mobility restrictions were lifted and schools re-opened. Tourism also picked up, rising nearly 700% y/y over January–April according to figures provided by the Minister of Trade and Tourism, Roberto Sánchez. The border with Chile was re-opened in May, which could stimulate tourism and trade further. And yet, it will become increasingly difficult to sustain +3% growth over time, as the y/y measure loses the benefit of base-effect comparisons with mobility restrictions early last year. Add to this rising costs, higher interest rates, and global metal markets that are beginning to correct, and the environment for growth becomes even more difficult. Not to mention continuing political turbulence.

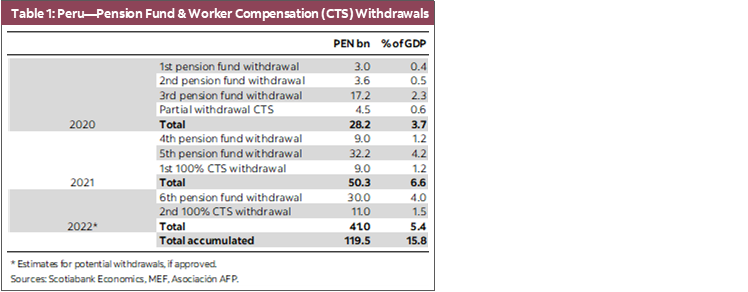

One thing that is likely to help support growth is the promise of a new round of pension fund withdrawals and access to worker compensation accounts. Congress authorized a new withdrawal from pension funds (AFPs) for up to USD 4,800 (PEN 18,400). The Executive must soon decide whether or not to veto the bill. It is not clear if it will do so, however, as a veto would probably be overridden by Congress. If that is the case, it is possible that withdrawals would start as soon as June. Congress also authorized full access to worker compensation accounts (Compensación por Tiempo de Servicios, CTS) from now until December 2023. Peru established the CTS system to compensate for job loss, as the country has no unemployment benefits.

Withdrawals from pension funds and worker compensation accounts, if drawn in full, could provide households with about USD40 bn in funds, or over 5% of GDP. We estimate that in the past anywhere between a third and a half of withdrawals were channeled into greater consumption, with the remainder used to bolster savings or reduce debt (table 1).

These measures are not without cost, however, as workers will have lower resources available upon retirement or if unemployed. The Bank Superintendent estimates that the new pension fund withdrawal could amount to between 20% and 25% of Assets Under Management (AUM). This could lead the BCRP to implement measures to provide AFPs with liquidity, such as repos sovereign bond facilities.

The government also announced a 10% increase in the minimum wage, from PEN 930 to PEN 1,025 (USD 267). Although the scope of this measure is limited (12% of the formal labour market), it should support consumption. Note that these measures have not been strong drivers of inflation in the past, but are certainly an additional factor in today’s already-inflationary environment.

The week has been particularly active in political events. Congress finally determined the new make-up of the Constitutional Court (Tribunal Constitucional), Peru’s equivalent to the Supreme Court. (The tenure of six Court members out of seven in total had expired, in some cases for over a year.) With so many members being replaced it is difficult to assess how the new Court will rule. However, the general impression seems to be that the Court is conservative on social issues (such as gender issues), but also broadly against State involvement in markets.

Meanwhile, ten members of Congress from Perú Libre resigned from the government party this week. These members, all of whom are closer to President Castillo than to the more radical leadership of Perú Libre, will mostly likely join the Partido Magisterial y Popular, a new party that is being formed to participate in the October 2 regional elections. The division leaves the Cerrón-controlled Perú Libre with 23 members in Congress.

Poverty figures for 2021 were released and came in mid-way between relief and worrisome. Relief because the 25.9% poverty figure was a sharp improvement over the rise to 30.1% in COVID-19-year 2020. But also worrisome because it remains well off the pre-COVID-19 level of 20.2% in 2019. Poverty should continue declining in 2022, based on jobs growth, but it may take another year or two for it to return to 20% or lower.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.