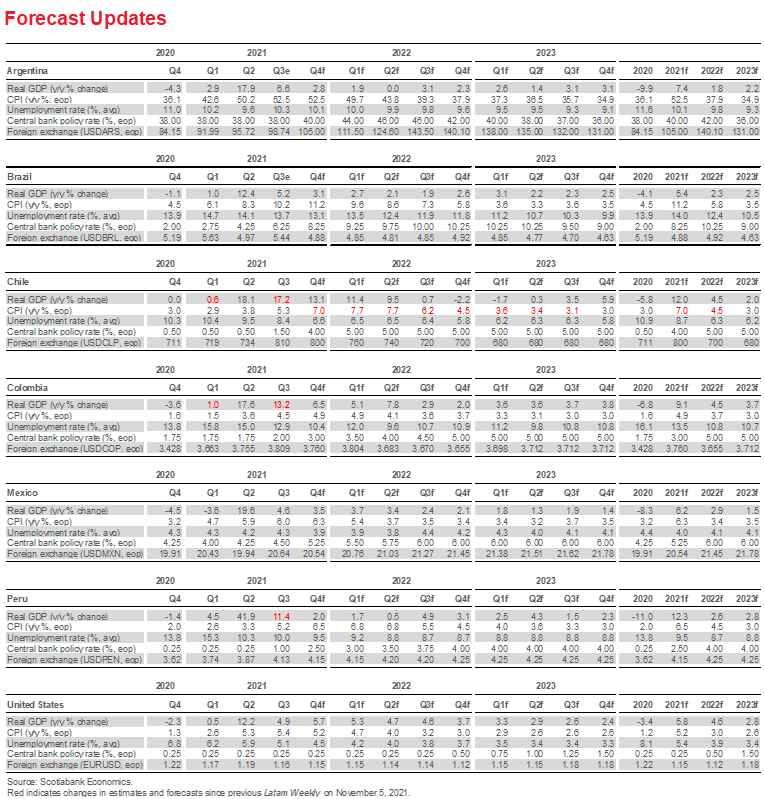

FORECAST UPDATES

- Stronger growth numbers have led Scotiabank’s country teams in Chile, Colombia and Peru to raise their GDP forecasts. In Chile, the robust recovery and higher inflation readings have also prompted our experts in Santiago to tweak their inflation outlook.

ECONOMIC OVERVIEW

- Higher inflation and the possibility that advanced country central banks may have to respond more aggressively than is currently expected have focused attention on financial stability.

- Recent central bank financial stability reports highlight the risks to sudden shifts in investor risk appetite and the effects of ample global liquidity on risk taking and the search for yield. Heightened leverage in the non-financial sector could fuel deep “tail risk” output contractions.

- While there is little evidence to imminent threats to financial stability in the Latam region, the threat of external shocks underscores the importance of strong macroeconomic policy frameworks. Looking ahead, debate may focus on the possible use of macroprudential tools that would assist central banks to better manage the policy trade-offs they face.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

