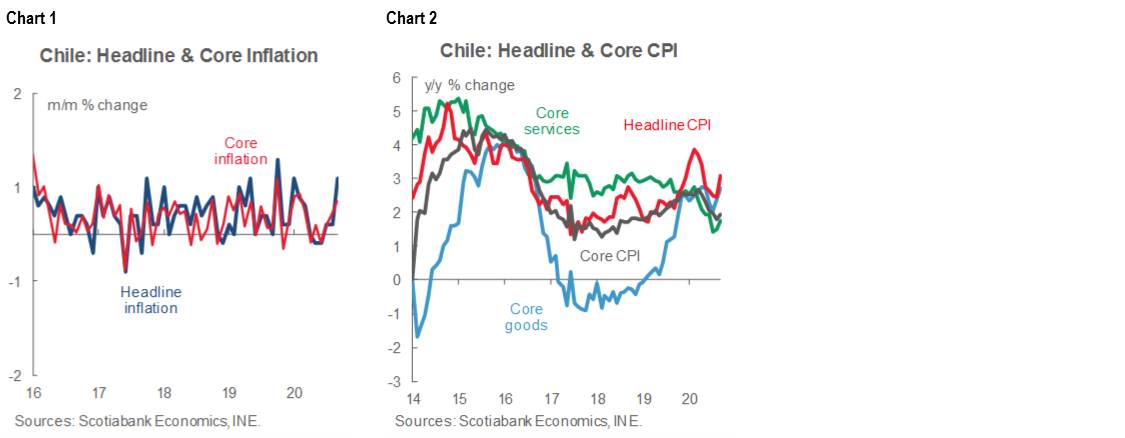

September CPI rose 0.6% m/m, strongly surprising the market and leaving annual inflation at 3.1% y/y.

This print moves us to raise our end-2020 inflation forecast from

2.2% y/y to 2.4% y/y, identical to the BCCh’s own forecast.The BCCh should look through this print as it’s in line with its baseline scenario. We expect the Board to keep the monetary policy rate on hold at -0.5% into 2021.

SEPTEMBER CPI ROSE 0.6% M/M, STRONGLY SURPRISING THE MARKET AND LEAVING ANNUAL INFLATION AT 3.1% Y/Y

At 07:00 ET this morning, INE published September’s CPI data, which showed an expectations-busting 0.6% m/m increase in the headline index (chart 1), up from 0.1% m/m in August and well above the 0.3% m/m rate expected in the Bloomberg consensus. The print moved annual inflation up from 2.4% y/y in August to 3.1% y/y in September, versus an expectation of

2.8% y/y (chart 2).

FORECAST REVISION

Although our baseline scenario already included a higher path for inflation than anticipated in the market consensus, September’s inflation surprise drives us to raise our forecast for end-2020 from the 2.2% y/y published in our October 4 Latam Weekly to 2.4% y/y. This aligns our outlook with the latest forecasts published by the BCCh, the central bank, in its September Monetary Policy Report. Although September’s surprise was generated mainly by food prices, other gains were sufficiently widely distributed across goods and services to merit this revision in our outlook. The CPI appears to be responding to the following factors:

1. The ongoing re-opening of the economy in a context where distributors and retailers do not have much financial flexibility to allow price reductions;

2. A strong demand shock from recent liquidity injections, including the withdrawal of up to 10% from pension accounts and the middle-class bonus, but where supply has not been able to respond. Retailers have reported sellouts of some durable goods, such as electronics and white goods, among others; and

3. Slight increases in costs derived from the depreciation of the CLP.

BCCh TO LOOK THROUGH THIS PRINT

Nevertheless, we hope that the BCCh will not read the September inflation print with undue concern, for the following reasons:

1. September’s upside surprise was driven by a transitory consumer demand shock underpinned by the liquidity injections from the withdrawal of pension account funds and fiscal aid—not a solid increase in wage bills;

2. Economic activity indicators for August disappointed, mainly owing to the slow recovery of investment, which is the main determinant of employment; and

3. The September print is still consistent with the central bank's baseline scenario that foresees annual inflation ending 2020 at 2.4% y/y.