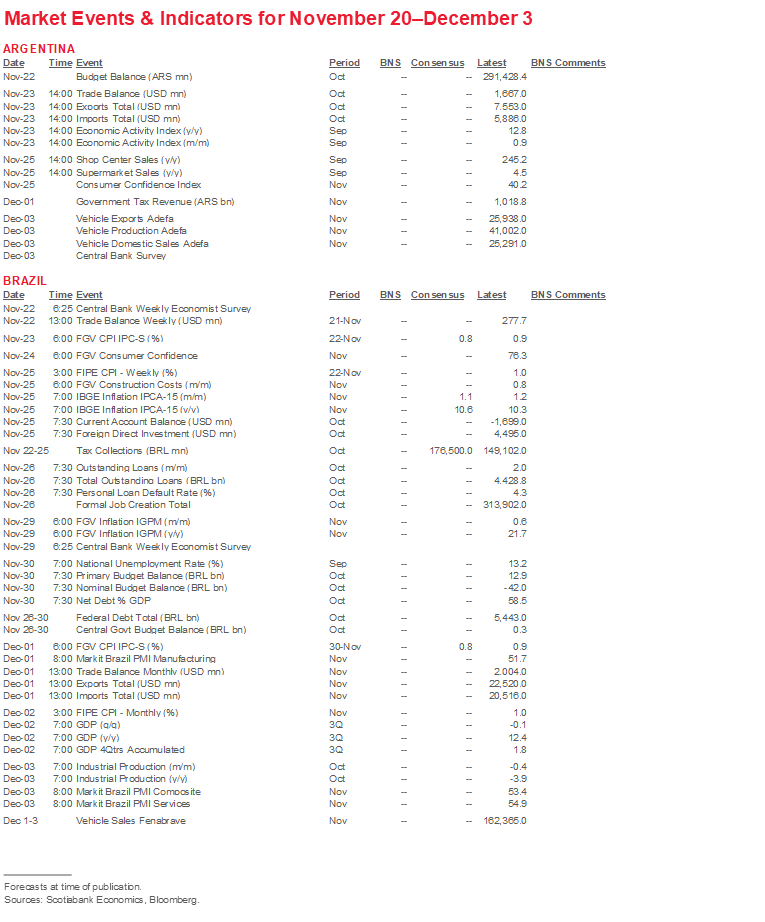

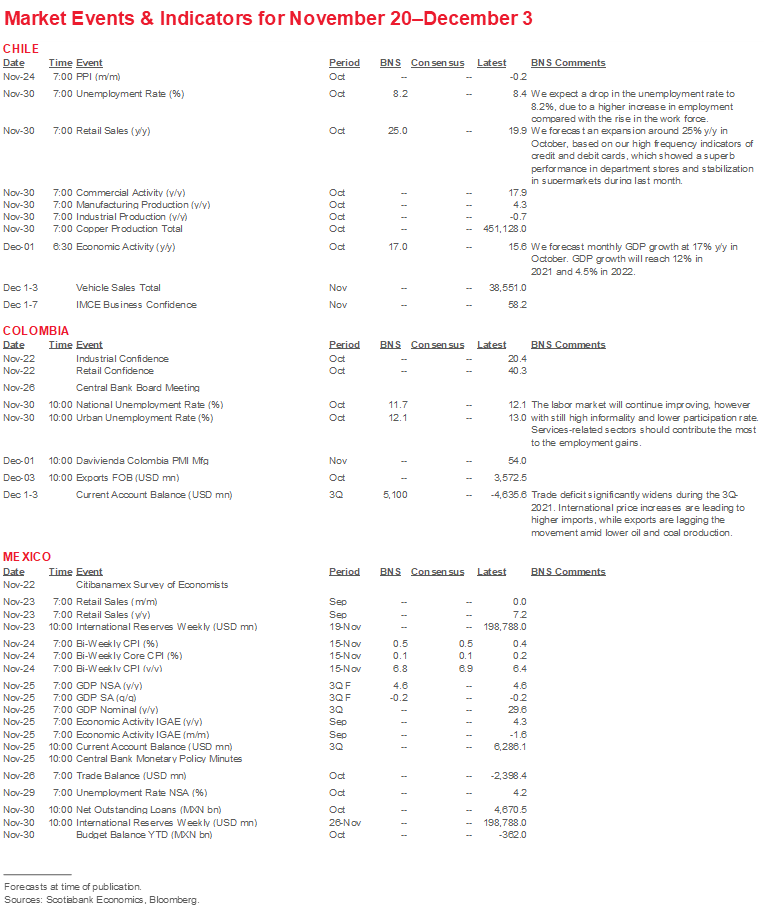

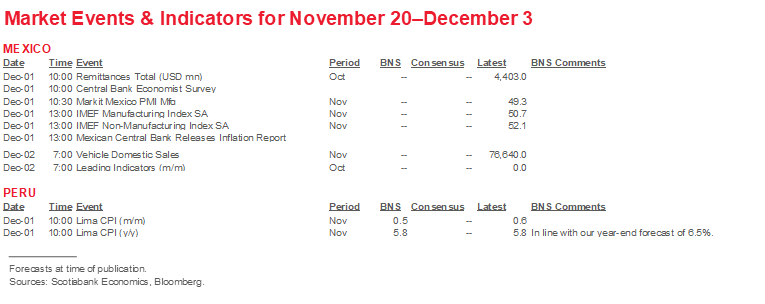

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period November 20–December 3 across the Pacific Alliance countries, plus their regional neighbours Argentina and Brazil.

Economic Overview: Focussing on Financial Stability

James Haley, Special Advisor

416.607.0058

Scotiabank Economics

jim.haley@scotiabank.com

- Recent central bank financial stability reports have focused on possible risks from shifts in investor risk appetite and more aggressive tightening in advanced economies.

- These concerns complicate decision-making with respect to the pace and timing of tightening and may lead to trade-offs in policy objectives.

- There is little evidence of nascent financial stability risks in Latam countries, but they remain exposed to external financial shocks.

- Strong macroeconomic policy frameworks help guard against these shocks. Going forward, attention could turn to the proactive use of macroprudential policies to assist central banks manage policy trade-offs.

INFLATION, FINANCIAL STABILITY AND POLICY TRADE-OFFS

The recent publication of financial stability reports by advanced country central banks as well as their counterparts in the Latam region has focused attention on financial stability. A central theme of these reports is the risk of a sudden re-pricing of assets resulting from a shift in investor risk appetite. Such a shift could propagate balance sheet shocks that are amplified by high levels of leverage across the non-financial sector, leading to lower investment and consumption and a prolonged period of lower growth as balance sheets are repaired.

Fortunately, as recent financial stability reports note, banking systems are generally well positioned to absorb these shocks, with higher capital and liquidity buffers; stress tests suggest, meanwhile, that banks have sufficient capital to withstand various adverse scenarios.

Nevertheless, given the current conjuncture, the attention placed on financial stability is appropriate. It has become increasingly clear that, as global inflation has picked up, the current extraordinarily expansionary stance of monetary policy cannot be maintained indefinitely. And while this does not necessarily imply that an immediate or an abrupt shift from expansionary to contractionary financial conditions is in the offing, some adjustment to the current stance of policies is warranted, if only because higher unexpected inflation drives real interest rates further into negative territory, adding to the stimulus impulse in the economy. Financial conditions may remain expansionary, just less so than is currently the case. But that adjustment implies a change, however gradual, in the global low interest rate environment that has prevailed for the past decade that animates financial stability concerns.

Latam central banks are leading this recalibration. Key policy rates have already been raised across the region; further increases are on the way. That said, the path towards the re-normalization of monetary policy conditions is clouded by considerable uncertainty. Disruptions to global supply chains and logistical bottlenecks raise the question of whether current price pressures are a temporary problem, or could become more persistent, should they become embedded in expectations and wage formation.

For central bankers grappling with the challenge of rebalancing monetary policy, financial stability concerns exacerbate the uncertainties they face. This is because past low interest rates may have fuelled excessive risk-taking that potentially poses a threat to financial stability. That channel could, for example, account for the emergence of asset price bubbles in some markets. At the same time, while extraordinary monetary (and fiscal) policies have insulated economies from the COVID-19 shock, they have also facilitated an increase in leverage in both advanced and emerging market economies.

Central banks may thus face an inter-temporal trade-off between the need to contain inflation and the risk that higher interest rates could imperil growth and employment objectives. On the one hand, an approach to rebalancing monetary conditions that is too gradual may result in a ratcheting up of inflation expectations and growing macroeconomic imbalances with adverse implications for long-term growth. In this scenario, central banks that have fallen behind the tightening cycle may inadvertently generate a future "hard landing" as they catch up to deliver on their price stability commitments. On the other hand, too rapid a rebalancing to contain price pressures might slow the recovery or trigger deleveraging that leads to large output losses. In this scenario, price stability objectives would be achieved at the cost of higher unemployment and financial disruption in the near term.

In part, this trade-off reflects the global build-up of non-financial sector debts since the 2008-10 financial crisis. IMF data shows, for example, that non-financial sector debt increased from 138 percent to 152 percent of GDP over the decade to the end of 2019. The COVID-19 pandemic has added to non-financial sector debt loads: economic activity collapsed as public health lockdowns took effect, resulting in the loss of income and the accumulation of additional debt to avoid bankruptcy and sustain consumption.

This effect does not mean that the extraordinary fiscal and monetary measures introduced to fight the pandemic were unnecessary or undesirable. Without them the plight of the most vulnerable would have been even greater and the economic and financial dislocation more severe. Delinquency rates would have soared and bankruptcies would have likely led to the loss of firm-specific relationship capital and long-term scarring effects that could impair growth prospects (see discussion in Colombia Country Update below). But high levels of non-financial sector leverage do raise questions about the effects on financial stability of the unwinding of these extraordinary measures coming out of the pandemic.

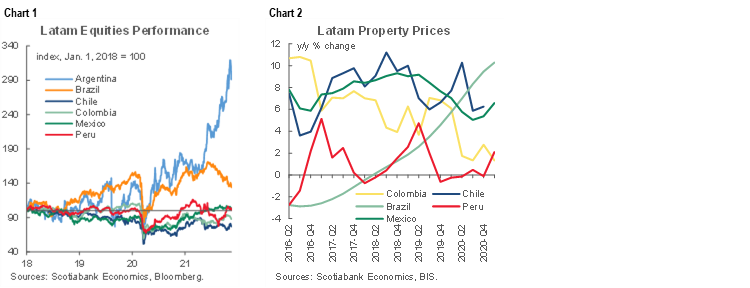

For the avoidance of doubt, there is scant evidence of serious imminent financial stability risks in Latam markets. Except for Argentina, where prices have soared over recent months, there are no clear signs of irrational exuberance in regional equity markets either preceding or in the wake of the pandemic (chart 1). Similarly, though the data is limited, and cross-country comparisons are fraught, year-over-year changes in Latam property prices do not appear exceptionally "frothy" (chart 2). If markets were caught up in a speculative frenzy, prices might be subject to extrapolative expectations, with progressively larger changes reflecting the expectation of still-higher prices to come. That isn’t the case in most Latam markets. In Brazil, increases prior to the pandemic might reflect an adjustment to the declines recorded in the earlier recession.