IN THE DETAILS: BROAD BASE FOR SEPTEMBER SURPRISE

September’s monthly CPI inflation rate of 0.6% m/m (3.1% y/y) was mainly explained by increases in food prices (with a contribution of 0.37 ppts) and a rebound in core inflation, especially in goods (chart 3). Core inflation increased 0.3% m/m (2.2% y/y), which was mainly explained by goods price inflation of 0.6% m/m (3.1% y/y) and to a lesser extent by incipient inflationary pressures coming from services prices (0.2% m/m; 1.7% y/y), which continue to be affected by data that have been missing since the beginning of the pandemic and are simply imputed.

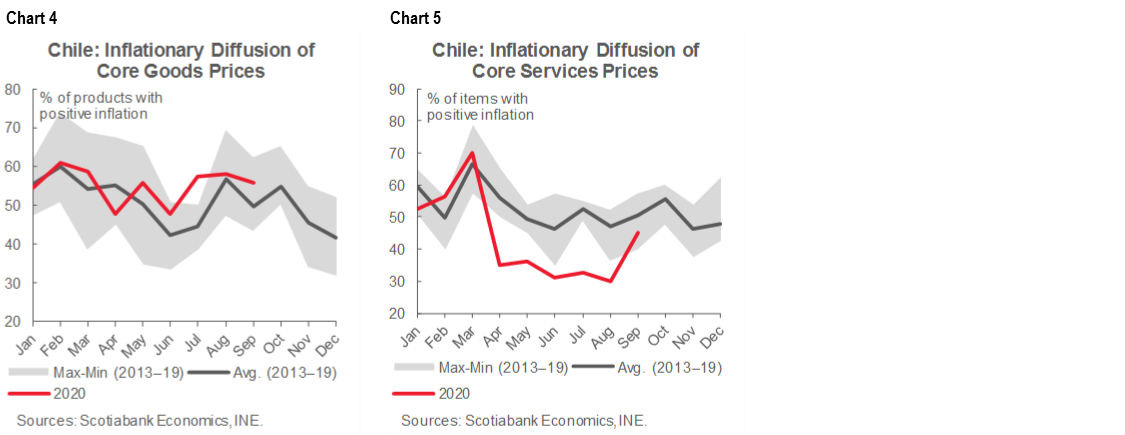

Our inflationary diffusion indicator (i.e., the percentage of products with positive monthly inflation) showed that 54.8% of the products in the CPI basket saw price increases in September, higher than the historical average of 51.5% for the month. The diffusion of goods prices was 55.8%, also higher than its historical average (chart 4), while that of services was 45%, rebounding strongly with respect to recent readings earlier this year (chart 5)—consistent with the demand shock we noted above.

END TO IMPUTATION POSES NEW VOLATILITY AHEAD

For the next few months, it will be key monitor when and how the INE goes back to collecting price data in a manner closer to its usual practices as this could inject new volatility into upcoming inflation prints. It is not yet clear whether the disinflationary effects of the high output gap or the inflationary pressures emanating from constrained supply in the face of stimulated demand will dominate. For now, in its technical note, the INE observed that in September the imputation methods applied in the previous months of the lockdown were maintained for cases where actual prices could not be collected. This included an assumption of zero monthly price inflation in items such as tourist packages, air transportation, and other services. The extent of imputation has been rising—not falling—as the economy has re-opened and hit 28.2% in September, the highest value since last May. The INE advises that it will be constantly re-evaluating its imputation practices over the coming months with a view to re-incorporating actual prices as they become available.

LOOKING AHEAD TO OCTOBER’S INFLATION PRINT

On a preliminary basis, we expect headline inflation in October to land between 0.2% m/m and 0.3% m/m. On the downside, October prices should not see a significant inflationary contribution coming from fuels; also, food prices will be left with a high monthly base from September, which leads us to anticipate slightly less inflationary pressure from this segment. On the upside, we should see a positive impact on prices from the reinstatement of the stamp tax, which could contribute 0.06 ppts to the headline sequential inflation rate. Finally, we expect that in October the INE will begin collecting actual prices for air travel and tourist packages, which would inject an additional element of uncertainty into the monthly projection. Historical data imply that during May–October both items would have seen increases in their prices.

—Jorge Selaive, Carlos Muñoz & Waldo Riveras

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.