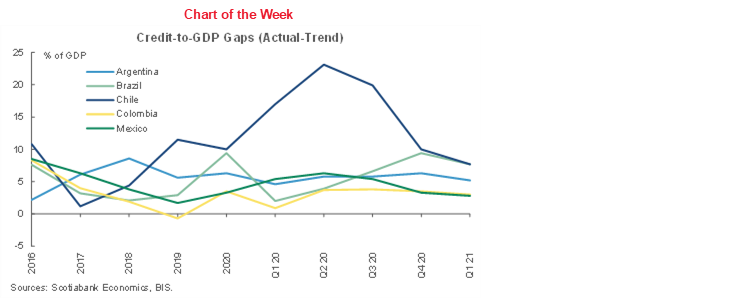

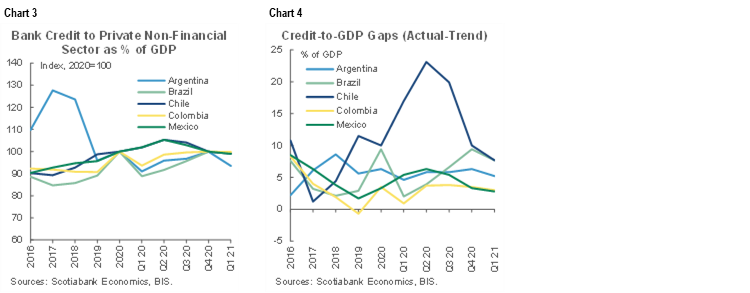

Two other indicators allay concerns of an excessively rapid build-up of debt. The first is bank credit to the private non-financial sector as a percentage of GDP (chart 3). Sharp increases in this ratio might signal excessively rapid credit expansion to fund speculative ventures or the accumulation of risky assets. The second indicator is the BIS credit-to-GDP gap, which shows the extent to which a broader measure of credit outstrips its underlying trend (chart 4). Here, too, an increase in the gap could warn of potential vulnerabilities. However, there is little to indicate an incipient problem of excessive credit expansion based on these two measures.

The broad conclusion from this admittedly cursory review, but one shared by recent local financial stability reports, seems to be that financial risks appear well contained.

While this assessment is certainly reassuring, it does not justify complacency and it would be imprudent to assume that risks do not exist. There may be idiosyncratic risks that are hidden by cross-country comparisons. For example, in Chile, the BCCh’s recent financial stability report notes with concern the impact of pension withdrawals in terms of the forced asset sales they created, which affected foreign exchange and debt markets and resulted in increased volatility of asset prices (see discussion below). Moreover, market disruptions at the global level can have spillover effects on local markets. In a panicked rush for the exits, investors are less likely to heed local indicators of financial health and more prone to follow the herd to safe-haven assets.

In such circumstances, investors may be more inclined to differentiate risks on the basis of broad macroeconomic measures. In this regard, while fiscal policy responses across most of the Latam region played a critical role in attenuating the impact of the pandemic and laying the foundations for robust recoveries, they have led to a marked increase in public sector debt burdens. In a sense, these measures shifted risks from private sector balance sheets to the public sector. Though the effects of this risk transfer are not readily discernible in financial market indicators such as the 10-year CDS spreads over US Treasuries (chart 5), which have narrowed from their peaks in March 2020, increases in Brazil, Colombia and Peru bear monitoring.

Strong, credible policy frameworks that support price stability and fiscal sustainability can help deal with vulnerabilities associated with greater global liquidity, shifts in risk appetite and the search for yield. Many Latam governments have already moved to buttress these frameworks. But the question remains as to whether additional measures beyond those macroeconomic policies should be deployed. Going forward, debate is likely to focus on the use of macroprudential measures; the proactive use of these instruments, it could be argued, would allow central banks to better manage the inter-temporal policy trade-offs they face. Tightening macroprudential policies might allow inflation-targeting central bankers to better calibrate monetary conditions to inflation control, while reducing the likelihood of a severe "tail risk" contraction associated with financial instability.

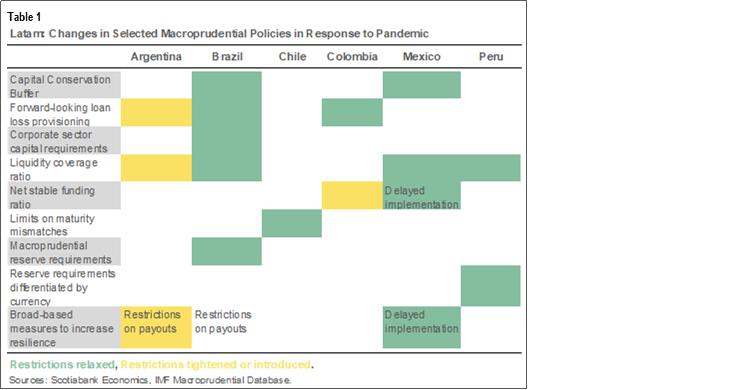

Such measures are already in place across the Latam region, especially measures related to the foreign currency exposure of banks. And as tracked by the IMF, many macroprudential measures were relaxed in the pandemic to promote credit flows to businesses and households (table 1). In this respect, advocates of macroprudential policies could argue that there is ample scope to tighten them now that recoveries are well established. Doing so, they contend, would have the salutary effect of insulating domestic financial systems from external shocks coming from shifts in investor risk appetite and unexpectedly aggressive tightening by advanced country central banks.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—A Hectic Political Agenda in Congress, Ahead of the Presidential Election

Jorge Selaive, Chief Economist, Chile

56.2.2619.5435 (Chile)

jorge.selaive@scotiabank.cl

Anibal Alarcón, Senior Economist

56.2.2619.5435 (Chile)

anibal.alarcon@scotiabank.cl

Waldo Riveras, Senior Economist

56.2.2939.1495 (Chile)

waldo.riveras@scotiabank.cl

The daily number of confirmed COVID-19 cases has continued to rise in recent days, reaching its highest level in four months, reflecting an increase in the positivity rate to 3.3% in the last week, despite the vaccination campaign having reached 90.5% of the eligible population. The occupancy of ICU beds and the COVID-19-related death rates slightly increased but remain at low levels. Meanwhile, the rollout of booster (third) doses keeps moving forward, reaching almost 7.3 million people. Thanks to the success of the vaccination program, workplace mobility has surpassed pre-pandemic levels.

Regarding the economic indicators, on November 8, the statistical agency (INE) released October’s CPI, which increased 1.3% m/m (6.0% y/y), above both market and our expectations. The figure was explained mainly by increases in two services: tourist packages (+55.8% m/m) and air transport fares (+45.4% m/m), which contributed 0.85 percent points (ppts) to the m/m inflation. Because recent high inflation figures risk introducing persistence and second-round effects, the central bank (BCCh) has been raising the Monetary Policy Rate in recent months and announced an early normalization of the interest rate.

In Congress, on November 9, the Senate rejected the pension funds withdrawal bill that the lower house had approved. As a result, a mixed commission of deputies and senators is studying and modifying the bill. In its meeting held on Wednesday, November 17, the commission defined nine key points of change required to reach approval in both Houses. The proposals are related to the introduction of some restrictions to the bill including, among others, a reduction in the maximum amount; income tax on withdrawals; dividing the benefit into two payments; and an agreement to ensure this is the last withdrawal.

With respect to the above, the central bank warned about the implications that the pension fund withdrawals have for the financial stability and has been implementing some macro-prudential measures to contain its financial and economic impacts, in line with its legal mandate. According to the BCCh, the impacts have different channels of transmission: a short-term macroeconomic channel, mainly in consumption, domestic demand and economic activity; a structural channel, due to the impact on the saving rate; expectations, with effects on uncertainty; and financial, affecting asset prices. To reduce the financial impact, last year the BCCh announced a program to conduct repos with pension funds to purchase up to USD 10 bn in senior bank bonds to allow pension funds to maintain their investment positions and help reduce pressures that the pension fund withdrawal process would have likely generated on bank bonds and deposits in the short term.

Amid the discussion regarding a fourth withdrawal of 10% of pension funds, the BCCh noted that with every new withdrawal, its capacity to minimize the effects on financial markets is reduced. Up to November 15, the amount of the last three pension fund withdrawals reached USD 49.7 bn (20% of GDP) (chart 1), according to the pension supervisor’s estimates.

With regard to the presidential election (Sunday November 21), the November 5 Cadem poll showed that the far-right candidate José Antonio Kast continues to lead the race, followed by the left-wing candidate Gabriel Boric. However, in recent days both candidates made some unforced errors that could affect their performance in Sunday’s election. We believe that candidates who go to the second round will likely adjust their proposed programs to broaden their appeal. Both Kast and Boric have indicated that they are open to modifying their programs, and it is very likely that both will capture part of the programs of their allies.

Meanwhile, on November 16, the Senate floor rejected the impeachment accusation against President Piñera, as expected. The bill was based on possible crimes of bribery and tax evasion in the sale of Minera Dominga and had two chapters, neither of which received the two-thirds majority required for approval.

Due to the political factors mentioned above, among others, the long-term nominal interest rates have decreased in recent days. In effect, with the rise in short-term nominal interest rates and the fall in 10-year rates, some days ago we warned about the risk of having an inverted yield curve in the next few months. We consider that the drop in the 10yr–2yr year spread that we are currently observing is mostly associated with higher inflationary expectations and the consequent monetary normalization, in a context of an uncertain political scenario (chart 2).

In the fortnight ahead, on Sunday, November 21, we will have the results of the presidential election, while on Monday, November 22 Congress should approve the 2022 Fiscal Budget. In addition, on Wednesday, November 30, the INE will release unemployment rate for the quarter that ended in October. Lastly, on Thursday, December 1, the BCCh will publish the monthly economic activity for October.

Colombia—The Significance of Reaching Pre-pandemic Activity Levels

Sergio Olarte, Head Economist, Colombia

57.1.745.6300 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Economist

57.1.745.6300 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

This week the statistical agency revealed that in the third quarter the Colombian economy surpassed pre-pandemic activity levels showing that, following a period of almost no pandemic-related restrictions, the economy could rebound and recover faster than expected. But what is this recovery signaling? Is the output gap closing faster than expected? Did potential GDP fall less than expected? What are the risks ahead? And what are the implications for the monetary policy?

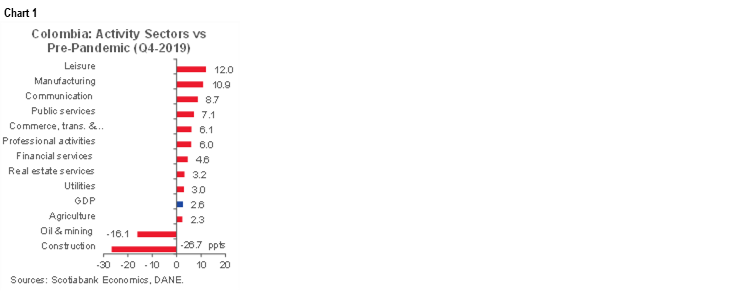

In the third quarter, the economy operated 2.6% above pre-pandemic levels (chart 1). Only two sectors continued to lag the recovery, mining (-16.1% versus pre-pandemic) and construction (-26.7% versus pre-pandemic). Output in the mining sector reflects weaker production, especially in oil and coal; while the construction sector is showing an effect of lower activity, as big civil works projects are in a final phase with a lower value-added. The other ten sectors are now above pre-pandemic levels, with some showing the surge of new activities amid the pandemic, for example, online betting. Traditional sectors, meanwhile, are now rebounding as operating conditions have improved amid a reduction in mobility and capacity restrictions. On the demand side, consumption—both public and private—lead the gains, while investment remains below pre-pandemic levels (-13.3% versus Q4-2019), showing the continued influence of lower construction activity.

In a fairly simple calculation, if the Colombian economy repeats the same performance of the third quarter in the fourth quarter, 2021 economic growth would stand between 9.8% and 10.3%. The main vulnerability in this scenario would come from renewed lockdowns amid new COVID-19 waves. However, we assign a low probability to this as the vaccination plan has advanced, and 45.8% of the population is now fully vaccinated.

Another relevant risk would come from international supply chain bottlenecks, which could disrupt regular industrial processes and translate into higher prices to consumers. For now, the commerce sector has warned of the risk of higher prices and lower-than-usual inventories for the year-end. Such effects may be felt unevenly across the economy: some sectors have reported a sudden increase in their supplies, while others have experienced interruptions in production due to delays in getting enough raw materials.

Previous dynamics also warrant close monitoring as, after the third quarter, pre-pandemic levels are no longer the benchmark. That is why despite recent results skewing our current expected GDP growth (9.1% y/y) to the upside, we prefer to maintain a conservative view.

Ahead of 2022, it will be important to look for a rebound in investment, especially in the construction sector, which has been strongly supported by the government. However, 2022 is likely to start slowly, since it is common for some private businesses to wait until after elections to make relevant investment decisions—an effect that is referred to as an “electoral clause”—in the event that the new administration shifts from a pro-market model. In fact, in 2018 before the elections, some investment decisions were basically frozen, while after the elections private firms were more confident to invest. If this phenomenon is repeated, that outcome would slow down the activity at the beginning of the year. Despite this possibility, we affirm our expectation of a 4.5% GDP expansion in 2022.

In this regard, stronger economic growth could have positive outcomes in terms of fiscal accounts—the MoF reported net tax collection grew by 22.6% vs 2020 (YTD up to October) and by 6.1% vs 2019, which would lead to positive surprises in terms of fiscal balance. On the monetary policy side, the better economic outlook was the main reason BanRep accelerated the hiking cycle in October’s meeting; continued improvements in the outlook would motivate an early normalization of monetary conditions. That said, the labour market still lags the recovery, in terms of quantities but also of quality, which makes us continue to think that, while monetary policy must move to a less expansionary stance, it is premature to shift to a contractionary stance.

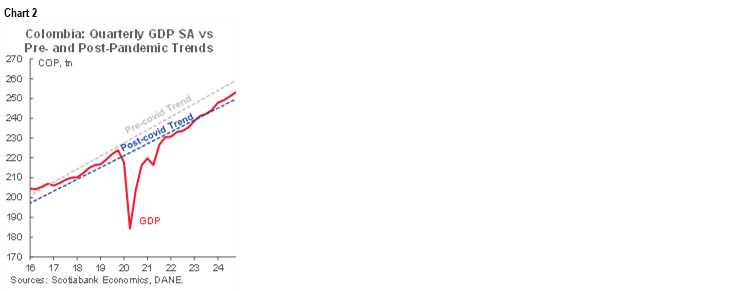

Looking ahead, with the economy operating normally, a critical question for the setting of monetary policy is whether the pandemic has had lasting effects on potential output. If the effects of the pandemic are purely transitory, GDP could be expected to return to its pre-COVID-19 trend (chart 2). On this basis, the economy has some way to go before returning to trend. However, it is possible that the pandemic has resulted in “scarring” effects that have reduced trend growth. If the relevant benchmark is the post-COVID-19 trend, the economy could have already returned to its longer-term path. In this event, monetary policy should reach the neutral rate in 2022, as is our base case scenario.

Mexico—Banxico: Re-shuffling the Deck

Eduardo Suárez, VP, Latin America Economics

52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

The first interest rate hike Banxico delivered at the start of the summer in 2021 caught economists (but not the market) by surprise. Heading into the decision, economists were almost universally looking for the central bank to remain on hold, as the price shock was seen as temporary and driven by short-term supply-side shocks and energy-related base effects. On the flip side, markets had already been pricing in the start of the tightening cycle for a couple of months. Since then, economists have remained at odds with the central bank, but the roles have been reversed (economists have seemed more hawkish on their views than most of the board).

Up until two central bank meetings ago, the guidance from the board suggested that getting the policy rate north of 5% would be a tall order, with deputy governors Esquivel and Borja supporting a hold, and deputy governor Heath stating that he only saw one or two 25 bps hikes over the course of the cycle (the policy rate was at 4.5%). At the same time, economists saw a terminal rate of around 6%, and the TIIE market was discounting a terminal rate close to 7.5%.

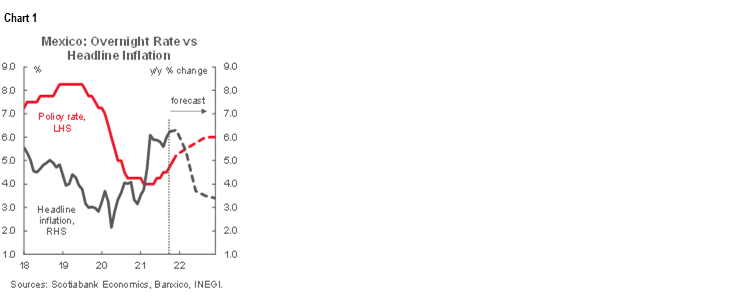

It increasingly looks likely that despite the departure of Governor Diaz de Leon—who has been among the two most hawkish members in the second half of 2021—at the end of the year, the unwind of monetary stimulus will continue into 2022, with the terminal rate being close to neutral (6.0% - which is our base case, chart 1), or even higher. There are several reasons for this:

- In its last policy decision, Banxico revised its inflation forecast for 2021 materially higher (to 6.8%, up from 6.2% at the end of September).

- In addition, core inflation is now forecast to remain above the top end of the target range until 2022Q4.

- Furthermore, yesterday, deputy governor Heath, who had previously suggested he would be unlikely to support rates at even 5.0%, said he believes inflation will close the year as high as 7.3% and described inflation as becoming “a very serious problem”.

With deputy governor Heath now seemingly turned more hawkish, and deputy Borja supporting tightening, at the same time as Banxico continues to revise inflation forecasts higher, we expect rate hikes will continue even with the departure of Governor Diaz de Leon. We are not yet in the camp that sees the pace of hikes accelerating to 50 bps moves, but we think it will be important to monitor comments by deputies Borja, Heath and Espinosa, as we don’t shut the door on that possibility. We also see risks that the rate hike cycle could end up being more front-loaded than our base case currently calls for. In addition, with evidence mounting that we are indeed getting some demand-side price pressures, we also see a growing possibility that the terminal rate could end up being higher than the 6% level we currently expect. At this point, however, we don’t yet see enough evidence to make the revision.

Peru—A Closer Look at Fiscal and Monetary Policy

Guillermo Arbe, Head of Economic Research

51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

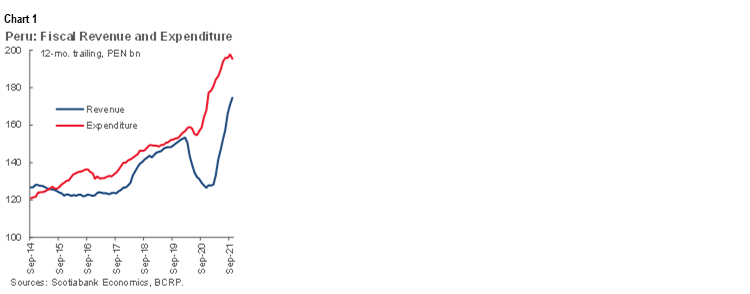

Fiscal policy has become prudent pretty much by default, as fiscal revenues have taken off quite independently of government action (chart 1). However, things are a bit more challenging for monetary policy.

Fiscal management

There are four aspects to highlight in terms of fiscal management under the Castillo regime:

1. The intention to a return to the fiscal rule of 1% of GDP by 2025.

2. Institutional continuity as manifested in key policy documents, including the 2022 budget, and the Multi-Year Macroeconomic Framework (Marco Macroeconómico Multianual, MMM), which show no significant break with the past.

3. The request before Congress for exceptional powers to legislate on a tax reform.

4. An improving fiscal picture, with no significant modifications in either the government spending schedule, or the strong tax revenue trend.

One of the first acts of Finance Minister Francke has been to stress the importance of the fiscal rule. His words and actions show seriousness of intent, aside from a clear intention to boost investor confidence. Since first established in 1999, the fiscal rule has changed at times, but has largely revolved around 1% of GDP. The rule is currently suspended for 2020–2021 due to the COVID-19 pandemic. The MEF lays out the following path to return to the 1% rule:

2021: -4.7%

2022: -3.7%

2023: -2.7%

2024: -1.7%

2025: -1.0%

The path is ambitious, but doable. In fact, we expect the targets for the 2021–2022 period to be surpassed. This is already the case in 2021, as the 12-month trailing fiscal deficit to October has come in at 4.1% of GDP (chart 2). The trend is on track to meet our full-year 2021 forecast of 3.7% of GDP. For 2022, we expect the fiscal deficit to decline further, to 3.5% of GDP, also surpassing the government target.

By far the main driver behind the improving fiscal trend has been fiscal revenue, which rose a considerable 46% y/y in January–October. Lest one believe this is solely a rebound from the 2020 lockdown, this represented a 17.9% increase from the same period in 2019. Both high metal prices and the increasing digitalization of sales have contributed. Increased digitalization has led to the formalization of previously informal sales.

Things may become more difficult from 2023 on, however. Commodity prices are stabilizing and, although high prices in 2021 will continue to affect revenue in 2022, the impact should fade afterwards, barring another boost in prices, which appears unlikely. The digitalization of sales is a structural change which may persist a bit more, but will also eventually exhaust itself. At some point, tax revenue growth will either depend once again on organic GDP growth, or require an increase in taxes. We expect GDP growth to be in the mid-2% range from 2022 to 2025, which may be too low to guarantee an exact return to the fiscal rule by 2025, especially considering that government spending is not likely to be curtailed, but the miss will not necessarily be too worrisome.

Meanwhile, the government has requested that Congress provide it with special powers to modify taxes in hopes of increasing resources for spending on social programs, while at the same time enabling the return to the fiscal rule that it seeks. Given the level of confrontation between Congress and the Executive, the chances that Congress will award these powers appear to be slim. If so, the Executive could still introduce new tax legislation piecemeal, although it would still need to rely on Congressional approval for some of the more significant proposals. The clock is ticking, as any new legislation would need to be introduced before December 30, 2021 for it to be in effect in 2022. Otherwise, tax change proposals will not be effective until 2023 at the earliest. Not that there is much urgency in fiscal management terms, as the short-term fiscal picture is sufficiently robust.

The government is seeking special powers to be able to increase taxes, especially on the affluent, the mining sector, real estate rent and financial market earnings. On mining, in particular, there is talk of increasing the minimum mining royalty from 1% of sales currently, presumably to 2%, and increasing the “Special Mining Tax”, which is an incremental tax that currently ranges from 2% to 8.4% of operating income.

The powers would also seek to broaden the tax base, in part through simplification. The tax structure for small business would be simplified, for example. Finally, the government would be including measures to reduce tax evasion and elusion, including introducing an automatic tax code, and enhancing the digitalization of sales and tax payments.

Monetary measures

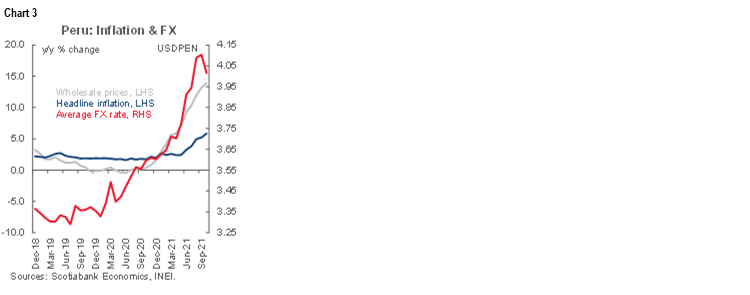

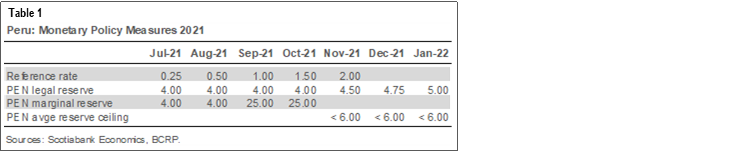

Meanwhile, with yearly inflation at 5.8% in October and rising, there is a partial shift in concern from growth to inflation (chart 3). This has put greater onus on the BCRP, which has become more aggressive on three fronts. The BCRP raised its reference rate from 0.25% in August, to 2.0% currently. We expect another 50 bps increase in December and for the rate to rise to 4.0%, at least, in 2022.

Secondly, the central bank (BCRP) significantly increased what is known here as the marginal reserve requirement on bank deposits (table 1). The reserve requirement on new deposits was raised from 4% to 25%, which means that banks must hold at the BCRP a quarter of each unit of PEN that it receives in deposit. However, the impact is softened by a 6% of deposits ceiling on total reserves. The impact of higher reserve requirements is to reduce liquidity availability in the banking system.

Finally, the BCRP has continued to be active in the FX market. The BCRP reported recently that it has provided USD liquidity to the FX market in the year-to-date to the tune of a huge USD 16.4 bn injection. Of this, USD 10.8 bn were through sales to the spot market, and the remainder through derivatives and FX certificates. Since in Peru both the PEN and the USD are used in practice as common currency, the risk of currency depreciation feeding into inflation is, perhaps, greater than elsewhere, which implies the need for the BCRP to include the FX market in its general monetary policy vision.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.